Academic Profile

Statistics

Similar Authors

Papers on arXiv

Continuous-time semi-Markov finite state-space jump processes are considered, inspired by a duration-dependent life insurance model. New approximations using grid-conditional homogeneous Markov jump...

The Mean-Field approximation is a tractable approach for studying large population dynamics. However, its assumption on homogeneity and universal connections among all agents limits its applicabilit...

This paper presents a novel model for bivariate stochastic fluid processes that incorporate a ruin-dependent behavioral switch. Unlike typical models that assume a shared underlying process, our mod...

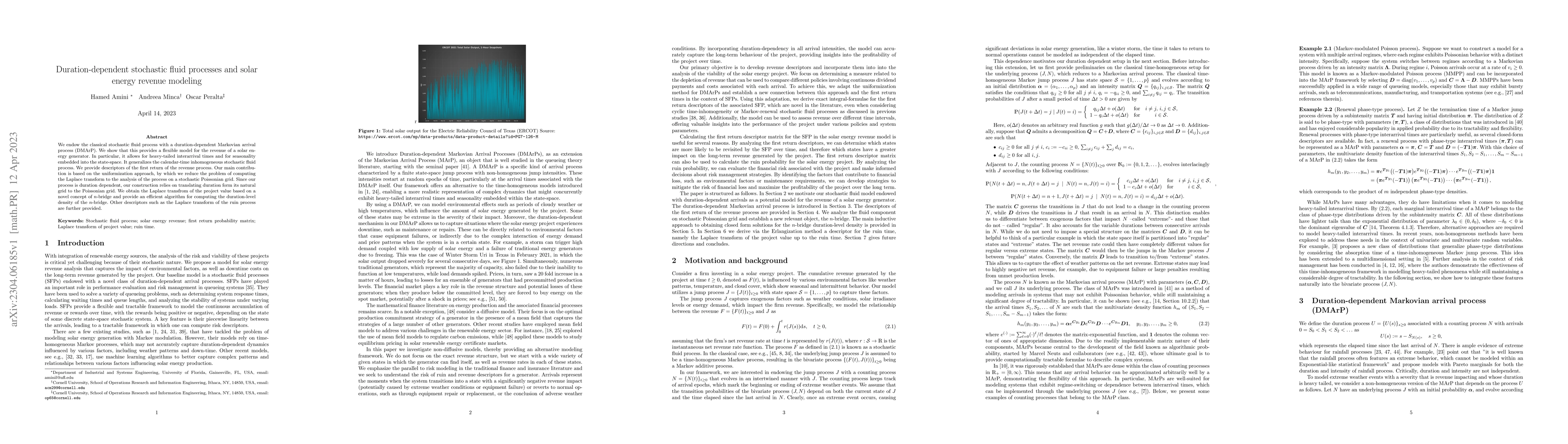

We endow the classical stochastic fluid process with a duration-dependent Markovian arrival process (DMArP). We show that this provides a flexible model for the revenue of a solar energy generator. ...

We study multidimensional Cram\'er-Lundberg risk processes where agents, located on a large sparse network, receive losses form their neighbors. To reduce the dimensionality of the problem, we intro...

We model incentive security in non-custodial stablecoins and derive conditions for participation in a stablecoin system across risk absorbers (vaults/CDPs) and holders of governance tokens. We apply...

We consider optimal intervention in the Elliott-Golub-Jackson network model \cite{jackson14} and we show that it can be transformed into an influence maximization-like form, interpreted as the rever...

We propose a reinforcement learning algorithm for stationary mean-field games, where the goal is to learn a pair of mean-field state and stationary policy that constitutes the Nash equilibrium. When...

We study a multi-type SIR epidemic process among a heterogeneous population that interacts through a network. When we base social contact on a random graph with given vertex degrees, we give limit t...

Stablecoins are one of the most widely capitalized type of cryptocurrency. However, their risks vary significantly according to their design and are often poorly understood. We seek to provide a sou...

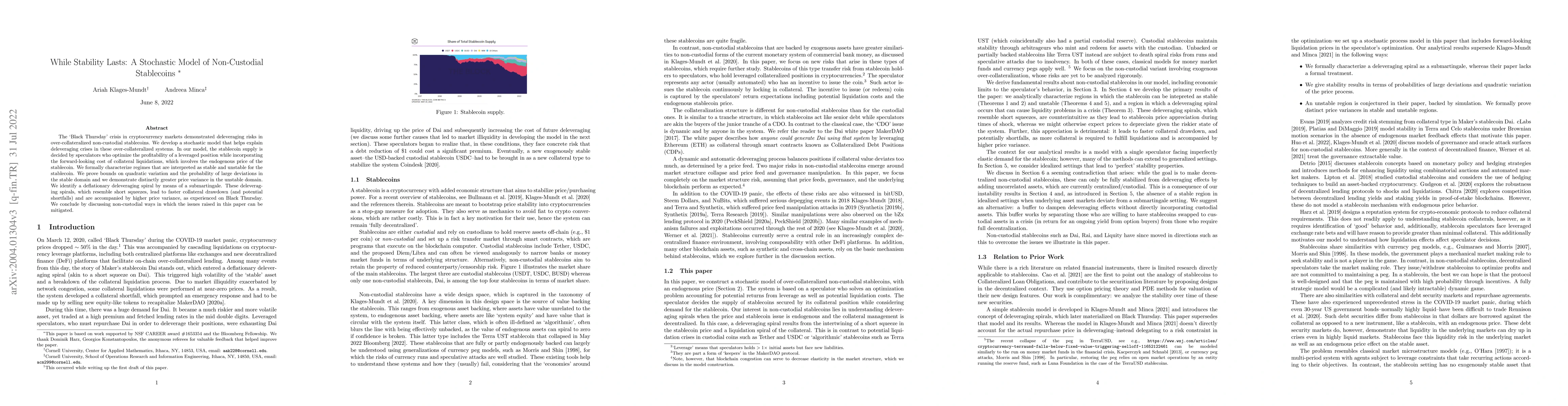

The `Black Thursday' crisis in cryptocurrency markets demonstrated deleveraging risks in over-collateralized non-custodial stablecoins. We develop a stochastic model that helps explain deleveraging ...

