Academic Profile

Statistics

Similar Authors

Papers on arXiv

We establish Zaremba problem for Laplacian and $p$-Laplacian with degenerate weights when the Dirichlet condition is only imposed in a set of positive weighted capacity. We prove weighted Sobolev-Po...

We consider the numerical approximation of variational problems with orthotropic growth, that is those where the integrand depends strongly on the coordinate directions with possibly different growt...

In this article we study convex non-autonomous variational problems with differential forms and corresponding function spaces. We introduce a general framework for constructing counterexamples to th...

In the present paper, we examine a Crouzeix-Raviart approximation of the $p(\cdot)$-Dirichlet problem. We derive a $\textit{medius}$ error estimate, $\textit{i.e.}$, a best-approximation result, whi...

We introduce a globally convergent relaxed Kacanov scheme for the computation of the discrete minimizer to the $p$-Laplace problem with $2 \leq p < \infty$. The iterative scheme is easy to implement...

In this paper we are concerned with global maximal regularity estimates for elliptic equations with degenerate weights. We consider both the linear case and the non-linear case. We show that higher ...

We investigate the convergence of the Crouzeix-Raviart finite element method for variational problems with non-autonomous integrands that exhibit non-standard growth conditions. While conforming sch...

A sharp pointwise differential inequality for vectorial second-order partial differential operators, with Uhlenbeck structure, is offered. As a consequence, optimal second-order regularity propertie...

In the present paper we find optimal conditions separating the regular case from the one with Lavrentiev gap for the borderline case of double phase potencial and related general classes of integran...

We obtain new local Calderon-Zygmund estimates for elliptic equations with matrix-valued weights for linear as well as non-linear equations. We introduce a novel log-BMO condition on the weight M. I...

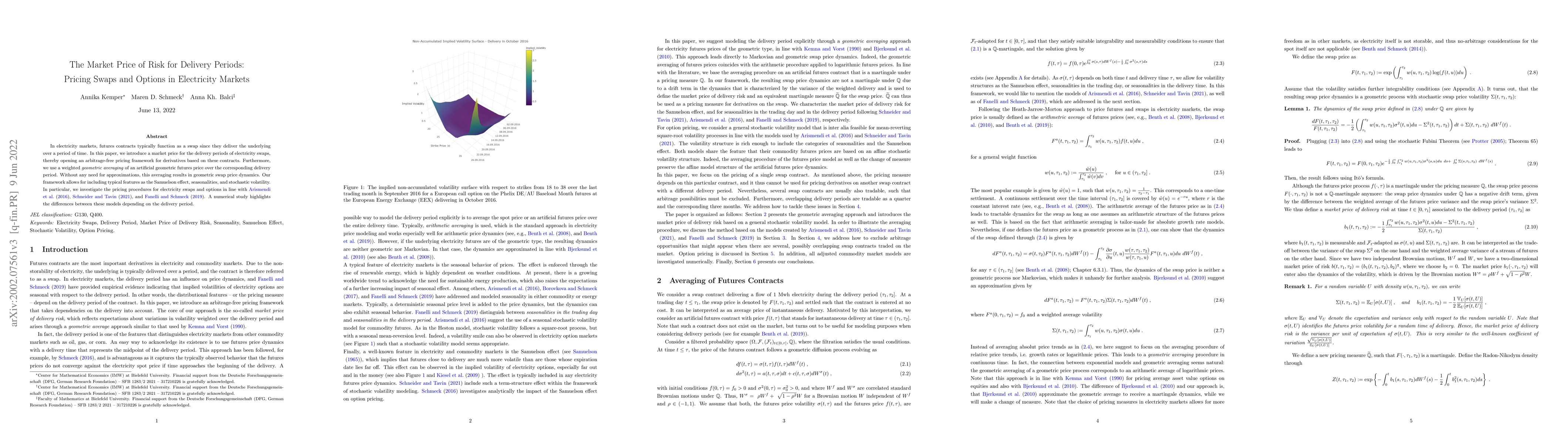

In electricity markets, futures contracts typically function as a swap since they deliver the underlying over a period of time. In this paper, we introduce a market price for the delivery periods of...

Zhikov showed 1986 with his famous checkerboard example that functionals with variable exponents can have a Lavrentiev gap. For this example it was crucial that the exponent had a saddle point whose...

We present nonlocal variants of the famous Meyers' example of limited higher integrability and differentiability. In the limit $s \nearrow 1$ we recover the standard Meyers' example. We consider the f...