The heat modulated infinite dimensional Heston model and its numerical approximation

Publication

Metrics

AI Quick Summary

The paper introduces the HEat modulated Infinite DImensional Heston (HEIDIH) model, a novel infinite-dimensional stochastic volatility model, and analyzes its numerical approximation. The model combines a stochastic advection equation with a stochastic heat equation, driven by independent Gaussian processes, and is analyzed using fractional Sobolev spaces. Numerical convergence rates are derived, showing higher accuracy than standard techniques, and are illustrated through simulations.

Paper Preview

Abstract

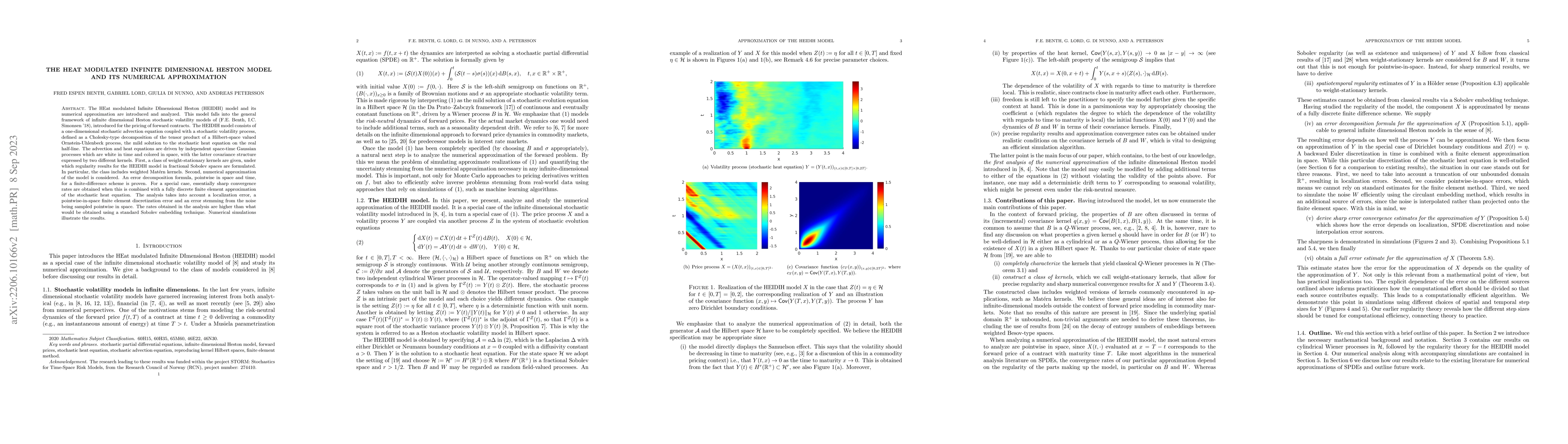

The HEat modulated Infinite DImensional Heston (HEIDIH) model and its numerical approximation are introduced and analyzed. This model falls into the general framework of infinite dimensional Heston stochastic volatility models of (F.E. Benth, I.C. Simonsen '18), introduced for the pricing of forward contracts. The HEIDIH model consists of a one-dimensional stochastic advection equation coupled with a stochastic volatility process, defined as a Cholesky-type decomposition of the tensor product of a Hilbert-space valued Ornstein-Uhlenbeck process, the mild solution to the stochastic heat equation on the real half-line. The advection and heat equations are driven by independent space-time Gaussian processes which are white in time and colored in space, with the latter covariance structure expressed by two different kernels. First, a class of weight-stationary kernels are given, under which regularity results for the HEIDIH model in fractional Sobolev spaces are formulated. In particular, the class includes weighted Mat\'ern kernels. Second, numerical approximation of the model is considered. An error decomposition formula, pointwise in space and time, for a finite-difference scheme is proven. For a special case, essentially sharp convergence rates are obtained when this is combined with a fully discrete finite element approximation of the stochastic heat equation. The analysis takes into account a localization error, a pointwise-in-space finite element discretization error and an error stemming from the noise being sampled pointwise in space. The rates obtained in the analysis are higher than what would be obtained using a standard Sobolev embedding technique. Numerical simulations illustrate the results.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0