Academic Profile

Statistics

Similar Authors

Papers on arXiv

Continuous-time semi-Markov finite state-space jump processes are considered, inspired by a duration-dependent life insurance model. New approximations using grid-conditional homogeneous Markov jump...

The Mean-Field approximation is a tractable approach for studying large population dynamics. However, its assumption on homogeneity and universal connections among all agents limits its applicabilit...

This paper presents a novel model for bivariate stochastic fluid processes that incorporate a ruin-dependent behavioral switch. Unlike typical models that assume a shared underlying process, our mod...

This paper investigates the convergence of Wong--Zakai approximations to regime-switching stochastic differential equations, generated by a collection of finite-variation approximations to Brownian ...

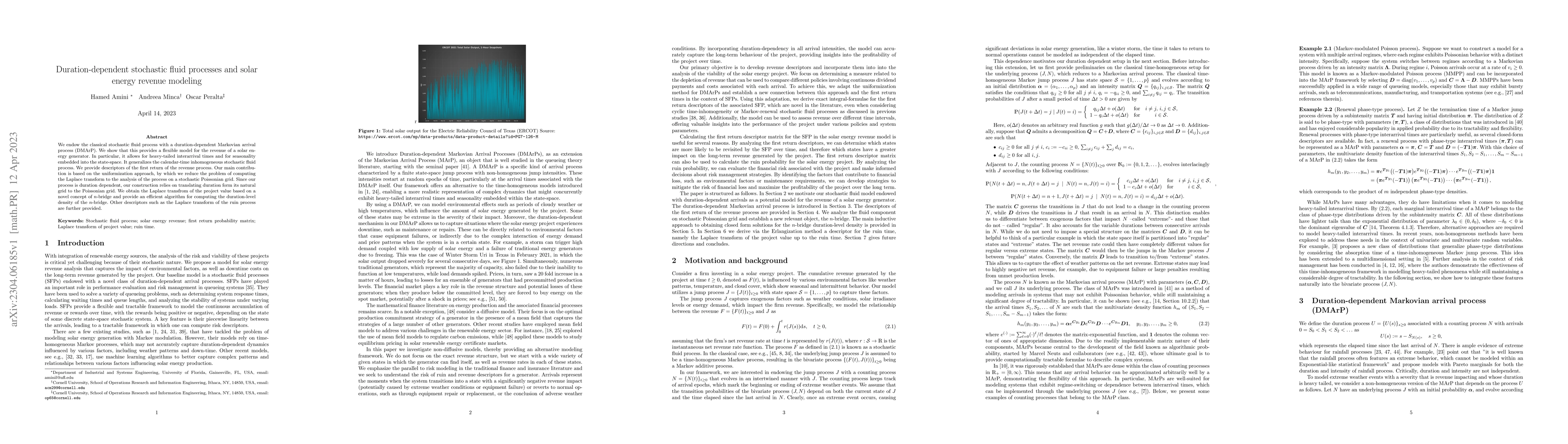

We endow the classical stochastic fluid process with a duration-dependent Markovian arrival process (DMArP). We show that this provides a flexible model for the revenue of a solar energy generator. ...

Hybrid stochastic differential equations are a useful tool to model continuously varying stochastic systems which are modulated by a random environment that may depend on the system state itself. In...

The study of time-inhomogeneous Markov jump processes is a traditional topic within probability theory that has recently attracted substantial attention in various applications. However, their flexi...

In this paper, a class of multivariate matrix-exponential affine mixtures with matrix-exponential marginals is proposed. The class is shown to possess various attractive properties such as closure u...

Let $f$ be the density function associated to a matrix-exponential distribution of parameters $(\alpha, T,s)$. By exponentially tilting $f$, we find a probabilistic interpretation which generalises ...

We construct a stochastic fluid process with an underlying piecewise deterministic Markov process (PDMP) akin to the one used in the construction of the rational arrival process (RAP), which we call...

We consider continuous time risk processes in which the claim sizes are dependent and non-identically distributed phase-type distributions. The class of distributions we propose is easy to character...

Strong approximations of uniform transport processes to the standard Brownian motion rely on the Skorokhod embedding of random walk with centered double exponential increments. In this note we make ...

In Latouche and Nguyen (2015), the authors constructed a sequence of stochastic fluid processes and showed that it converges weakly to a Markov-modulated Brownian motion (MMBM). Here, we construct a...

We introduce a novel class of bivariate common-shock discrete phase-type (CDPH) distributions to describe dependencies in loss modeling, with an emphasis on those induced by common shocks. By construc...

We introduce the hybrid risk process, constructed via a time-change transformation applied to the solution of a hybrid stochastic differential equation. The framework covers several modern ruin settin...

We introduce a class of continuous-time bivariate phase-type distributions for modeling dependencies from common shocks. The construction uses continuous-time Markov processes that evolve identically ...

This work introduces hybrid stochastic differential equations with memory (mH-SDEs), a new class of stochastic systems where transition rates depend on the joint history of both Euclidean and discrete...

Telek (2022) asked whether a rational arrival process (RAP), specified by matrices ${G}_0$ and ${G}_1$ and an initial row vector $ν$, with strictly positive joint densities and a unique dominant real ...

For a spectrally negative Lévy process with Laplace transform $ψ$, the $q$-scale function is characterized as the function whose Laplace transform is $(ψ(\cdot)-q)^{-1}$. It has applications in fluctu...

Near-deterministic positive delays require highly concentrated distributions, but phase-type models are constrained by the Erlang variance limit. While matrix-exponential distributions can empirically...

We resolve two questions left open by Bladt and Nielsen (2010) concerning multivariate families of matrix-exponential and phase-type distributions. First, in the matrix-exponential case, the projectio...