For the degree corrected stochastic block model in the presence of arbitrary or even adversarial outliers, we develop a convex-optimization-based clustering algorithm that includes a penalization te...

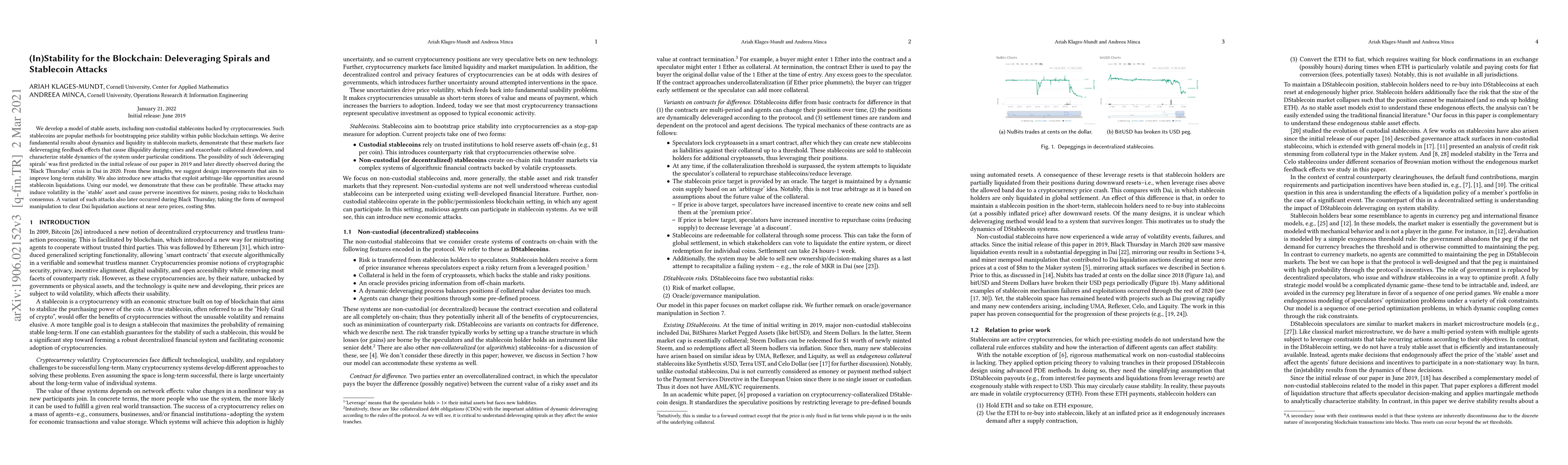

We develop a model of stable assets, including non-custodial stablecoins backed by cryptocurrencies. Such stablecoins are popular methods for bootstrapping price stability within public blockchain s...

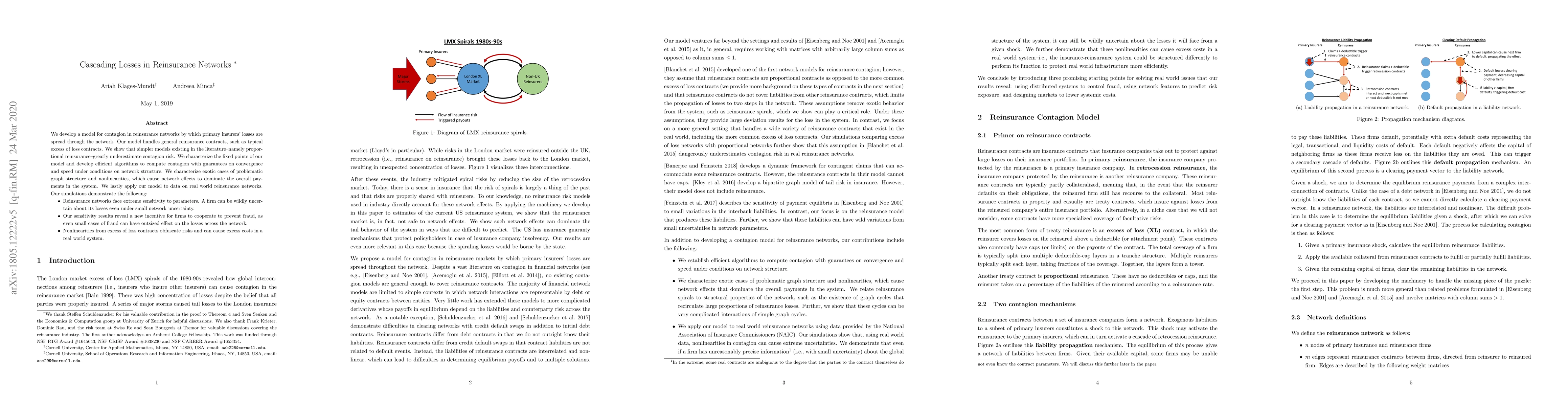

We develop a model for contagion in reinsurance networks by which primary insurers' losses are spread through the network. Our model handles general reinsurance contracts, such as typical excess of ...