Academic Profile

Statistics

Similar Authors

Papers on arXiv

Europe as a whole as well as individual countries have many distinct pathways to net carbon neutrality by 2050. We use novel near-optimal modelling techniques to illuminate trade-offs and interactio...

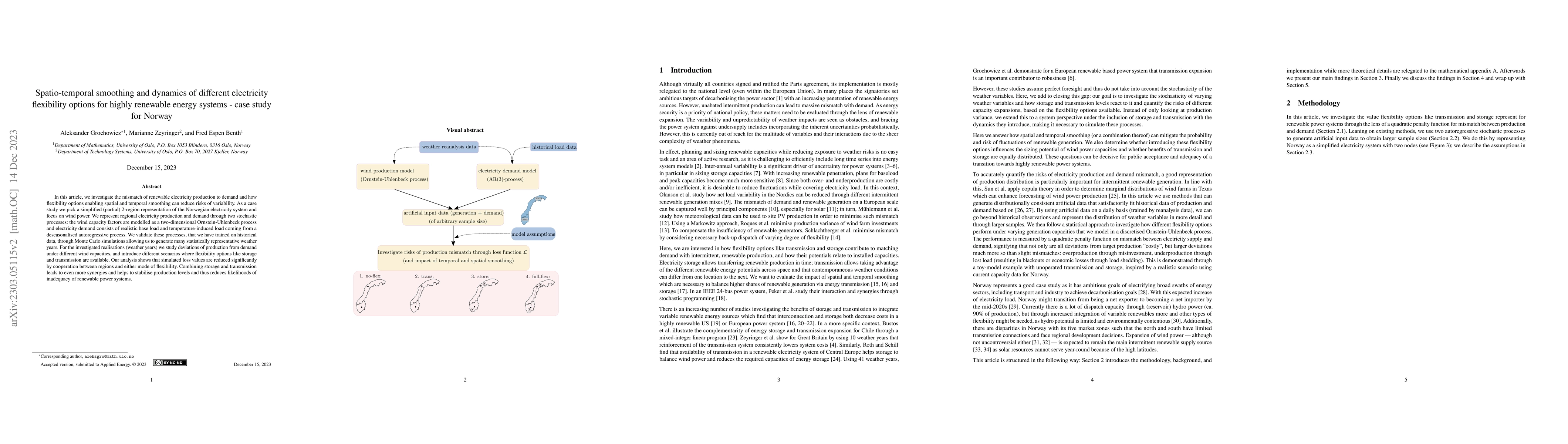

In this article, we investigate mismatch of renewable electricity production to demand and how this is affected by flexibility options on the supply side. We assess the impact of spatial and tempora...

In this paper we show that Hilbert space-valued stochastic models are robust with respect to perturbation, due to measurement or approximation errors, in the underlying volatility process. Within th...

We suggest a new methodology for designing robust energy systems. For this, we investigate so-called near-optimal solutions to energy system optimisation models; solutions whose objective values dev...

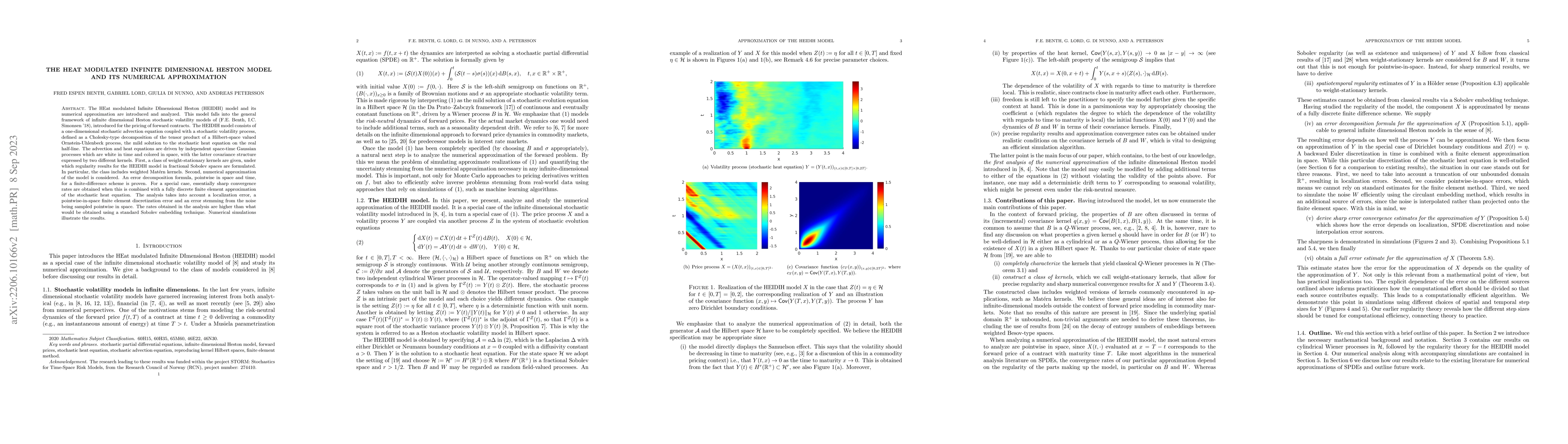

The HEat modulated Infinite DImensional Heston (HEIDIH) model and its numerical approximation are introduced and analyzed. This model falls into the general framework of infinite dimensional Heston ...

