Academic Profile

Statistics

Similar Authors

Papers on arXiv

Let $X_1,\,X_2,\,\ldots,\,X_N$, $N\in\mathbb{N}$ be independent but not necessarily identically distributed discrete and integer-valued random variables. Assume that $X_1\geqslant m_1$, $X_2\geqslan...

This survey article is dedicated to the life of the famous American economist H. Markowitz (1927--2023). We do revisit the main statements of the portfolio selection theory in terms of mathematical ...

In this work, we propose a simplification of the Pollaczek-Khinchine formula for the ultimate time survival (or ruin) probability calculation in exchange for a few assumptions on the random variable...

In ruin theory, the net profit condition intuitively means that the incurred random claims on average do not occur more often than premiums are gained. The breach of the net profit condition causes ...

This article gives a probabilistic overview of the widely used method of default probability estimation proposed by K. Pluto and D. Tasche. There are listed detailed assumptions and derivation of th...

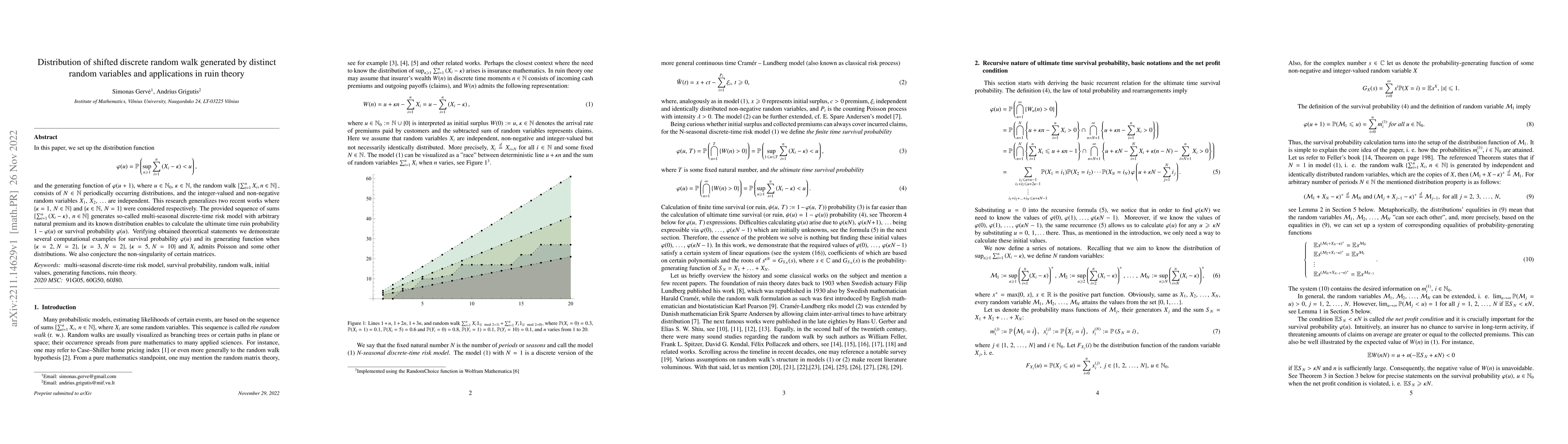

In this paper, we set up the distribution function $$ \varphi(u)=\mathbb{P}\left(\sup_{n\geqslant 1}\sum_{i=1}^{n}\left(X_i-\kappa\right)<u\right), $$ and the generating function of $\varphi(u+1)$, ...

In this work we set up the generating function of the ultimate time survival probability $\varphi(u+1)$, where $$\varphi(u)=\mathbb{P}\left(\sup_{n\geqslant 1}\sum_{i=1}^{n}\left(X_i-\kappa\right)<u...

In this work we set up the distribution function of $\mathcal{M}:=\sup_{n\geqslant1}\sum_{i=1}^{n}{(Z_i-1)}$, where the random walk $\sum_{i=1}^{n}Z_i, n\in\mathbb{N},$ is generated by $N$ periodica...

In this paper we investigate the positivity property of the real part of logarithmic derivative of the Riemann $\xi$-function for $1/2<\sigma<1$ and sufficiently large $t$. We give an explicit upper...

This paper proceeds an approximate calculation of ultimate time survival probability for bi-seasonal discrete time risk model when premium rate equals two. The same model with income rate equal to o...

We analyze $2\times 2$ Hankel-like determinants $D_n$ that arise in the initial values problem for the ultimate time survival probability $\varphi(u)$ in a homogeneous discrete time risk model $W(n)...

The mathematical essence in life insurance spins around the search of the nu\-me\-ri\-cal characteristics of the random variables $T_x$, $\nu^{T_x}$, $T_x\nu^{T_x}$, etc., where $\nu$ (deterministic) ...

Let ${\pmb b}=\{b_0,\,b_1,\,\ldots\}$ be the known sequence of numbers such that $b_0\neq0$. In this work, we develop methods to find another sequence ${\pmb a}=\{a_0,\,a_1,\,\ldots\}$ that is related...

