Model-free Portfolio Theory: A Rough Path Approach

Publication

Metrics

AI Quick Summary

This paper develops a model-free stochastic portfolio theory using rough path techniques, allowing for more general portfolios than previous methods. It proves a pathwise formula for the relative wealth process and shows that log-optimal portfolios in an ergodic Itô diffusion setting achieve the same asymptotic growth rate as Cover's universal portfolio.

Paper Preview

Abstract

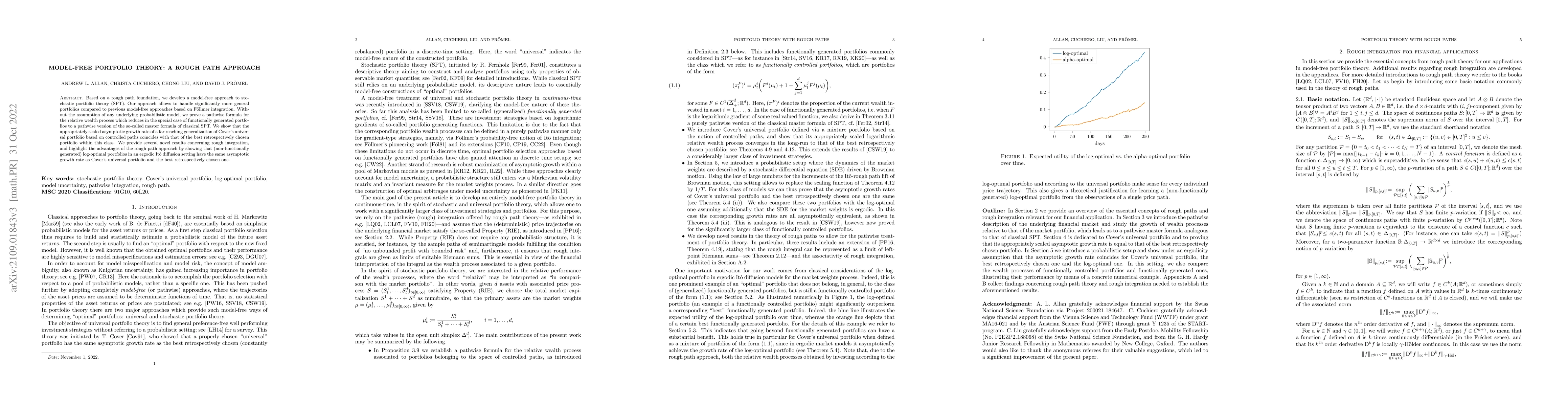

Based on a rough path foundation, we develop a model-free approach to stochastic portfolio theory (SPT). Our approach allows to handle significantly more general portfolios compared to previous model-free approaches based on F{\"o}llmer integration. Without the assumption of any underlying probabilistic model, we prove a pathwise formula for the relative wealth process which reduces in the special case of functionally generated portfolios to a pathwise version of the so-called master formula of classical SPT. We show that the appropriately scaled asymptotic growth rate of a far reaching generalization of Cover's universal portfolio based on controlled paths coincides with that of the best retrospectively chosen portfolio within this class. We provide several novel results concerning rough integration, and highlight the advantages of the rough path approach by showing that (non-functionally generated) log-optimal portfolios in an ergodic It{\^o} diffusion setting have the same asymptotic growth rate as Cover's universal portfolio and the best retrospectively chosen one.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0