Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper we derive novel change of variable formulas for stochastic integrals w.r.t. a time-changed Brownian motion where we assume that the time-change is a general increasing stochastic proce...

Horizon risk (see arXiv:2301.04971) is studied in the context of cash non-additive fully-dynamic risk measures induced by BSDEs. Furthermore, we introduce a risk measure based on generalized Tsallis...

In this paper, we present analytical proof demonstrating that the Sandwiched Volterra Volatility (SVV) model is able to reproduce the power-law behavior of the at-the-money implied volatility skew, ...

In this paper, we present a comprehensive survey of continuous stochastic volatility models, discussing their historical development and the key stylized facts that have driven the field. Special at...

In a dynamic framework, we identify a new concept associated with the risk of assessing the financial exposure by a measure that is not adequate to the actual time horizon of the position. This will...

We consider stochastic volatility dynamics driven by a general H\"older continuous Volterra-type noise and with unbounded drift. For such models, we consider the explicit computation of quadratic he...

We introduce a new model of financial market with stochastic volatility driven by an arbitrary H\"older continuous Gaussian Volterra process. The distinguishing feature of the model is the form of t...

Default risk calculus plays a crucial role in portfolio optimization when the risky asset is under threat of bankruptcy. However, traditional stochastic control techniques are not applicable in this...

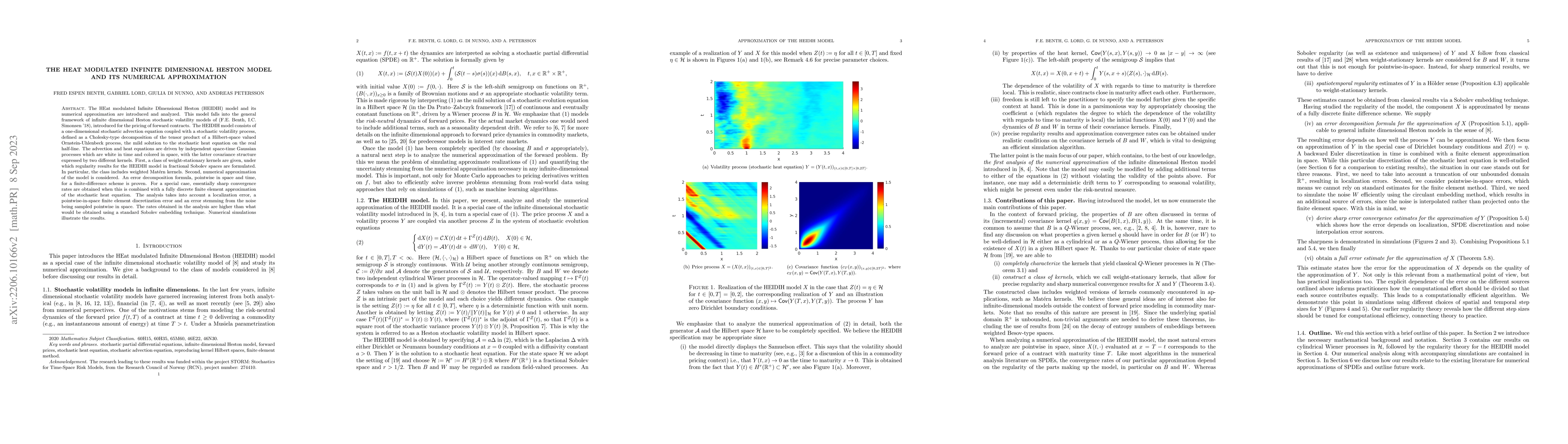

The HEat modulated Infinite DImensional Heston (HEIDIH) model and its numerical approximation are introduced and analyzed. This model falls into the general framework of infinite dimensional Heston ...

In this paper, we analyze the drift-implicit (or backward) Euler numerical scheme for a class of stochastic differential equations with unbounded drift driven by an arbitrary $\lambda$-H\"older cont...

This paper introduces SPDE bridges with observation noise and contains an analysis of their spatially semidiscrete approximations. The SPDEs are considered in the form of mild solutions in an abstra...

We prove Sklar's theorem in infinite dimensions via a topological argument and the notion of inverse systems.

We consider the infinite dimensional Heston stochastic volatility model proposed in \arXiv:1706:03500. The price of a forward contract on a non-storable commodity is modelled by a generalized Ornste...

