Academic Profile

Statistics

Similar Authors

Papers on arXiv

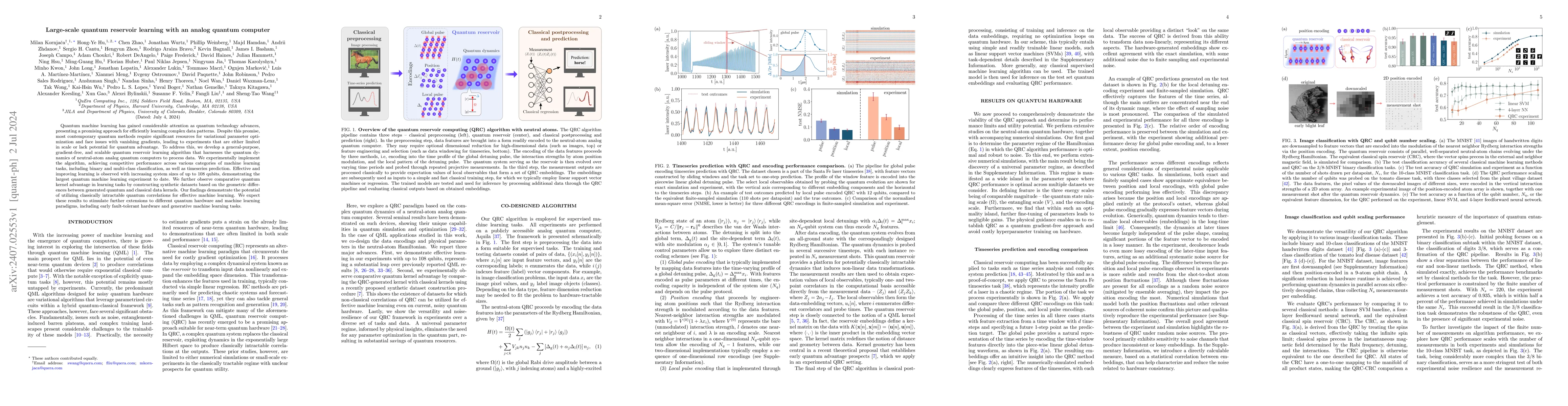

Quantum machine learning has gained considerable attention as quantum technology advances, presenting a promising approach for efficiently learning complex data patterns. Despite this promise, most ...

We investigate Markovian lifts of stochastic Volterra equations (SVEs) with completely monotone kernels and general coefficients within a class of weighted Sobolev spaces. Our primary focus is devel...

