Academic Profile

Statistics

Similar Authors

Papers on arXiv

Using a Besov topology on spaces of modelled distributions in the framework of Hairer's regularity structures, we prove the reconstruction theorem on these Besov spaces with negative regularity. The...

The classical Skorokhod embedding problem for a Brownian motion $W$ asks to find a stopping time $\tau$ so that $W_\tau$ is distributed according to a prescribed probability distribution $\mu$. Many...

The existence of unique solutions is established for rough differential equations (RDEs) with path-dependent coefficients and driven by c\`adl\`ag rough paths. Moreover, it is shown that the associa...

Besov spaces with dominating mixed smoothness, on the product of the real line and the torus as well as bounded domains, are studied. A characterization of these function spaces in terms of differen...

Quantitative estimates are derived, on the whole space, for the relative entropy between the joint law of random interacting particles and the tensorized law at the limiting systeme. The developed m...

The well-posedness and regularity properties of diffusion-aggregation equations, emerging from interacting particle systems, are established on the whole space for bounded interaction force kernels ...

The convergence of the first order Euler scheme and an approximative variant thereof, along with convergence rates, are established for rough differential equations driven by c\`adl\`ag paths satisf...

The well-posedness is established for multi-dimensional mean-field stochastic Volterra equations with Lipschitz continuous coefficients and allowing for singular kernels as well as for one-dimension...

We study a continuous-time version of the Hegelsmann--Krause model describing the opinion dynamics of interacting agents subject to random perturbations. Mathematical speaking, the opinion of agents...

The existence of weak solutions is established for stochastic Volterra equations with time-inhomogeneous coefficients allowing for general kernels in the drift and convolutional or bounded kernels i...

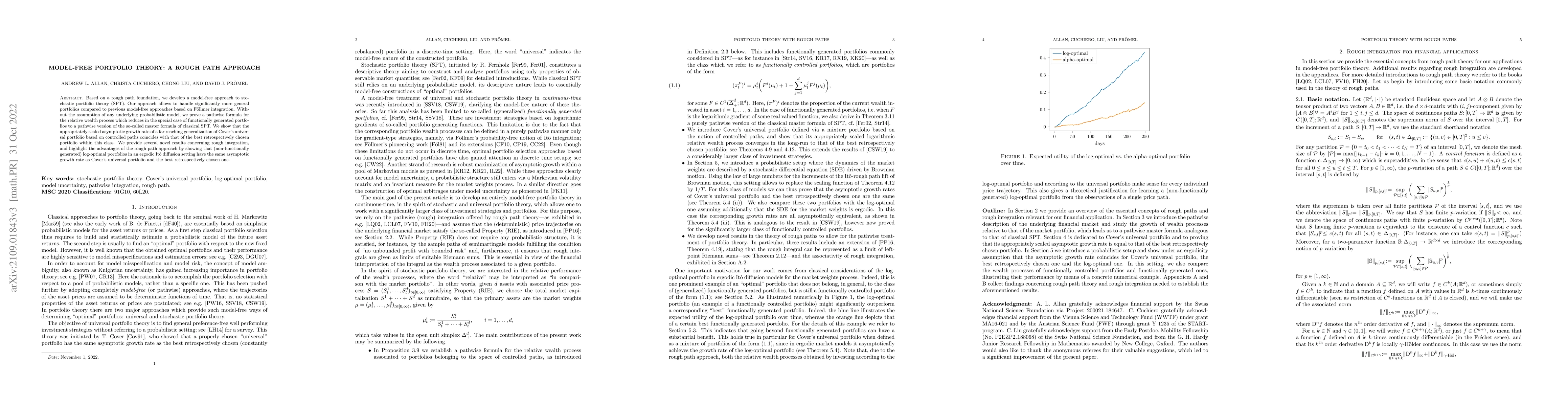

Based on a rough path foundation, we develop a model-free approach to stochastic portfolio theory (SPT). Our approach allows to handle significantly more general portfolios compared to previous mode...

We show that every $\mathbb{R}^d$-valued Sobolev path with regularity $\alpha$ and integrability $p$ can be lifted to a Sobolev rough path provided $\alpha < 1/p<1/3$. The novelty of our approach is...

We provide a very brief introduction to typical paths and the corresponding It\^o type integration. Relying on this robust It\^o integration, we prove an existence and uniqueness result for one-dime...

We introduce the space of rough paths with Sobolev regularity and the corresponding concept of controlled Sobolev paths. Based on these notions, we study rough path integration and rough differentia...

We obtain a dual representation of the Kantorovich functional defined for functions on the Skorokhod space using quotient sets. Our representation takes the form of a Choquet capacity generated by m...

Based on the notion of paracontrolled distributions, we provide existence and uniqueness results for rough Volterra equations of convolution type with potentially singular kernels and driven by the ...

We show that every $\mathbb{R}^d$-valued Sobolev path with regularity $\alpha$ and integrability $p$ can be lifted to a Sobolev rough path in the sense of T. Lyons provided $\alpha >1/p>0$. Moreover...

The canonical generalizations of two classical norms on Besov spaces are shown to be equivalent even in the case of non-linear Besov spaces, that is, function spaces consisting of functions taking v...

We provide a model-free pricing-hedging duality in continuous time. For a frictionless market consisting of $d$ risky assets with continuous price trajectories, we show that the purely analytic prob...

Stochastic Volterra equations (SVEs) serve as mathematical models for the time evolutions of random systems with memory effects and irregular behaviour. We introduce neural stochastic Volterra equatio...

We identify various classes of neural networks that are able to approximate continuous functions locally uniformly subject to fixed global linear growth constraints. For such neural networks the assoc...

Stochastic models with fractional Brownian motion as source of randomness have become popular since the early 2000s. Fractional Brownian motion (fBm) is a Gaussian process, whose covariance depends on...

We develop a general framework for pathwise stochastic integration that extends F\"ollmer's classical approach beyond gradient-type integrands and standard left-point Riemann sums and provides pathwis...

Based on the theory of c\`adl\`ag rough paths, we develop a pathwise approach to analyze stability and approximation properties of portfolios along individual price trajectories generated by standard ...

The universal approximation property uniformly with respect to weakly compact families of measures is established for several classes of neural networks. To that end, we prove that these neural networ...

We establish $L^p$-type universal approximation theorems for general and non-anticipative functionals on suitable rough path spaces, showing that linear functionals acting on signatures of time-extend...

We establish a universal approximation theorem for signatures of rough paths that are not necessarily weakly geometric. By extending the path with time and its rough path bracket terms, we prove that ...

We establish global universal approximation theorems on spaces of piecewise linear paths, stating that linear functionals of the corresponding signatures are dense with respect to $L^p$- and weighted ...

We prove the existence of weak solutions for distribution-dependent stochastic Volterra equations under linear growth and continuity conditions on the coefficients and mild regularity assumptions on t...