Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we consider a system of heterogeneously interacting quantum particles subject to indirect continuous measurement. The interaction is assumed to be of the mean-field type. We derive a ...

This paper presents a novel model for bivariate stochastic fluid processes that incorporate a ruin-dependent behavioral switch. Unlike typical models that assume a shared underlying process, our mod...

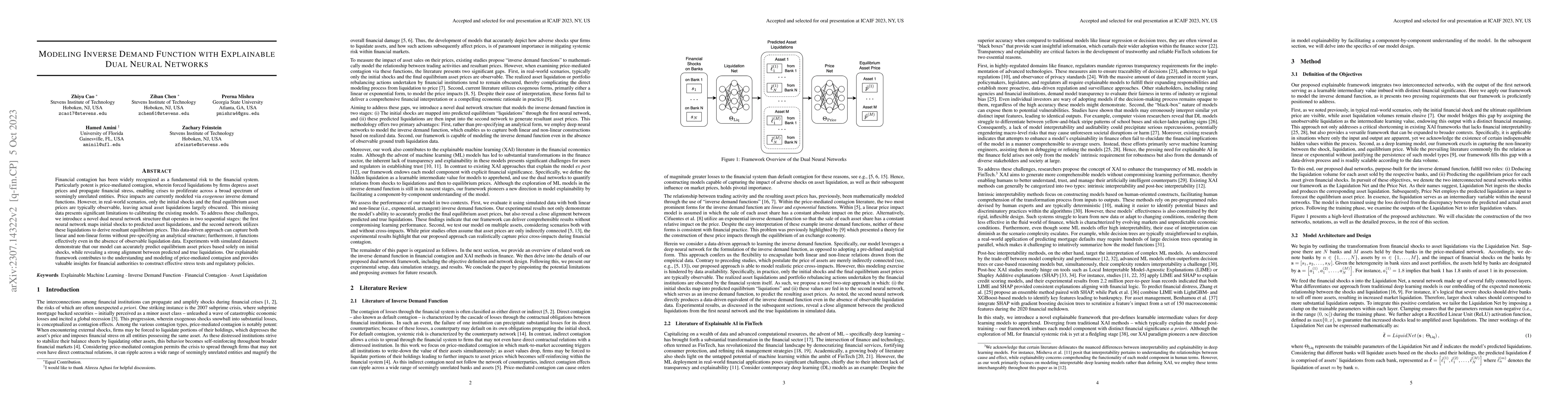

Financial contagion has been widely recognized as a fundamental risk to the financial system. Particularly potent is price-mediated contagion, wherein forced liquidations by firms depress asset pric...

Prediction markets allow traders to bet on potential future outcomes. These markets exist for weather, political, sports, and economic forecasting. Within this work we consider a decentralized frame...

