Duration-dependent stochastic fluid processes and solar energy revenue modeling

Publication

Metrics

AI Quick Summary

This paper introduces a duration-dependent Markovian arrival process to model the revenue of solar energy generators, allowing for heavy-tailed interarrival times and seasonality. The authors use a uniformization approach to compute the Laplace transform, providing an efficient algorithm for determining the duration-level density and other descriptors.

Paper Preview

Abstract

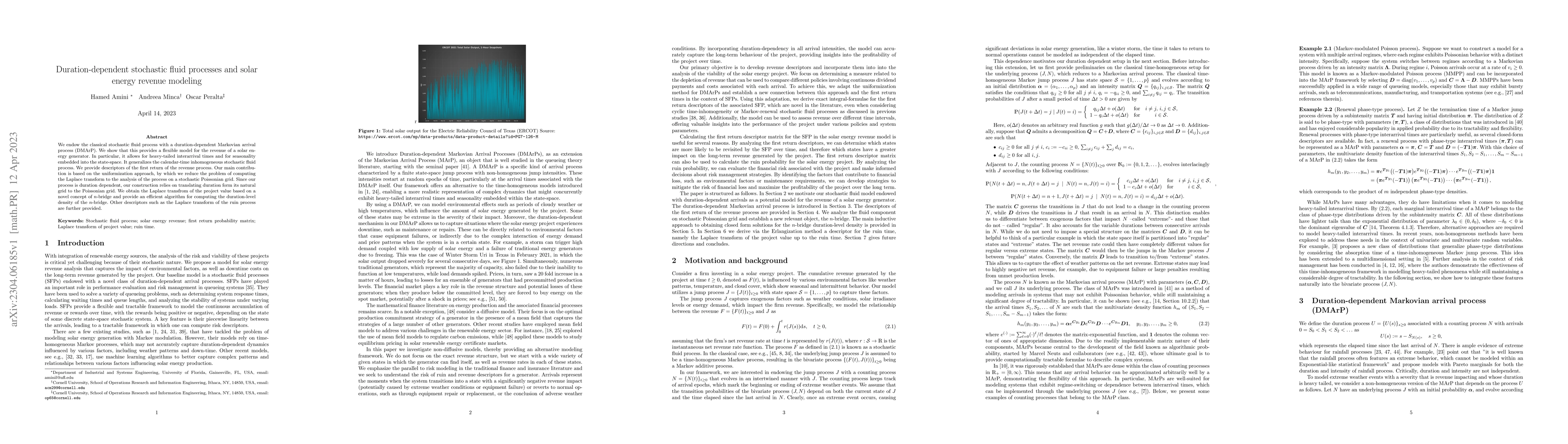

We endow the classical stochastic fluid process with a duration-dependent Markovian arrival process (DMArP). We show that this provides a flexible model for the revenue of a solar energy generator. In particular, it allows for heavy-tailed interarrival times and for seasonality embedded into the state-space. It generalizes the calendar-time inhomogeneous stochastic fluid process. We provide descriptors of the first return of the revenue process. Our main contribution is based on the uniformization approach, by which we reduce the problem of computing the Laplace transform to the analysis of the process on a stochastic Poissonian grid. Since our process is duration dependent, our construction relies on translating duration form its natural grid to the Poissonian grid. We obtain the Laplace transfrom of the project value based on a novel concept of $n$-bridge and provide an efficient algorithm for computing the duration-level density of the $n$-bridge. Other descriptors such as the Laplace transform of the ruin process are further provided.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0