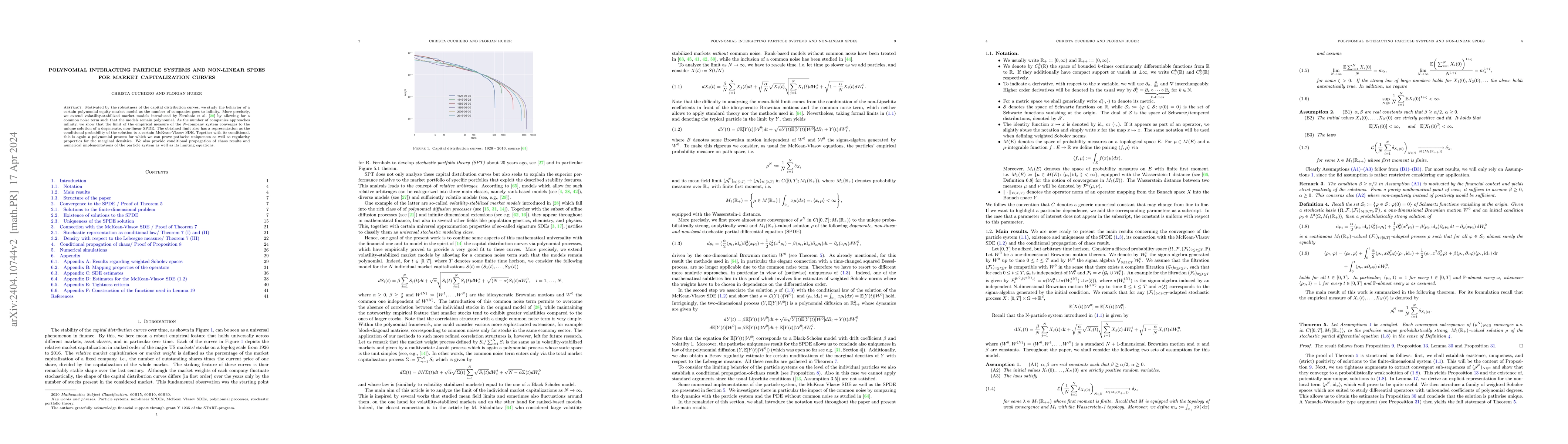

Polynomial interacting particle systems and non-linear SPDEs for market capitalization curves

Publication

Metrics

AI Quick Summary

This paper investigates the behavior of a polynomial equity market model as the number of companies tends to infinity, showing its convergence to a unique solution of a degenerate, non-linear stochastic partial differential equation (SPDE). It also establishes pathwise uniqueness and regularity for marginal densities, along with conditional propagation of chaos and numerical implementations.

Paper Preview

Abstract

Motivated by the robustness of the capital distribution curves, we study the behavior of a certain polynomial equity market model as the number of companies goes to infinity. More precisely, we extend volatility-stabilized market models introduced by Fernholz et al. by allowing for a common noise term such that the models remain polynomial. As the number of companies approaches infinity, we show that the limit of the empirical measure of the $N$-company system converges to the unique solution of a degenerate, non-linear SPDE. The obtained limit also has a representation as the conditional probability of the solution to a certain McKean-Vlasov SDE. Together with its conditional, this is again a polynomial process for which we can prove pathwise uniqueness as well as regularity properties for the marginal densities. We also provide conditional propagation of chaos results and numerical implementations of the particle system as well as its limiting equations.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0