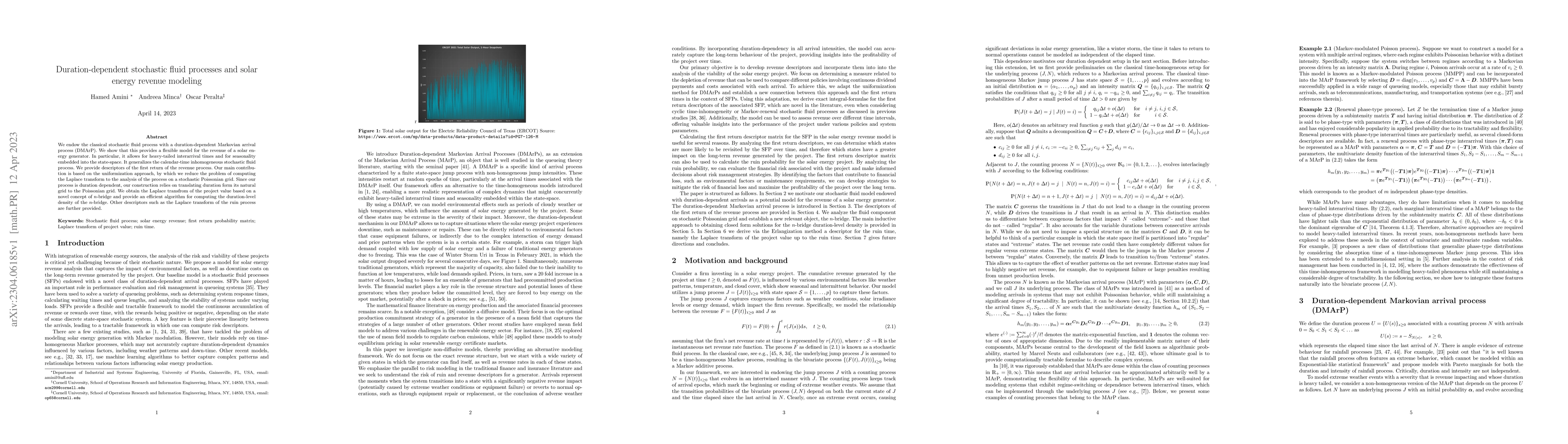

We endow the classical stochastic fluid process with a duration-dependent Markovian arrival process (DMArP). We show that this provides a flexible model for the revenue of a solar energy generator. ...

We study continuous stochastic games with inhomogeneous mean field interactions on large networks and explore their graphon limits. We consider a model with a continuum of players, where each player...

We study multidimensional Cram\'er-Lundberg risk processes where agents, located on a large sparse network, receive losses form their neighbors. To reduce the dimensionality of the problem, we intro...

In this paper, we construct a decentralized clearing mechanism which endogenously and automatically provides a claims resolution procedure. This mechanism can be used to clear a network of obligatio...

We consider a general tractable model for default contagion and systemic risk in a heterogeneous financial network, subject to an exogenous macroeconomic shock. We show that, under some regularity a...

We consider bootstrap percolation and diffusion in sparse random graphs with fixed degrees, constructed by configuration model. Every node has two states: it is either active or inactive. We assume ...

This paper introduces a formulation of the optimal network compression problem for financial systems. This general formulation is presented for different levels of network compression or rerouting a...

We study a multi-type SIR epidemic process among a heterogeneous population that interacts through a network. When we base social contact on a random graph with given vertex degrees, we give limit t...

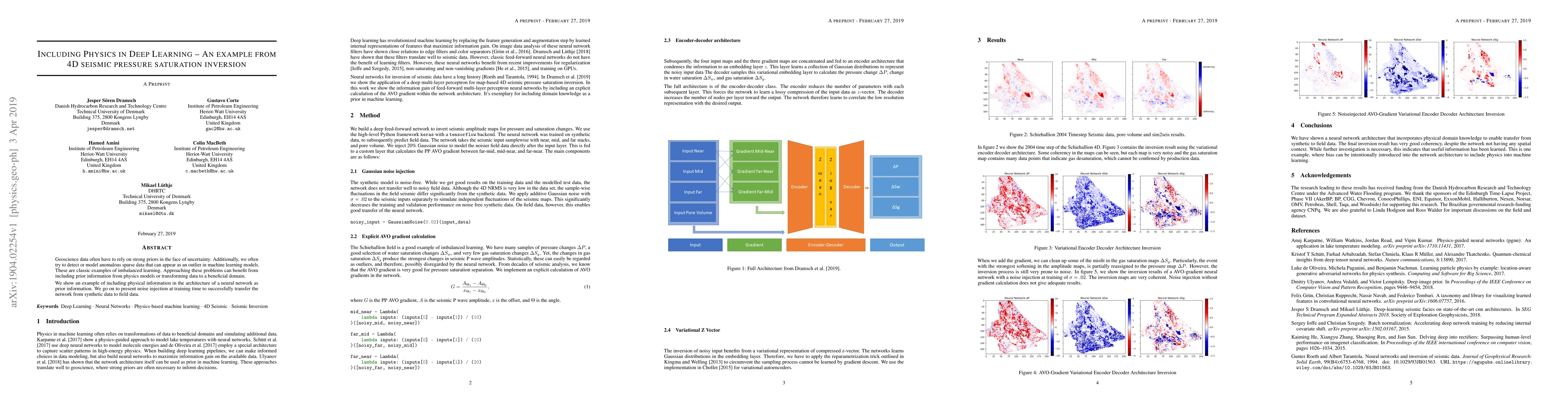

Geoscience data often have to rely on strong priors in the face of uncertainty. Additionally, we often try to detect or model anomalous sparse data that can appear as an outlier in machine learning ...

We consider a non-exchangeable system of interacting quantum particles with mean-field type interactions, subject to continuous measurement on a class of dense graphs. In the mean-field limit, we deri...

The aim of this paper is to establish a certain equivalence between a Brownian motion on a Fubini extension space and a collection of essentially pairwise independent Brownian motions on the marginal ...

Working within the quantum filtering framework, we establish a dynamic programming principle in an infinite-dimensional setting by embedding the state space into the Hilbert-Schmidt space. We then stu...