Academic Profile

Statistics

Similar Authors

Papers on arXiv

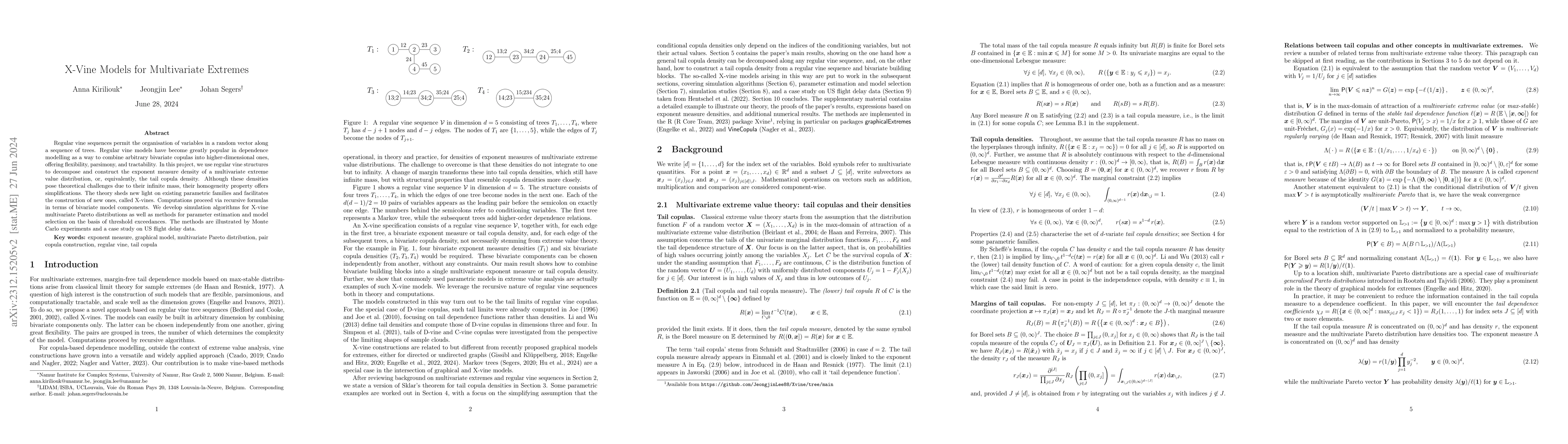

Regular vine sequences permit the organisation of variables in a random vector along a sequence of trees. Regular vine models have become greatly popular in dependence modelling as a way to combine ...

When modeling a vector of risk variables, extreme scenarios are often of special interest. The peaks-over-thresholds method hinges on the notion that, asymptotically, the excesses over a vector of h...

An important problem in extreme-value theory is the estimation of the probability that a high-dimensional random vector falls into a given extreme failure set. This paper provides a parametric appro...

The empirical beta copula is a simple but effective smoother of the empirical copula. Because it is a genuine copula, from which, moreover, it is particularly easy to sample, it is reasonable to exp...