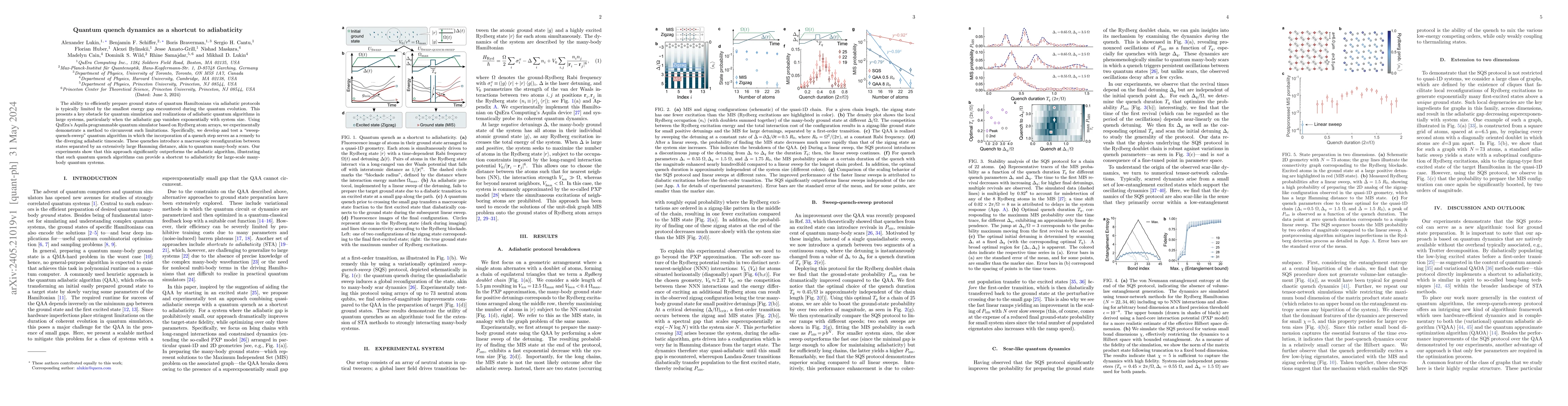

The ability to efficiently prepare ground states of quantum Hamiltonians via adiabatic protocols is typically limited by the smallest energy gap encountered during the quantum evolution. This presen...

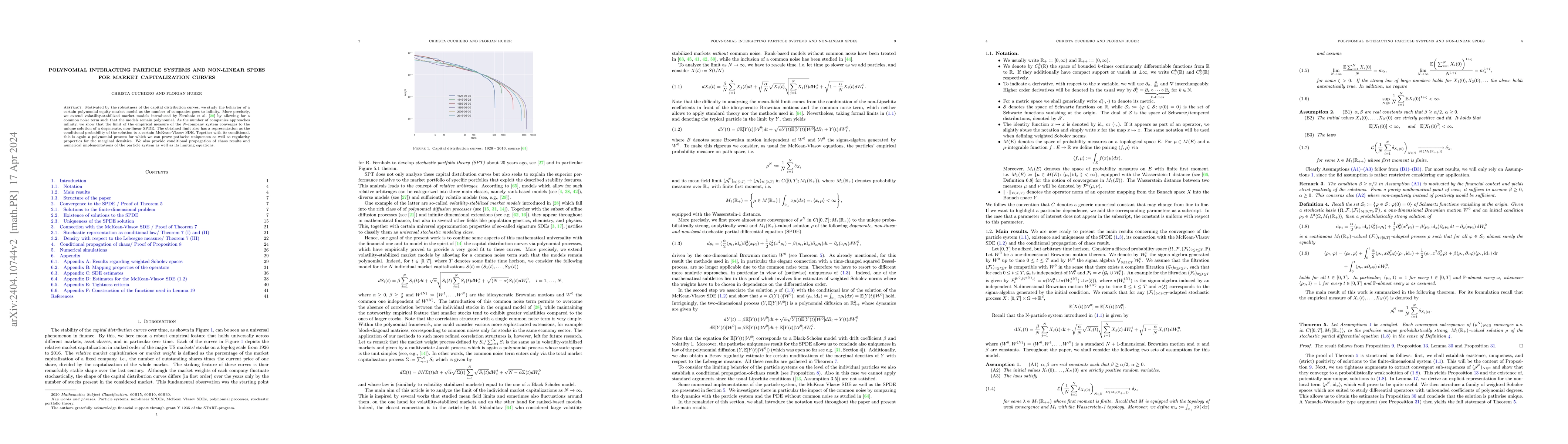

Motivated by the robustness of the capital distribution curves, we study the behavior of a certain polynomial equity market model as the number of companies goes to infinity. More precisely, we exte...

While a variety of methods offer good yield prediction on histogrammed remote sensing data, vision Transformers are only sparsely represented in the literature. The Convolution vision Transformer (C...

Timely information about the state of regional economies can be essential for planning, implementing and evaluating locally targeted economic policies. However, European regional accounts for output...

