Academic Profile

Statistics

Similar Authors

Papers on arXiv

We develop adaptive time-stepping strategies for It\^o-type stochastic differential equations (SDEs) with jump perturbations. Our approach builds on adaptive strategies for SDEs. Adaptive methods ca...

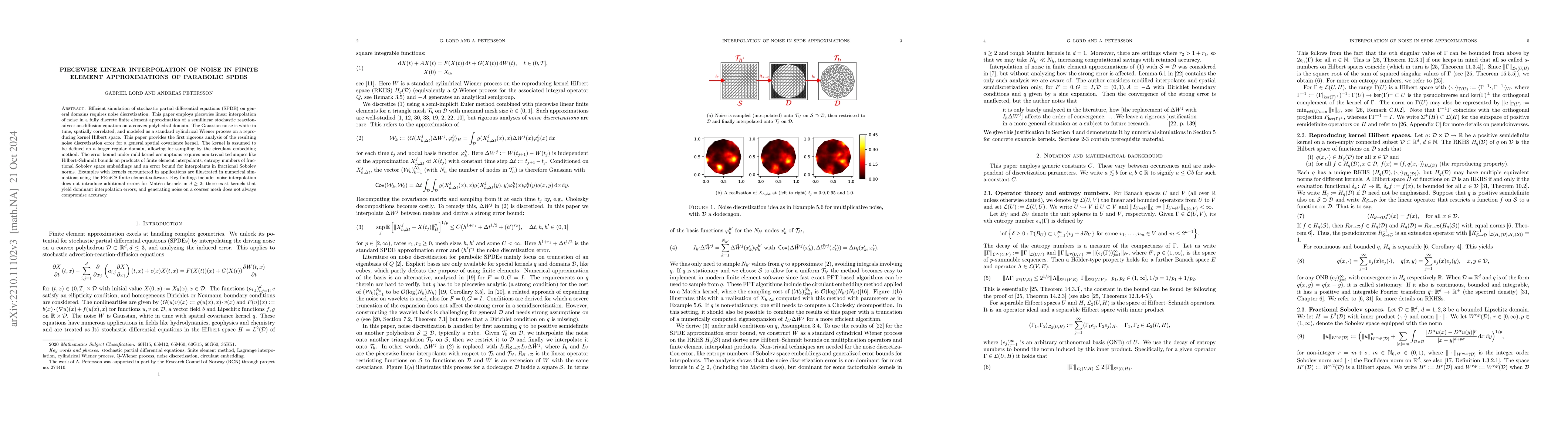

Efficient simulation of stochastic partial differential equations (SPDE) on general domains requires noise discretization. This paper employs piecewise linear interpolation of noise in a fully discr...

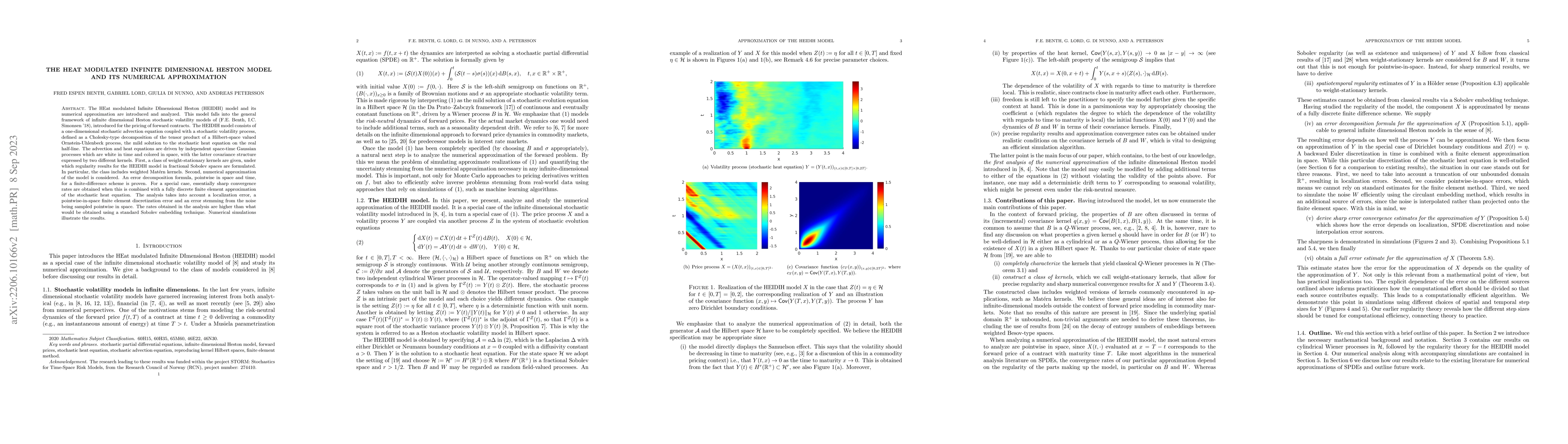

The HEat modulated Infinite DImensional Heston (HEIDIH) model and its numerical approximation are introduced and analyzed. This model falls into the general framework of infinite dimensional Heston ...

The full discretization of the semi-linear stochastic wave equation is considered. The discontinuous Galerkin finite element method is used in space and analyzed in a semigroup framework, and an exp...

We demonstrate the effectiveness of an adaptive explicit Euler method for the approximate solution of the Cox-Ingersoll-Ross model. This relies on a class of path-bounded timestepping strategies whi...

We introduce an explicit adaptive Milstein method for stochastic differential equations (SDEs) with no commutativity condition. The drift and diffusion are separately locally Lipschitz and together ...

In this paper, we develop numerical methods for solving Stochastic Differential Equations (SDEs) with solutions that evolve within a hypercube $D$ in $\mathbb{R}^d$. Our approach is based on a convex ...