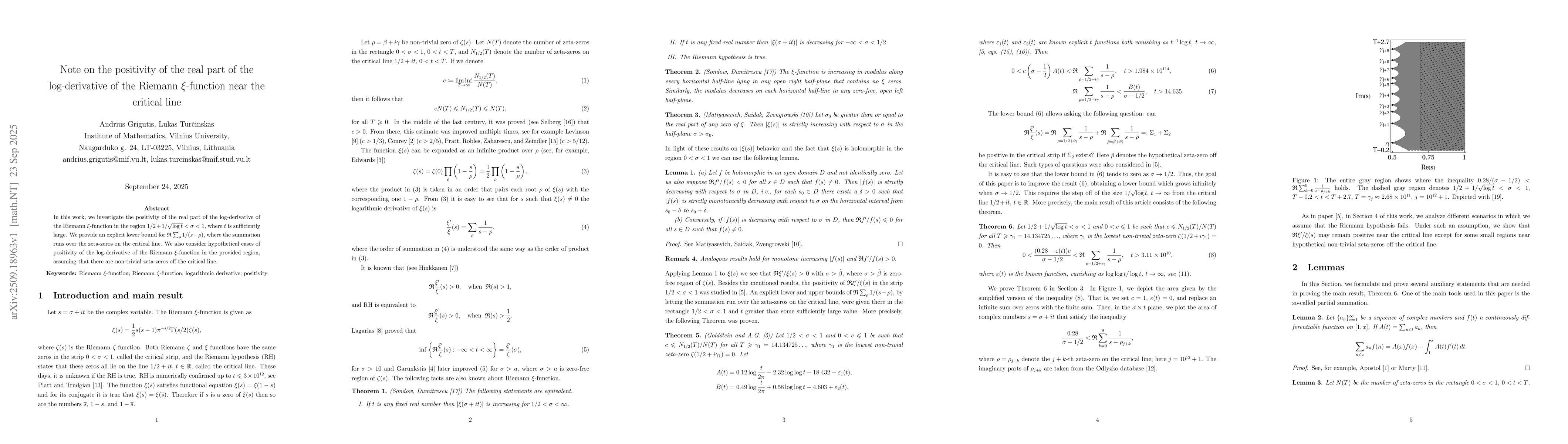

In this work, we investigate the positivity of the real part of the log-derivative of the Riemann $\xi$-function in the region $1/2+1/\sqrt{\log t}<\sigma<1$, where $t$ is sufficiently large. We provi...

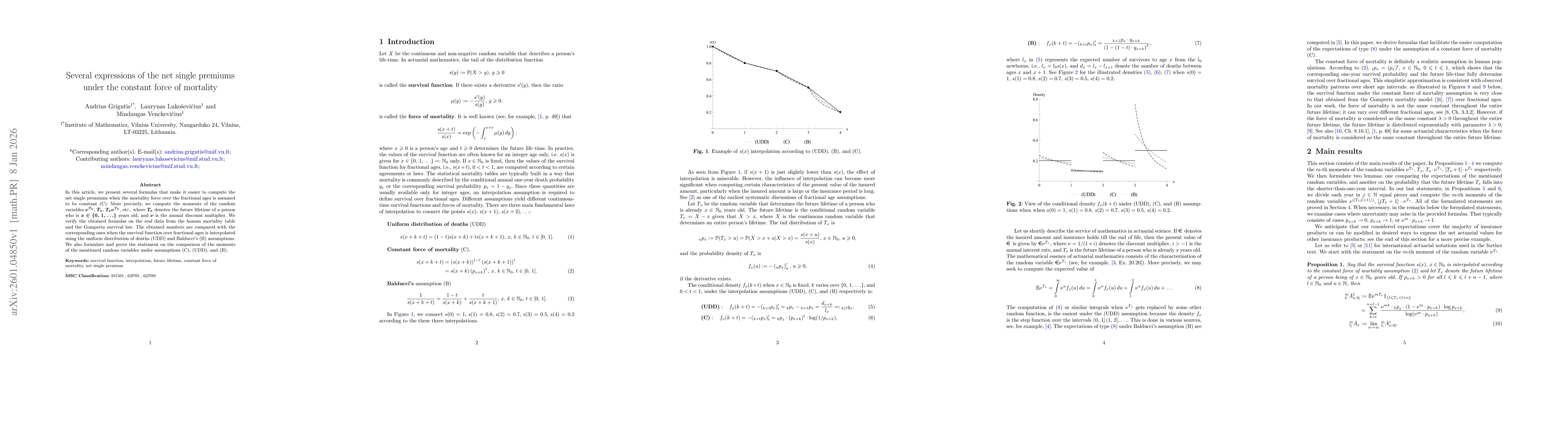

In this article, we present several formulas that make it easier to compute the net single premiums when the mortality force over the fractional ages is assumed to be constant (C). More precisely, we ...

Let $X_1,\,X_2,\,\ldots,\,X_N$, $N\in\mathbb N$ be independent, discrete, integer-valued random variables. Assume that $X_j\geqslant m_j$ almost surely for each $j=1,\,2,\,\ldots,\,N$, where $m_1,\,m_...