In this article we study multivariate continuous-time autoregressive moving-average (MCARMA) processes with values in convex cones. More specifically, we introduce matrix-valued MCARMA processes wit...

This article establishes an asymptotic theory for volatility estimation in an infinite-dimensional setting. We consider mild solutions of semilinear stochastic partial differential equations and der...

We propose a new methodology for pricing options on flow forwards by applying infinite-dimensional neural networks. We recast the pricing problem as an optimization problem in a Hilbert space of rea...

The share of wind power in fuel mixes worldwide has increased considerably. The main ingredient when deriving wind power predictions are wind speed data; the closer to the wind farms, the better the...

We provide a detailed analysis of the Gelfand integral on Fr\'echet spaces, showing among other things a Vitali theorem, dominated convergence and a Fubini result. Furthermore, the Gelfand integral ...

We prove Sklar's theorem in infinite dimensions via a topological argument and the notion of inverse systems.

We consider the infinite dimensional Heston stochastic volatility model proposed in \arXiv:1706:03500. The price of a forward contract on a non-storable commodity is modelled by a generalized Ornste...

Although copulas are used and defined for various infinite-dimensional objects (e.g. Gaussian processes and Markov processes), there is no prevalent notion of a copula that unifies these concepts. W...

This article generalises the concept of realised covariation to Hilbert-space-valued stochastic processes. More precisely, based on high-frequency functional data, we construct an estimator of the t...

We suggest a novel approach to polynomial processes solely based on a polynomial action operator. With this approach, we can analyse such processes on general state spaces, going far beyond Banach s...

We price European-style options written on forward contracts in a commodity market, which we model with an infinite-dimensional Heath-Jarrow-Morton (HJM) approach. For this purpose we introduce a ne...

In the setting of polynomial jump-diffusion dynamics, we provide an explicit formula for computing correlators, namely, cross-moments of the process at different time points along its path. The form...

We observe a multilinearity preserving property of conditional expectation for infinite dimensional independent increment processes defined on some abstract Banach space $B$. It is similar in nature...

This article surveys key aspects of ambit stochastics and remembers Ole E. Barndorff-Nielsen's important contributions to the foundation and advancement of this new research field over the last two de...

In this paper, we present a framework for learning the solution map of a backward parabolic Cauchy problem. The solution depends continuously but nonlinearly on the final data, source, and force terms...

This paper focuses on minimizing the costs related to renewable energy installations under emission constraints. We tackle the problem in three different cases. Assuming intervening once, we determine...

We present a novel perspective on the universal approximation theorem for rough path functionals, introducing a polynomial-based approximation class. We extend universal approximation to non-geometric...

Electric vehicle batteries have a proven flexibility potential which could serve as an alternative to conventional electricity storage solutions. EV batteries could support the balancing of supply and...

In this paper, we examine continuous-time autoregressive moving-average (CARMA) processes on Banach spaces driven by L\'evy subordinators. We show their existence and cone-invariance, investigate thei...

We study a stochastic model for the installation of renewable energy capacity under demand uncertainty and jump driven dynamics. The system is governed by a multidimensional Ornstein-Uhlenbeck (OU) pr...

We propose a numerical method for the valuation of European-style options under two-asset infinite-activity exponential Lévy models. Our method extends the effective approach developed by Wang, Wan & ...

This paper concerns the numerical valuation of swing options with discrete action times under a linear two-factor mean-reverting model with jumps. The resulting sequence of two-dimensional partial int...

We conduct the first rigorous study of electricity price volatility for the full panel of electricity prices across three European generation zones. By interpreting the observed day-ahead prices as lo...

We study forecasting of the realized covariation in electricity markets. The realized covariation in this context is a matrix-valued representation of the latent infinite-dimensional covariance operat...

McKean-Vlasov-type stochastic differential equations (SDEs) are characterized by coefficients depending on both the state and the law of the solution. In this work, we focus on a class of such equatio...

In this study, we develop a stochastic framework for computing Delta sensitivities in energy markets, where both prices and traded volumes are modeled as correlated stochastic processes. Within this f...