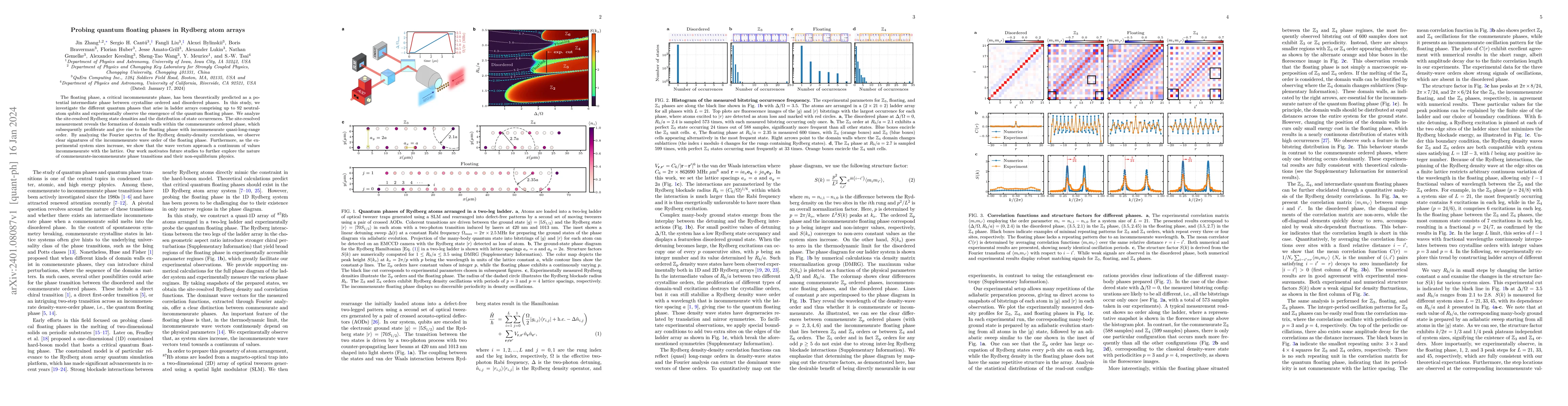

The floating phase, a critical incommensurate phase, has been theoretically predicted as a potential intermediate phase between crystalline ordered and disordered phases. In this study, we investiga...

This paper proposes a new Bayesian machine learning model that can be applied to large datasets arising in macroeconomics. Our framework sums over many simple two-component location mixtures. The tr...

Bayesian predictive synthesis (BPS) provides a method for combining multiple predictive distributions based on agent/expert opinion analysis theory and encompasses a range of existing density foreca...

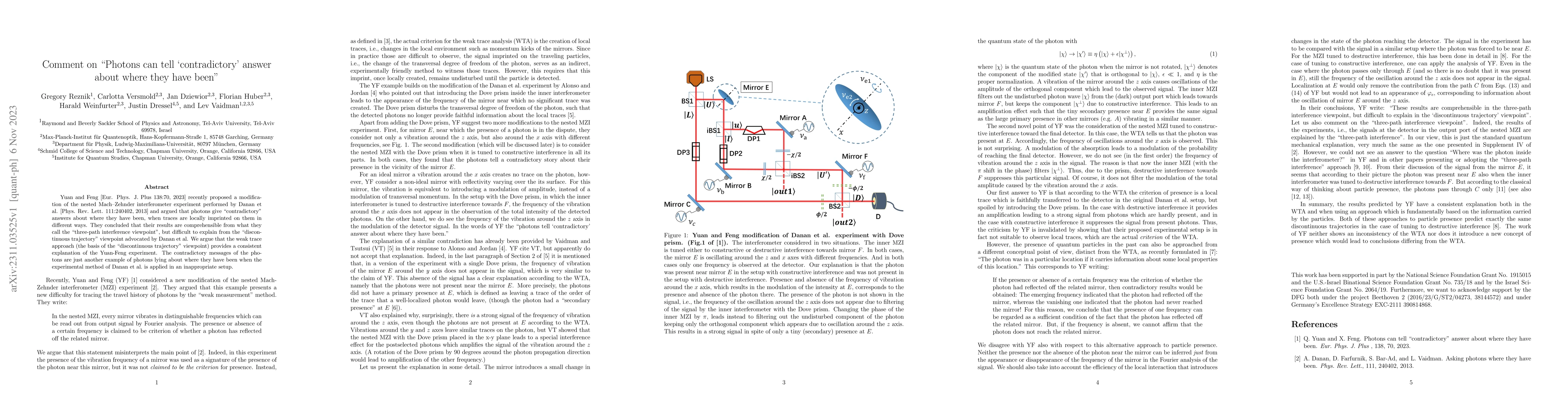

Yuan and Feng [Eur. Phys. J. Plus 138:70, 2023] recently proposed a modification of the nested Mach-Zehnder interferometer experiment performed by Danan et al. [Phys. Rev. Lett. 111:240402, 2013] an...

