Academic Profile

Statistics

Similar Authors

Papers on arXiv

In the context of large financial markets we formulate the notion of \emph{no asymptotic free lunch with vanishing risk} (NAFLVR), under which we can prove a version of the fundamental theorem of as...

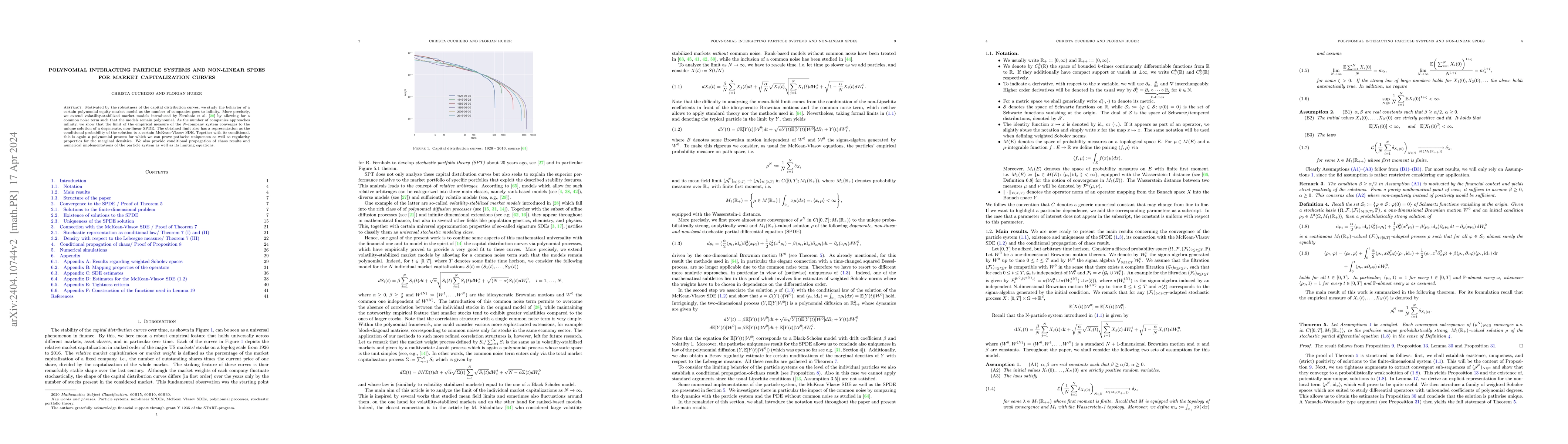

Motivated by the robustness of the capital distribution curves, we study the behavior of a certain polynomial equity market model as the number of companies goes to infinity. More precisely, we exte...

We study the class of continuous polynomial Volterra processes, which we define as solutions to stochastic Volterra equations driven by a continuous semimartingale with affine drift and quadratic di...

In the context of stochastic portfolio theory we introduce a novel class of portfolios which we call linear path-functional portfolios. These are portfolios which are determined by certain transform...

Generalized Feller theory provides an important analog to Feller theory beyond locally compact state spaces. This is very useful for solutions of certain stochastic partial differential equations, M...

We introduce so-called functional input neural networks defined on a possibly infinite dimensional weighted space with values also in a possibly infinite dimensional output space. To this end, we us...

We introduce and analyse infinite dimensional Wishart processes taking values in the cone $S^+_1(H)$ of positive self-adjoint trace class operators on a separable real Hilbert space $H$. Our main re...

Signature stochastic differential equations (SDEs) constitute a large class of stochastic processes, here driven by Brownian motions, whose characteristics are entire or real-analytic functions of t...

We consider a stochastic volatility model where the dynamics of the volatility are described by linear functions of the (time extended) signature of a primary underlying process, which is supposed t...

We introduce a framework that allows to employ (non-negative) measure-valued processes for energy market modeling, in particular for electricity and gas futures. Interpreting the process' spatial st...

We consider asset price models whose dynamics are described by linear functions of the (time extended) signature of a primary underlying process, which can range from a (market-inferred) Brownian mo...

We consider two implicit approximation schemes of the one-dimensional supercooled Stefan problem and prove their convergence, even in the presence of finite time blow-ups. All proofs are based on a ...

We introduce two kinds of risk measures with respect to some reference probability measure, which both allow for a certain order structure and domination property. Analyzing their relation to each o...

We introduce a class of measure-valued processes, which -- in analogy to their finite dimensional counterparts -- will be called measure-valued polynomial diffusions. We show the so-called moment fo...

We consider the problem faced by a central bank which bails out distressed financial institutions that pose systemic risk to the banking sector. In a structural default model with mutual obligations...

