Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper studies pricing derivatives in an age-dependent semi-Markov modulated market. We consider a financial market where the asset price dynamics follow a regime switching geometric Brownian mo...

In this paper, a multidimensional system of parabolic partial differential equations arising in European option pricing under a regime-switching market model is studied in details. For solving that ...

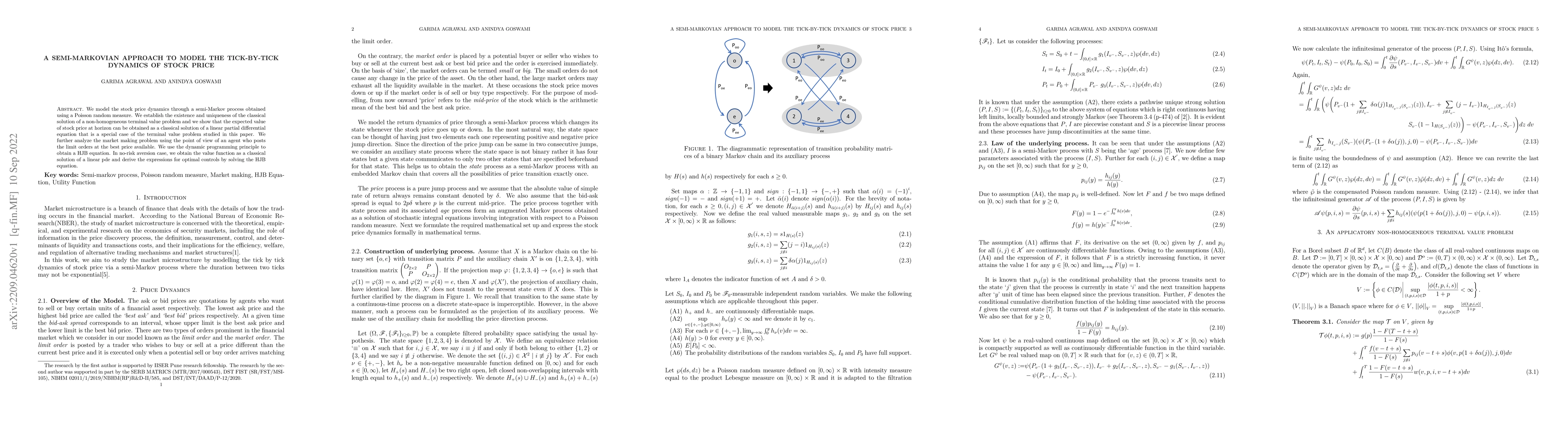

We model the stock price dynamics through a semi-Markov process obtained using a Poisson random measure. We establish the existence and uniqueness of the classical solution of a non-homogeneous term...

Fourth-order accurate compact schemes for variable coefficient convection diffusion equations are considered. A sufficient condition for the stability of the fully discrete problem is derived using ...

We consider a class of semi-Markov processes (SMP) such that the embedded discrete time Markov chain may be non-homogeneous. The corresponding augmented processes are represented as semi-martingales...

In the regime switching extension of Black-Scholes-Merton model of asset price dynamics, one assumes that the volatility coefficient evolves as a hidden pure jump process. Under the assumption of Ma...