The neutral-atom quantum computer "Aquila" is QuEra's latest device available through the Braket cloud service on Amazon Web Services (AWS). Aquila is a "field-programmable qubit array" (FPQA) opera...

The shocks which hit macroeconomic models such as Vector Autoregressions (VARs) have the potential to be non-Gaussian, exhibiting asymmetries and fat tails. This consideration motivates the VAR deve...

Model mis-specification in multivariate econometric models can strongly influence quantities of interest such as structural parameters, forecast distributions or responses to structural shocks, even...

Explainability in yield prediction helps us fully explore the potential of machine learning models that are already able to achieve high accuracy for a variety of yield prediction scenarios. The dat...

We extend the existing growth-at-risk (GaR) literature by examining a long time period of 130 years in a time-varying parameter regression model. We identify several important insights for policymak...

Modeling and predicting extreme movements in GDP is notoriously difficult and the selection of appropriate covariates and/or possible forms of nonlinearities are key in obtaining precise forecasts. ...

The Bayesian statistical paradigm provides a principled and coherent approach to probabilistic forecasting. Uncertainty about all unknowns that characterize any forecasting problem -- model, paramet...

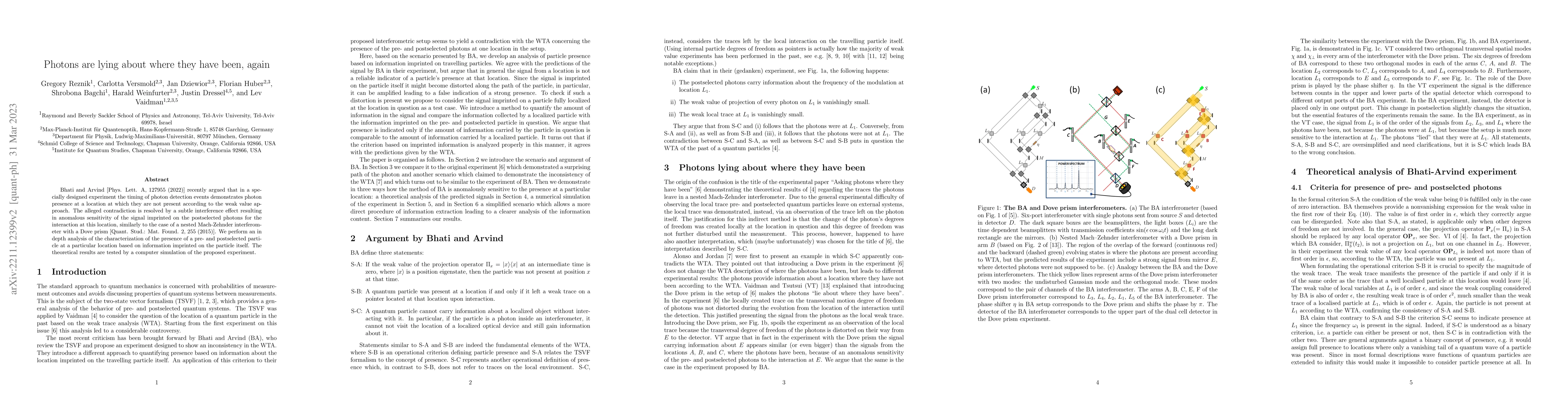

Bhati and Arvind [Phys. Lett. A, 127955 (2022)] recently argued that in a specially designed experiment the timing of photon detection events demonstrates photon presence at a location at which they...

Macroeconomic data is characterized by a limited number of observations (small T), many time series (big K) but also by featuring temporal dependence. Neural networks, by contrast, are designed for ...

In light of widespread evidence of parameter instability in macroeconomic models, many time-varying parameter (TVP) models have been proposed. This paper proposes a nonparametric TVP-VAR model using...

Accurate prediction of crop yield before harvest is of great importance for crop logistics, market planning, and food distribution around the world. Yield prediction requires monitoring of phenologi...

