Academic Profile

Statistics

Similar Authors

Papers on arXiv

We use empirical Bayes (EB) to mine data on 140,000 long-short strategies constructed from accounting ratios, past returns, and ticker symbols. This "high-throughput asset pricing" produces out-of-s...

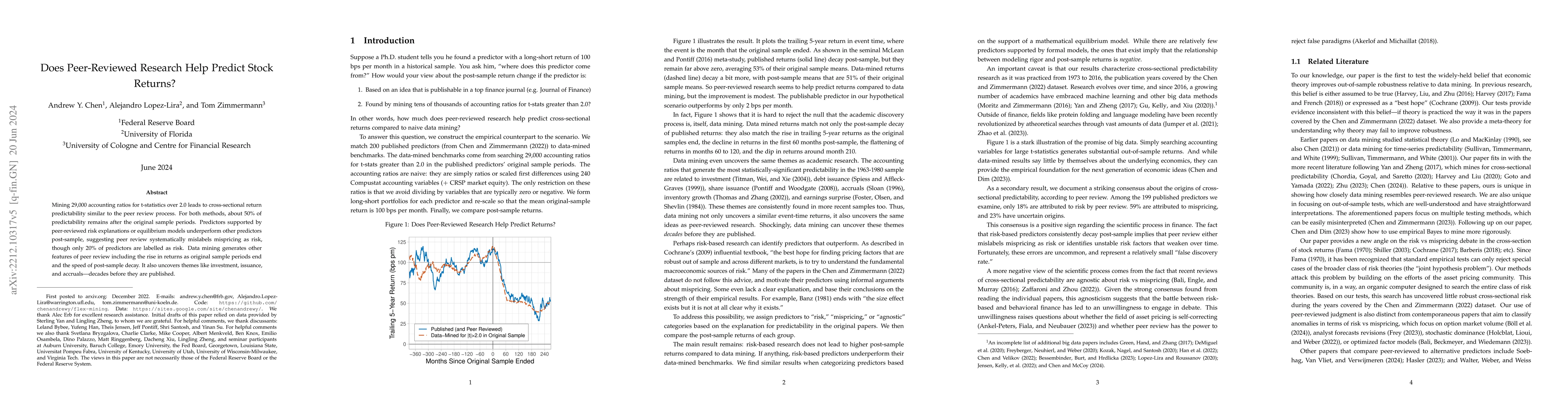

Mining 29,000 accounting ratios for t-statistics over 2.0 leads to cross-sectional return predictability similar to the peer review process. For both methods, about 50% of predictability remains aft...

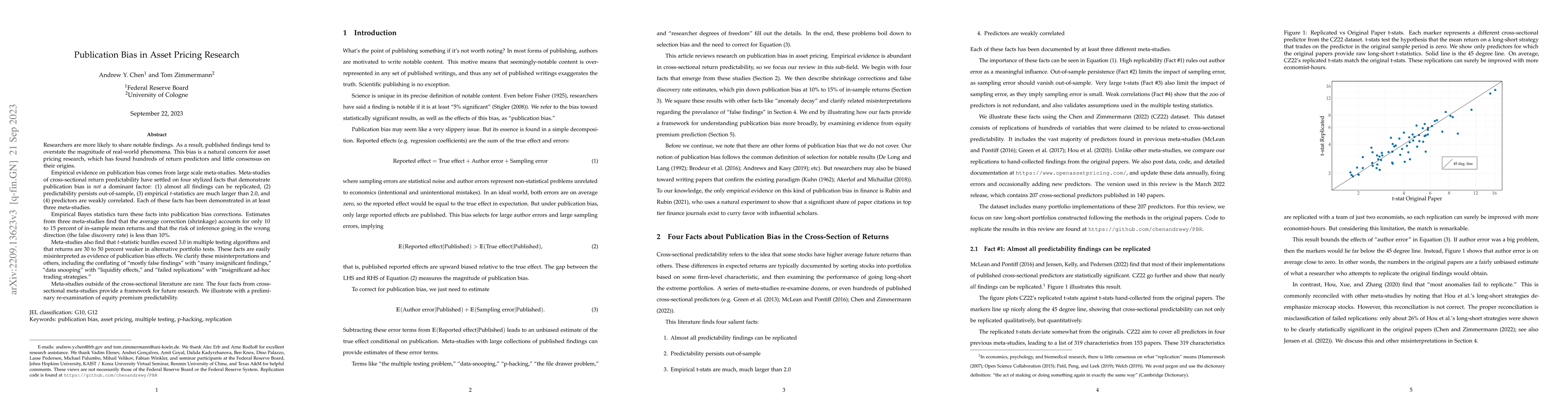

Researchers are more likely to share notable findings. As a result, published findings tend to overstate the magnitude of real-world phenomena. This bias is a natural concern for asset pricing resea...

We characterize the structure and origins of missingness for 159 cross-sectional return predictors and study missing value handling for portfolios constructed using machine learning. Simply imputing...

I develop simple and intuitive bounds for the false discovery rate (FDR) in cross-sectional return predictability publications. The bounds can be calculated by plugging in summary statistics from pr...

Many scholars have called for raising statistical hurdles to guard against false discoveries in academic publications. I show these calls may be difficult to justify empirically. Published data exhi...

Composite materials are used across engineering applications for their superior mechanical performance, a result of efficient load transfer between the structure and matrix phases. However, the inhere...

For many economic questions, the empirical results are not interesting unless they are strong. For these questions, theorizing before the results are known is not always optimal. Instead, the optimal ...

Magnetic remote actuation of soft materials has been demonstrated at the macroscale using hard-magnetic particles for applications such as transforming materials and medical robots. However, due to ma...

AI stocks trade at extraordinary valuations. We develop an asset pricing model in which investors use AI stocks to hedge against an AI singularity that displaces their consumption. Because markets are...

This paper examines about 200 published long-short anomaly equity portfolios (Chen and Zimmermann, 2022). Over the period through 2005 (December 2005 and earlier) and across all stocks, their median z...