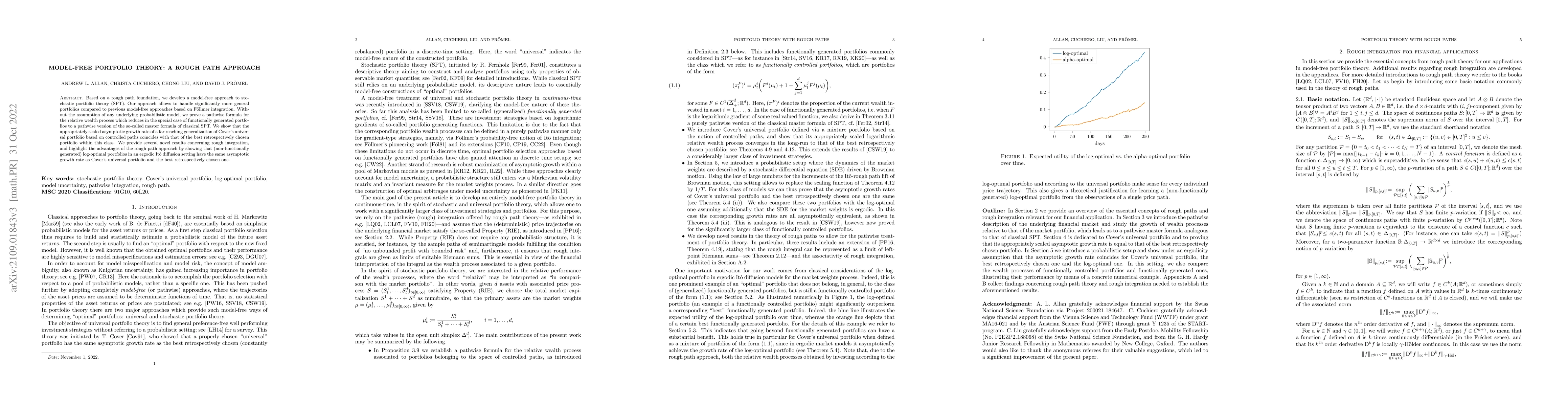

Based on a rough path foundation, we develop a model-free approach to stochastic portfolio theory (SPT). Our approach allows to handle significantly more general portfolios compared to previous mode...

A new explanation of geometric nature of the reservoir computing phenomenon is presented. Reservoir computing is understood in the literature as the possibility of approximating input/output systems...

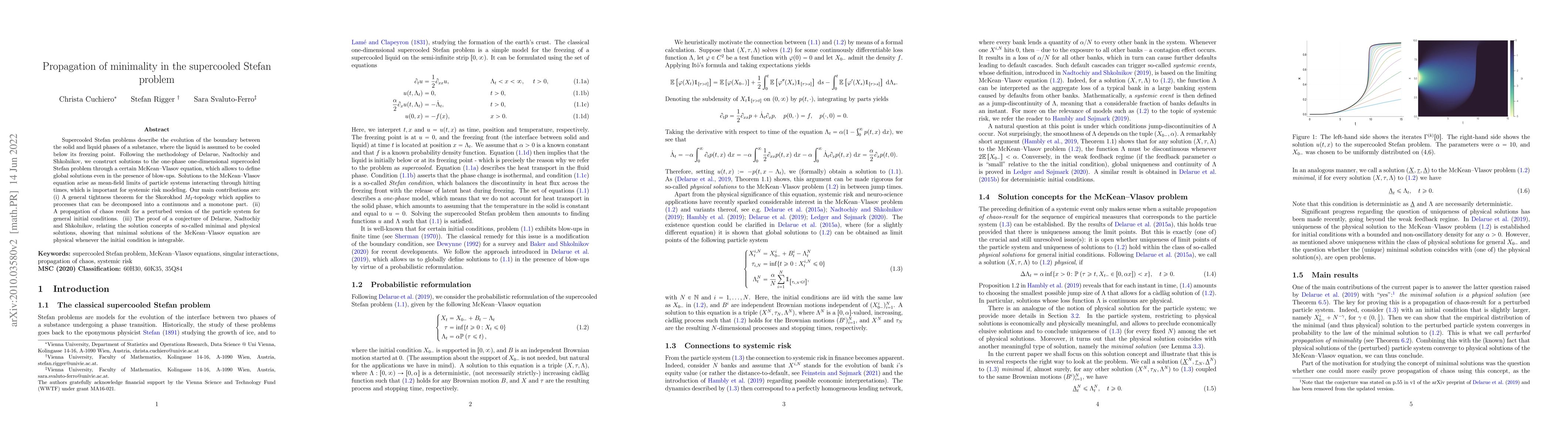

Supercooled Stefan problems describe the evolution of the boundary between the solid and liquid phases of a substance, where the liquid is assumed to be cooled below its freezing point. Following th...

We introduce polynomial processes taking values in an arbitrary Banach space $B$ via their infinitesimal generator $L$ and the associated martingale problem. We obtain two representations of the (co...

We obtain general weak existence and stability results for stochastic convolution equations with jumps under mild regularity assumptions, allowing for non-Lipschitz coefficients and singular kernels...

We consider stochastic partial differential equations appearing as Markovian lifts of matrix valued (affine) Volterra type processes from the point of view of the generalized Feller property (see e....

The paper presents a Bayesian framework for the calibration of financial models using neural stochastic differential equations (neural SDEs). The method is based on the specification of a prior distri...

We introduce a class of jump-diffusions, called holomorphic, of which the well-known classes of affine and polynomial processes are particular instances. The defining property concerns the extended ge...

We study a new class of McKean-Vlasov stochastic differential equations (SDEs), possibly with common noise, applying the theory of time-inhomogeneous polynomial processes. The drift and volatility coe...

We derive a functional It\^o-formula for non-anticipative maps of rough paths, based on the approximation properties of the signature of c\`adl\`ag rough paths. This result is a functional extension o...

We establish a quantitative version of the classical Halmos-Savage theorem for convex sets of probability measures and its dual counterpart, generalizing previous quantitative versions. These results ...