In this paper, we forecast euro area inflation and its main components using an econometric model which exploits a massive number of time series on survey expectations for the European Commission's ...

Not all real-world data are labeled, and when labels are not available, it is often costly to obtain them. Moreover, as many algorithms suffer from the curse of dimensionality, reducing the features...

The relationship between inflation and predictors such as unemployment is potentially nonlinear with a strength that varies over time, and prediction errors error may be subject to large, asymmetric...

We investigate the consequences of legal rulings on the conduct of monetary policy. Several unconventional monetary policy measures of the European Central Bank have come under scrutiny before natio...

The existence of global nonnegative martingale solutions to cross-diffusion systems of Shigesada-Kawasaki-Teramoto type with multiplicative noise is proven. The model describes the stochastic segreg...

We develop a non-parametric multivariate time series model that remains agnostic on the precise relationship between a (possibly) large set of macroeconomic time series and their lagged values. The ...

We develop a Bayesian non-parametric quantile panel regression model. Within each quantile, the response function is a convex combination of a linear model and a non-linear function, which we approx...

Macroeconomists using large datasets often face the choice of working with either a large Vector Autoregression (VAR) or a factor model. In this paper, we develop methods for combining the two using...

Panel Vector Autoregressions (PVARs) are a popular tool for analyzing multi-country datasets. However, the number of estimated parameters can be enormous, leading to computational and statistical is...

Time-varying parameter (TVP) regressions commonly assume that time-variation in the coefficients is determined by a simple stochastic process such as a random walk. While such models are capable of ...

The existence of global nonnegative martingale solutions to a cross-diffusion system of Shigesada-Kawasaki-Teramoto type with multiplicative noise is proven. The model describes the segregation dyna...

In this paper, we assess whether using non-linear dimension reduction techniques pays off for forecasting inflation in real-time. Several recent methods from the machine learning literature are adop...

In line with the recent policy discussion on the use of macroprudential measures to respond to cross-border risks arising from capital flows, this paper tries to quantify to what extent macroprudent...

This paper develops Bayesian econometric methods for posterior inference in non-parametric mixed frequency VARs using additive regression trees. We argue that regression tree models are ideally suit...

The main goal of this work is to relate weak and pathwise mild solutions for parabolic quasilinear stochastic partial differential equations (SPDEs). Extending in a suitable way techniques from the ...

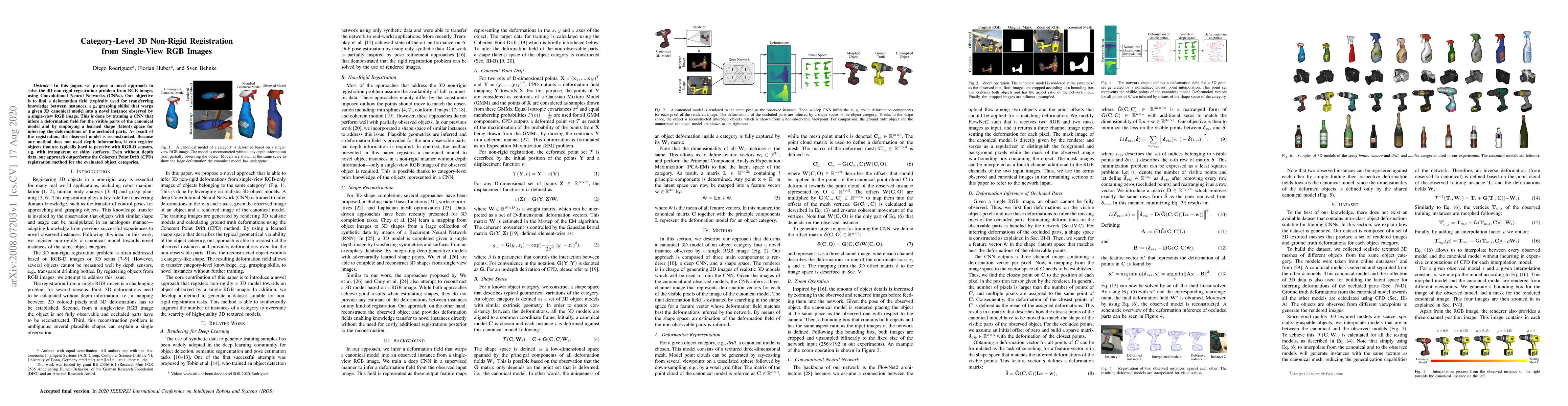

In this paper, we propose a novel approach to solve the 3D non-rigid registration problem from RGB images using Convolutional Neural Networks (CNNs). Our objective is to find a deformation field (ty...

