Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider a Wigner matrix $A$ with entries tail decaying as $x^{-\alpha}$ with $2<\alpha<4$ for large $x$ and study fluctuations of linear statistics $N^{-1}\operatorname{Tr}\varphi(A)$. The behav...

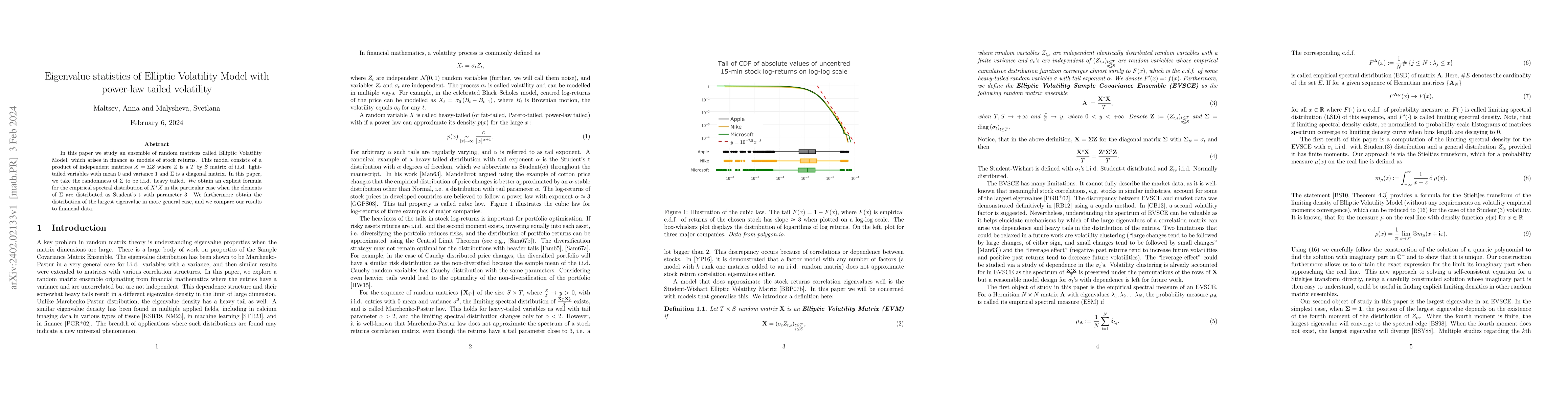

In this paper we study an ensemble of random matrices called Elliptic Volatility Model, which arises in finance as models of stock returns. This model consists of a product of independent matrices $...

We consider N x N matrices with complex entries that are perturbed by a complex Gaussian matrix with small variance. We prove that if the unperturbed matrix satisfies certain local laws then the bul...

Consider an $N$ by $N$ matrix $X$ of complex entries with iid real and imaginary parts. We show that the local density of eigenvalues of $X^*X$ converges to the Marchenko-Pastur law on the optimal s...

In this paper we analyze the covariance kernel of the Gaussian process that arises as the limit of fluctuations of linear spectral statistics for Wigner matrices with a few moments. More precisely, ...

Heart muscle contraction is normally activated by a synchronized Ca release from sarcoplasmic reticulum (SR), a major intracellular Ca store. However, under abnormal conditions Ca leaks from the SR,...

Motivated by the analogy between spectral moments of random matrices and associated zeta functions, we study inverse power trace moments of the Laguerre ensemble of dimension $N$ and inverse temperatu...

We study mesoscopic linear spectral statistics for two ensembles of random quantum graphs. These are defined by a discrete graph $G$ and a unitary-matrix-valued function $U(k)$ indexed by directed edg...