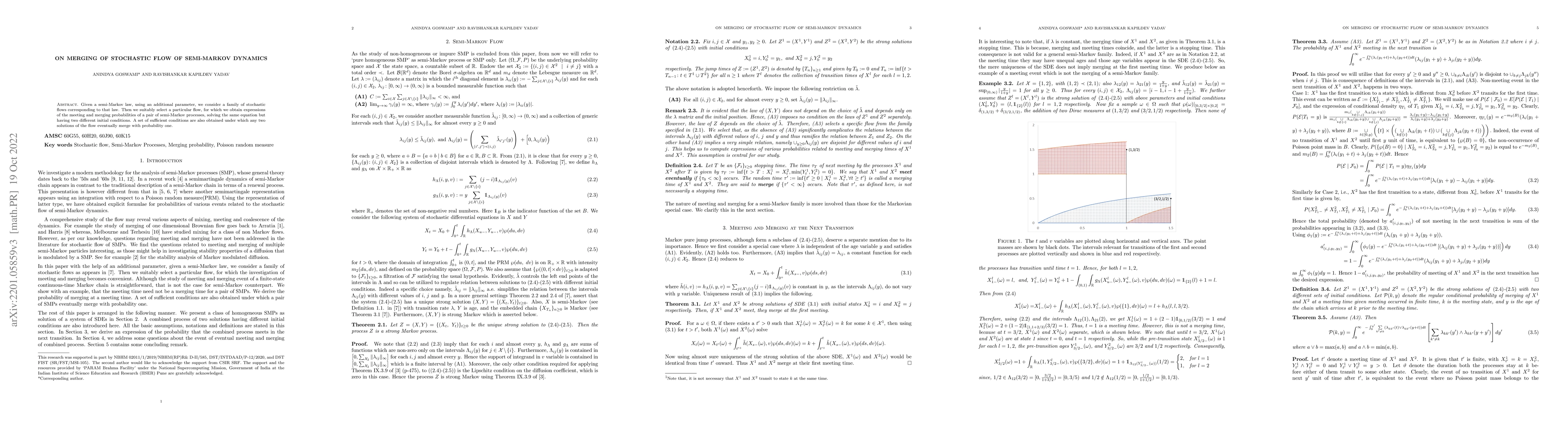

Given a semi-Markov law, using an additional parameter, we consider a family of stochastic flows corresponding to that law. Then we suitably select a particular flow, for which we obtain expressions...

The fully discrete problem for convection-diffusion equation is considered. It comprises compact approximations for spatial discretization, and Crank-Nicolson scheme for temporal discretization. The...

We consider a risk-sensitive optimization of consumption-utility on infinite time horizon where the one-period investment gain depends on an underlying economic state whose evolution over time is as...

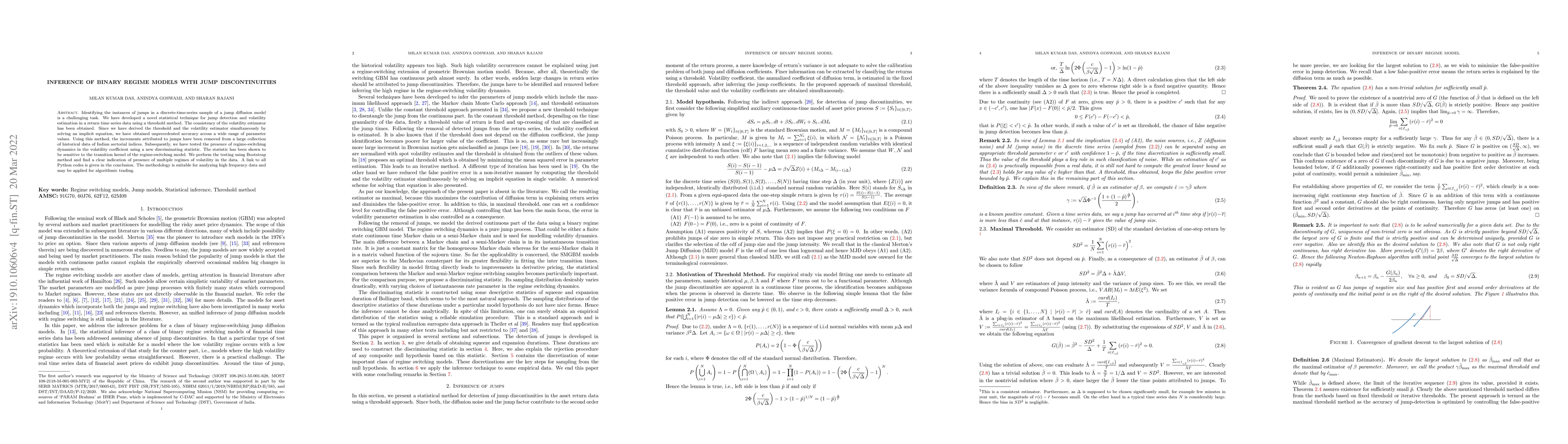

Identifying the instances of jumps in a discrete-time-series sample of a jump diffusion model is a challenging task. We have developed a novel statistical technique for jump detection and volatility...

This paper presents the solution to a European option pricing problem by considering a regime-switching jump diffusion model of the underlying financial asset price dynamics. The regimes are assumed...

In the classical model of stock prices which is assumed to be Geometric Brownian motion, the drift and the volatility of the prices are held constant. However, in reality, the volatility does vary. ...

In this paper, we present a data-driven ensemble approach for option price prediction whose derivation is based on the no-arbitrage theory of option pricing. Using the theoretical treatment, we derive...