The COVID-19 recession that started in March 2020 led to an unprecedented decline in economic activity across the globe. To fight this recession, policy makers in central banks engaged in expansiona...

Vector autoregressive (VAR) models assume linearity between the endogenous variables and their lags. This assumption might be overly restrictive and could have a deleterious impact on forecasting ac...

Successful forecasting models strike a balance between parsimony and flexibility. This is often achieved by employing suitable shrinkage priors that penalize model complexity but also reward model f...

Time-varying parameter (TVP) regression models can involve a huge number of coefficients. Careful prior elicitation is required to yield sensible posterior and predictive inferences. In addition, th...

Researchers increasingly wish to estimate time-varying parameter (TVP) regressions which involve a large number of explanatory variables. Including prior information to mitigate over-parameterizatio...

This paper develops a dynamic factor model that uses euro area (EA) country-specific information on output and inflation to estimate an area-wide measure of the output gap. Our model assumes that ou...

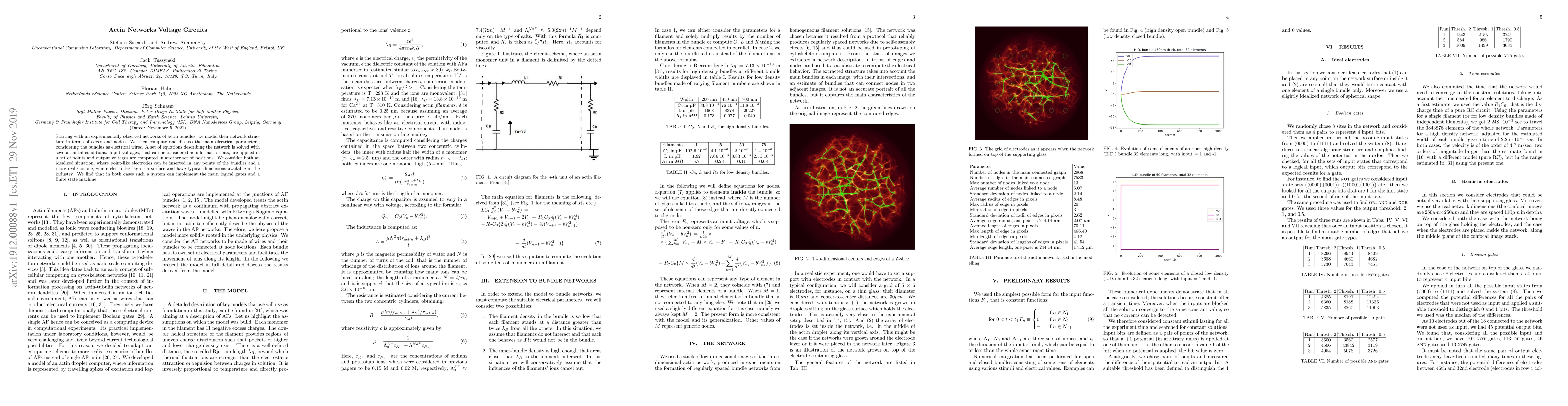

Starting with an experimentally observed networks of actin bundles, we model their network structure in terms of edges and nodes. We then compute and discuss the main electrical parameters, consider...

Time-varying parameter (TVP) models have the potential to be over-parameterized, particularly when the number of variables in the model is large. Global-local priors are increasingly used to induce ...

We forecast S&P 500 excess returns using a flexible Bayesian econometric state space model with non-Gaussian features at several levels. More precisely, we control for overparameterization via novel...

We assess the relationship between model size and complexity in the time-varying parameter VAR framework via thorough predictive exercises for the Euro Area, the United Kingdom and the United States...

