Academic Profile

Statistics

Similar Authors

Papers on arXiv

This work aims to deal with the optimal allocation instability problem of Markowitz's modern portfolio theory in high dimensionality. We propose a combined strategy that considers covariance matrix ...

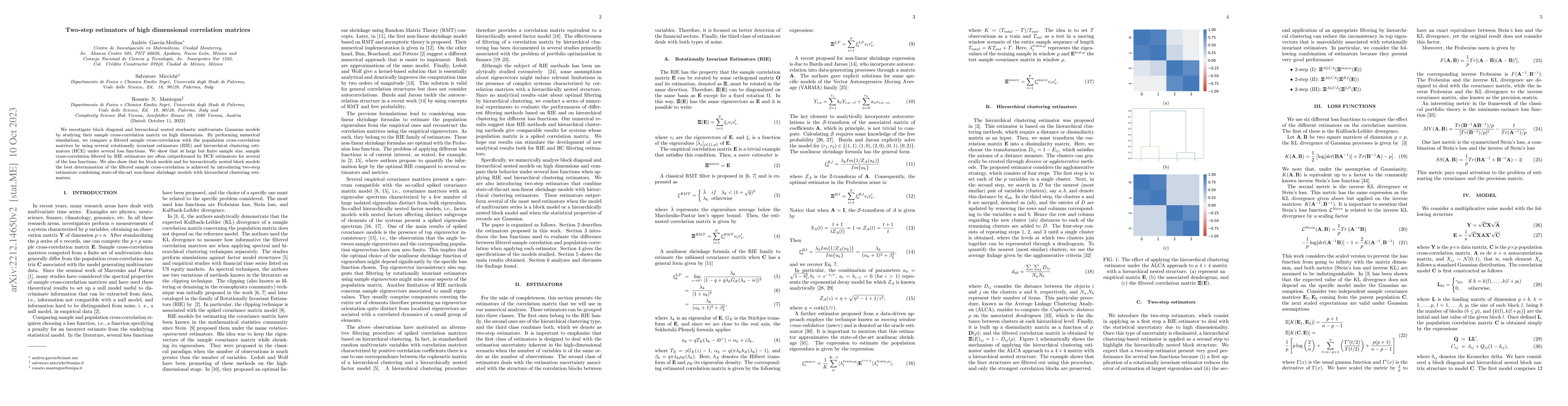

We investigate block diagonal and hierarchical nested stochastic multivariate Gaussian models by studying their sample cross-correlation matrix on high dimensions. By performing numerical simulation...

Bitcoin has attracted attention from different market participants due to unpredictable price patterns. Sometimes, the price has exhibited big jumps. Bitcoin prices have also had extreme, unexpected...

We study the allocation of synthetic portfolios under hierarchical nested, one-factor, and diagonal structures of the population covariance matrix in a high-dimensional scenario. The noise reduction a...

In this note, we compare Bitcoin trading performance using two machine learning models-Light Gradient Boosting Machine (LightGBM) and Long Short-Term Memory (LSTM)-and two technical analysis-based str...

Detecting the number of global factors in high-dimensional correlation matrices is a central problem in multivariate statistics and random matrix theory, with important implications for asset pricing ...