Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider the dynamics and the interactions of multiple reinforcement learning optimal execution trading agents interacting with a reactive Agent-Based Model (ABM) of a financial market in event t...

Portfolio management is a multi-period multi-objective optimisation problem subject to a wide range of constraints. However, in practice, portfolio management is treated as a single-period problem p...

We consider the learning dynamics of a single reinforcement learning optimal execution trading agent when it interacts with an event driven agent-based financial market model. Trading takes place as...

Online portfolio selection is an integral componentof wealth management. The fundamental undertaking is tomaximise returns while minimising risk given investor con-straints. We aim to examine and im...

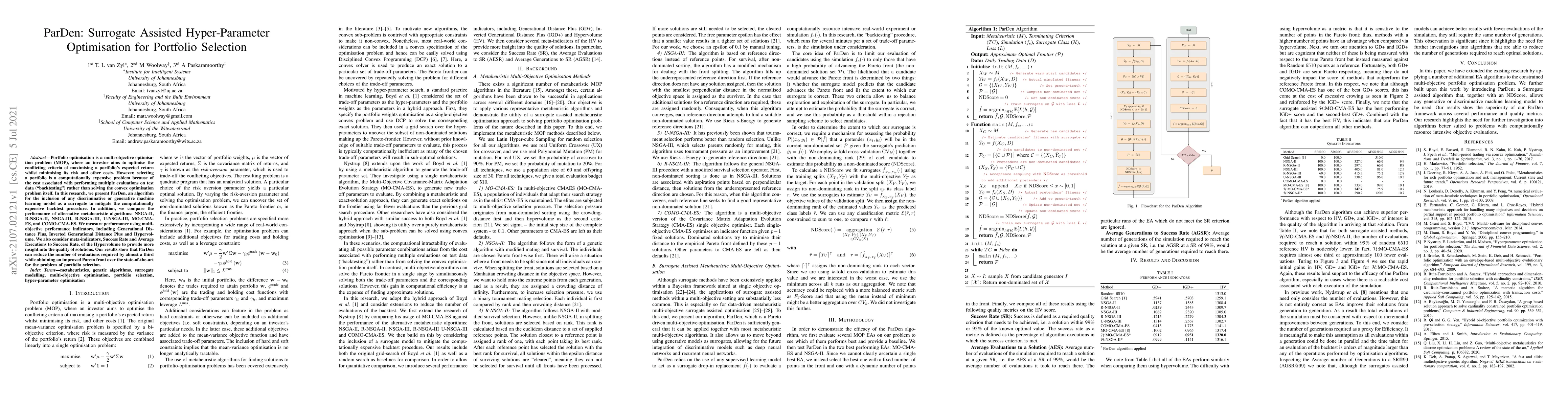

Portfolio optimisation is a multi-objective optimisation problem (MOP), where an investor aims to optimise the conflicting criteria of maximising a portfolio's expected return whilst minimising its ...

Mean-variance portfolio decisions that combine prediction and optimisation have been shown to have poor empirical performance. Here, we consider the performance of various shrinkage methods by their...

The artificial segmentation of an investment management process into a workflow with silos of offline human operators can restrict silos from collectively and adaptively pursuing a unified optimal i...

Backtests on historical data are the basis for practical evaluations of portfolio selection rules, but their reliability is often limited by reliance on a single sample path. This can lead to high est...