Although copulas are used and defined for various infinite-dimensional objects (e.g. Gaussian processes and Markov processes), there is no prevalent notion of a copula that unifies these concepts. W...

We study a stochastic differential game between two players, controlling a forward stochastic Volterra integral equation (FSVIE). Each player has to optimize his own performance functional which inc...

We study the existence and uniqueness of solutions to stochastic differential equations with Volterra processes driven by L\'evy noise. For this purpose, we study in detail smoothness properties of ...

We consider an auction type equilibrium model with an insider in line with the one originally introduced by Kyle in 1985 and then extended to the continuous time setting by Back in 1992. The novelty...

We consider the problem of maximising expected utility from terminal wealth in a semimartingale setting, where the semimartingale is written as a sum of a time-changed Brownian motion and a finite v...

Motivated by dynamic risk measures and conditional $g$-expectations, in this work we propose a numerical method to approximate the solution operator given by a Backward Stochastic Differential Equatio...

The transmission of monkeypox is studied using a stochastic model taking into account the biological aspects, the contact mechanisms and the demographic factors together with the intrinsic uncertainti...

We develop a stochastic human-rodent compartment model for Mpox transmission that combines diffusion noise with Hawkes self-exciting jumps in the human infection dynamics. Including Hawkes processes a...

The Euler scheme is a standard time discretization for BSDEs, but its implementation hinges on approximating conditional expectations and the associated martingale terms at each time step. We propose ...

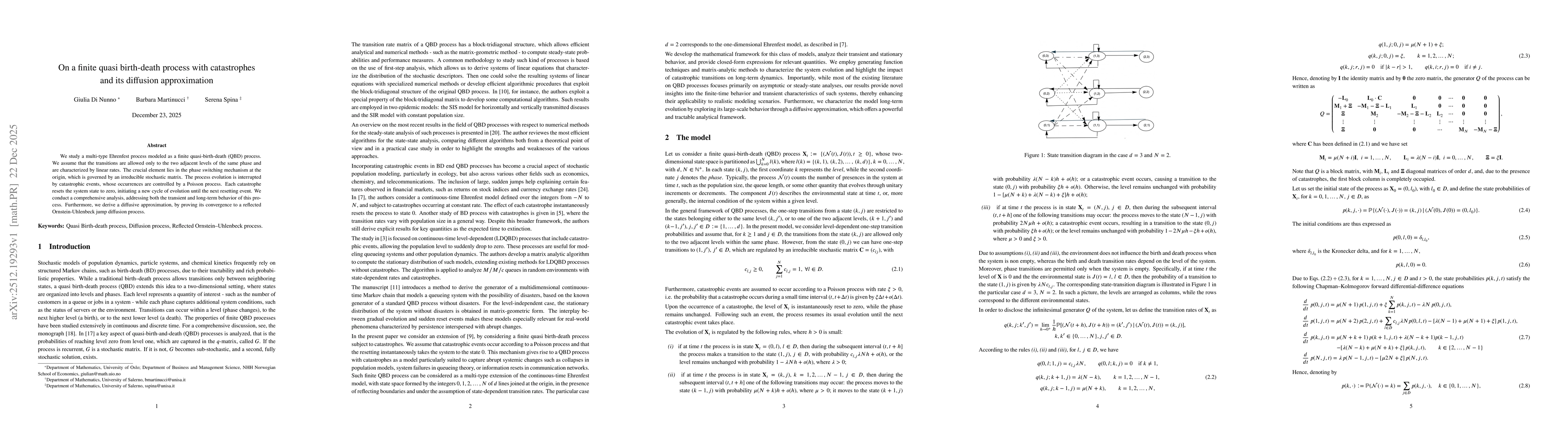

We study a multi-type Ehrenfest process modeled as a finite quasi-birth-death (QBD) process. We assume that the transitions are allowed only to the two adjacent levels of the same phase and are charac...

Whenever dealing with horizons of different times scales, risk evaluation of losses may incur in both interest rate uncertainty and horizon risk as introduced in [11]. With the goal to capture both ef...

We prove a Hölder-type regularity estimate for the martingale integrand of a backward stochastic Volterra integral equation (BSVIE). The estimate is formulated in $L^p(Ω)$ after averaging in $L^2$ ove...