We develop a Bayesian vector autoregressive (VAR) model with multivariate stochastic volatility that is capable of handling vast dimensional information sets. Three features are introduced to permit...

This paper analyzes nonlinearities in the international transmission of financial shocks originating in the US. To do so, we develop a flexible nonlinear multi-country model. Our framework is capable ...

The discovery and identification of molecules in biological and environmental samples is crucial for advancing biomedical and chemical sciences. Tandem mass spectrometry (MS/MS) is the leading techniq...

We propose a method to learn the nonlinear impulse responses to structural shocks using neural networks, and apply it to uncover the effects of US financial shocks. The results reveal substantial asym...

We provide a framework for efficiently estimating impulse response functions with Local Projections (LPs). Our approach offers a Bayesian treatment for LPs with Instrumental Variables, accommodating m...

We study the distributional implications of uncertainty shocks by developing a model that links macroeconomic aggregates to the US distribution of earnings and consumption. We find that: initially, th...

Commonly used priors for Vector Autoregressions (VARs) induce shrinkage on the autoregressive coefficients. Introducing shrinkage on the error covariance matrix is sometimes done but, in the vast majo...

Realizing universal fault-tolerant quantum computation is a key goal in quantum information science. By encoding quantum information into logical qubits utilizing quantum error correcting codes, physi...

We derive a noise term to account for fluctuation corrections based on the particle system approximation for the n-species Shigesada-Kawasaki-Teramoto (SKT) system. For the resulting system of stochas...

This paper proposes a Vector Autoregression augmented with nonlinear factors that are modeled nonparametrically using regression trees. There are four main advantages of our model. First, modeling pot...

We study double descent and benign overfitting in macroeconomic forecasting. We document that double-descent risk curves arise in standard macroeconomic datasets that are driven by a small number of l...

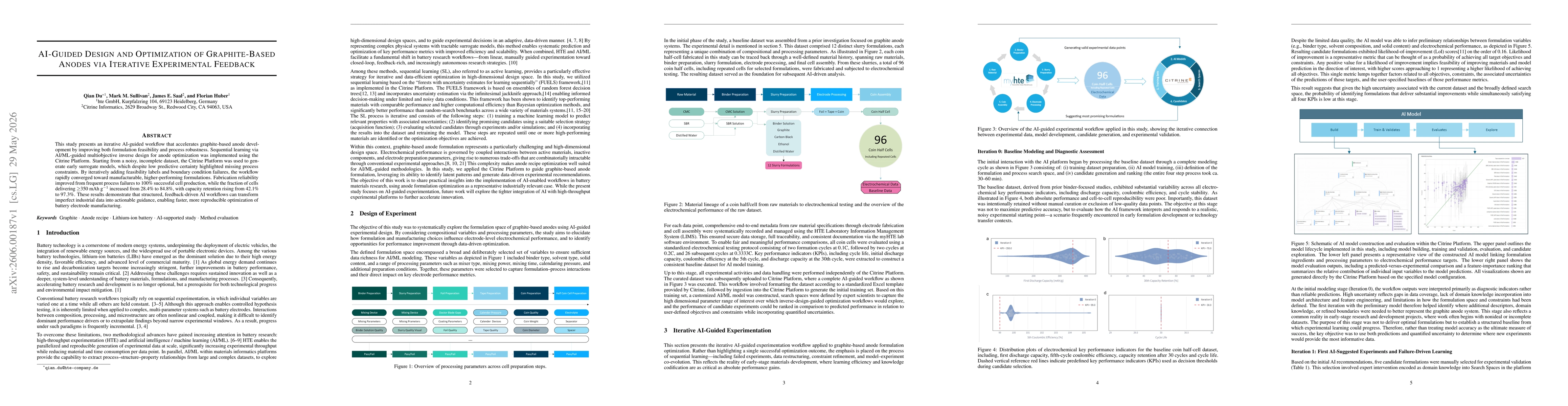

This study presents an iterative AI-guided workflow that accelerates graphite-based anode development by improving both formulation feasibility and process robustness. Sequential learning via AI/ML-gu...