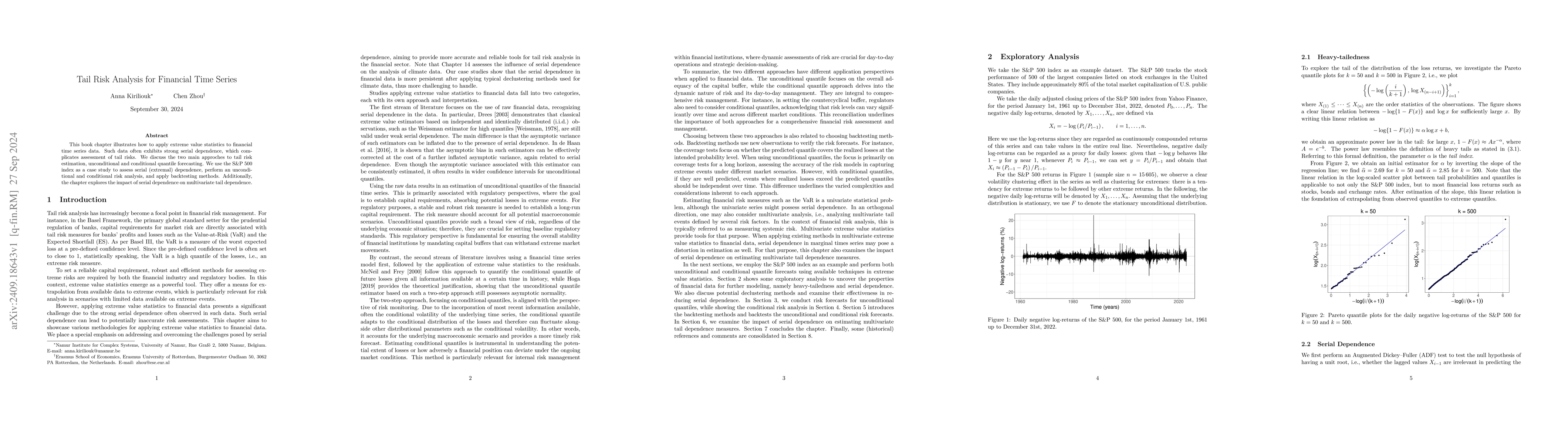

This book chapter illustrates how to apply extreme value statistics to financial time series data. Such data often exhibits strong serial dependence, which complicates assessment of tail risks. We dis...

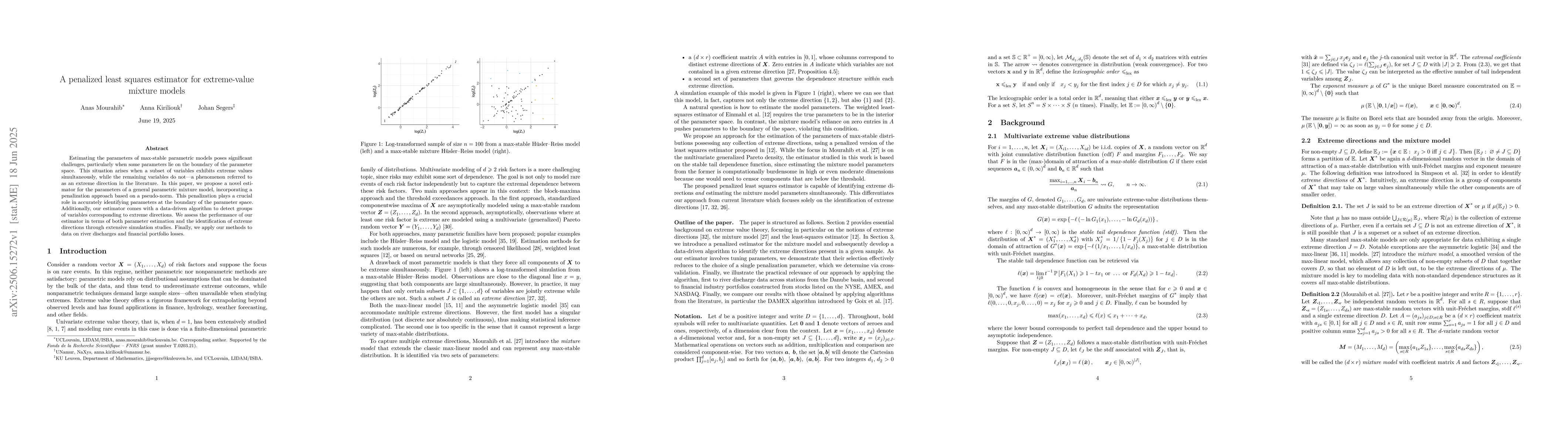

Estimating the parameters of max-stable parametric models poses significant challenges, particularly when some parameters lie on the boundary of the parameter space. This situation arises when a subse...

Extreme value theory offers a statistical framework for quantifying the risk of rare events, with the generalized Pareto (GP) distribution providing the canonical limit model for univariate threshold ...