1

arXiv Papers

2

Total Publications

Profile

Academic Profile

Metrics

Statistics

1

arXiv Papers

2

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

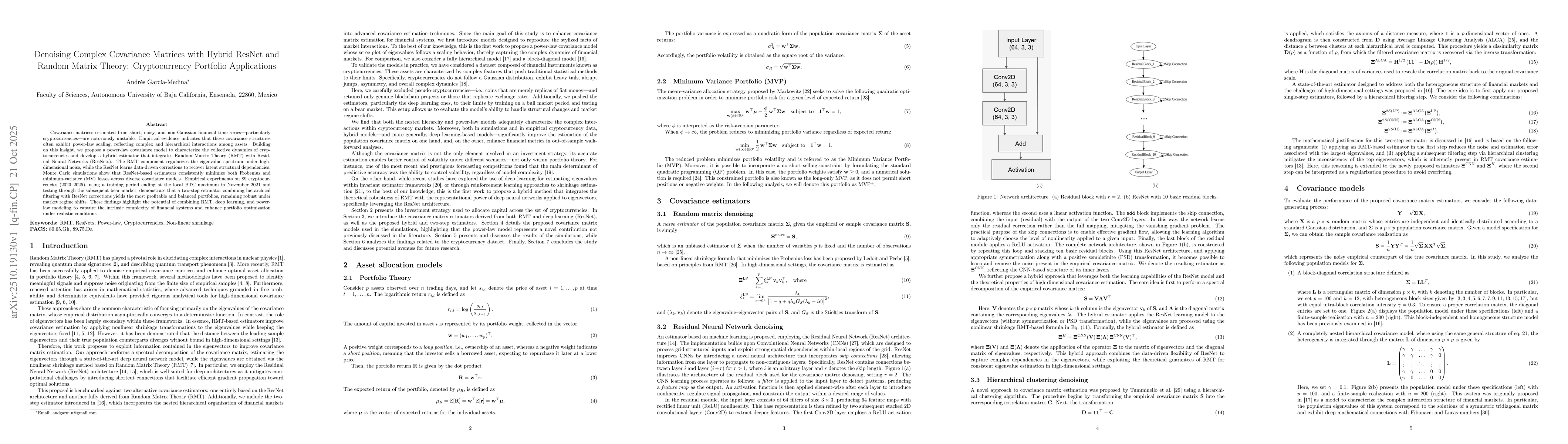

Denoising Complex Covariance Matrices with Hybrid ResNet and Random

Matrix Theory: Cryptocurrency Portfolio Applications

Covariance matrices estimated from short, noisy, and non-Gaussian financial time series-particularly cryptocurrencies-are notoriously unstable. Empirical evidence indicates that these covariance struc...