Academic Profile

Statistics

Similar Authors

Papers on arXiv

The convergence of the first order Euler scheme and an approximative variant thereof, along with convergence rates, are established for rough differential equations driven by c\`adl\`ag paths satisf...

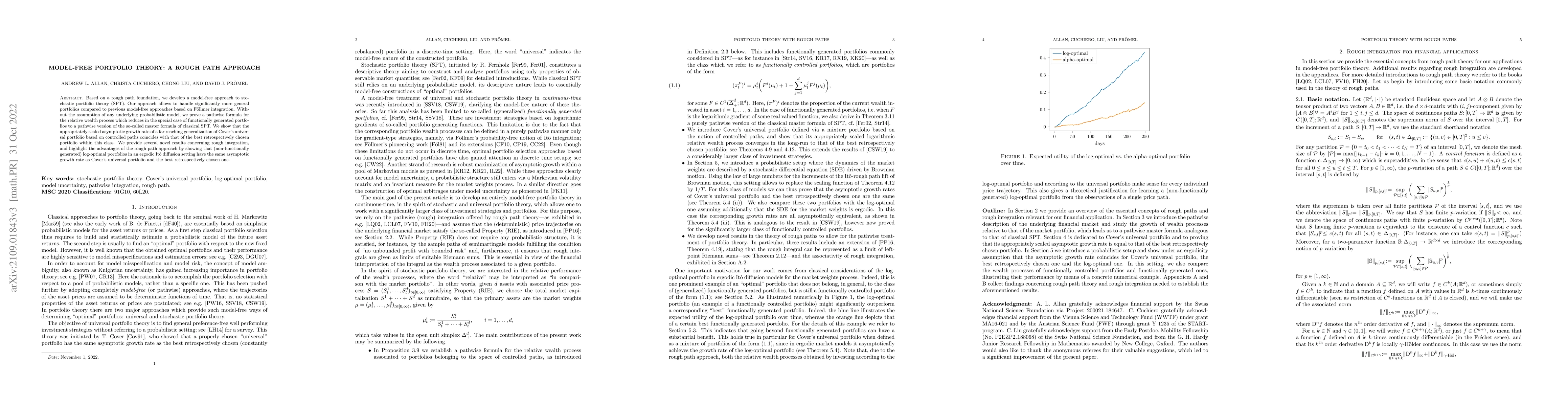

Based on a rough path foundation, we develop a model-free approach to stochastic portfolio theory (SPT). Our approach allows to handle significantly more general portfolios compared to previous mode...

We consider the filtering of continuous-time finite-state hidden Markov models, where the rate and observation matrices depend on unknown time-dependent parameters, for which no prior or stochastic ...

We study the problem of pathwise stochastic optimal control, where the optimization is performed for each fixed realisation of the driving noise, by phrasing the problem in terms of the optimal cont...

We present a new version of the stochastic sewing lemma, capable of handling multiple discontinuous control functions. This is then used to develop a theory of rough stochastic analysis in a c\`adl\`a...

We investigate the existence of a robust, i.e., continuous, representation of the conditional distribution in a stochastic filtering model for multidimensional correlated jump-diffusions. Even in the ...

Based on the theory of c\`adl\`ag rough paths, we develop a pathwise approach to analyze stability and approximation properties of portfolios along individual price trajectories generated by standard ...