Academic Profile

Statistics

Similar Authors

Papers on arXiv

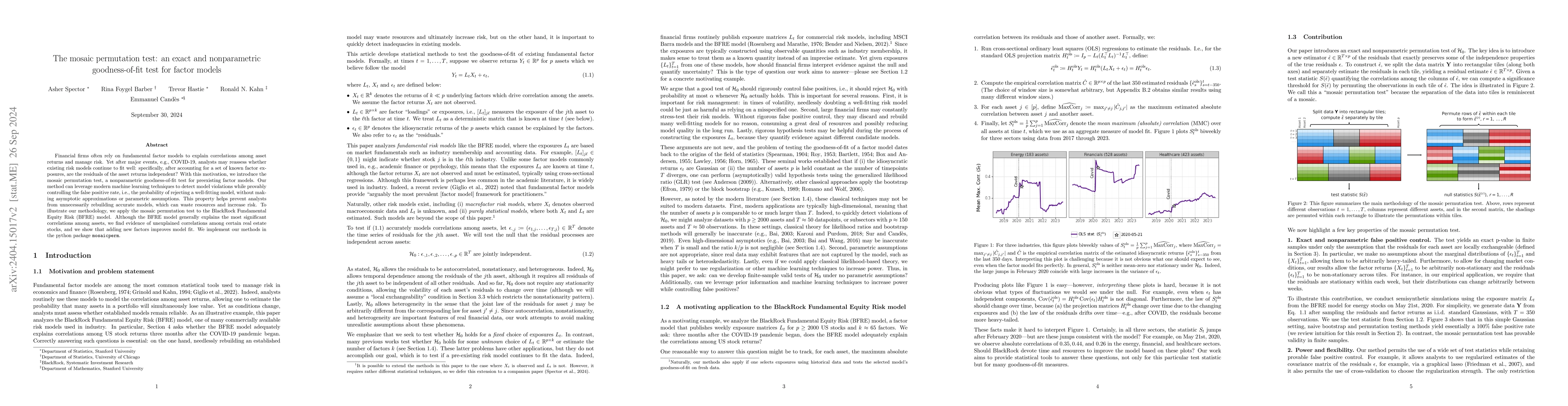

Financial firms often rely on factor models to explain correlations among asset returns. These models are important for managing risk, for example by modeling the probability that many assets will s...

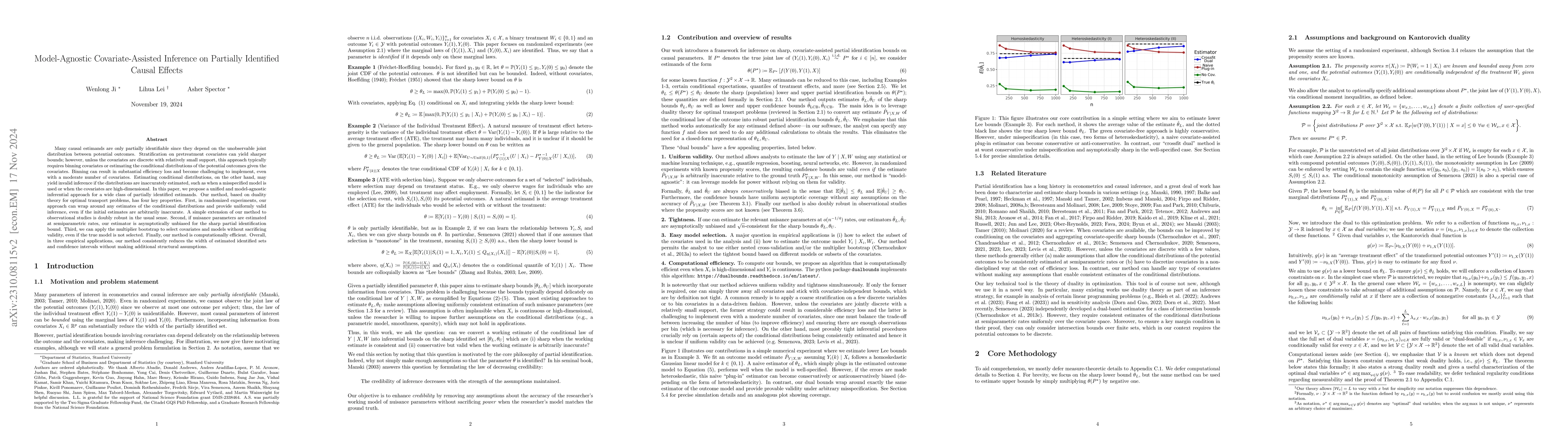

Many causal estimands are only partially identifiable since they depend on the unobservable joint distribution between potential outcomes. Stratification on pretreatment covariates can yield sharper...

This paper introduces a class of asymptotically most powerful knockoff statistics based on a simple principle: that we should prioritize variables in order of our ability to distinguish them from th...

Scientists often must simultaneously localize and discover signals. For instance, in genetic fine-mapping, high correlations between nearby genetic variants make it hard to identify the exact locati...

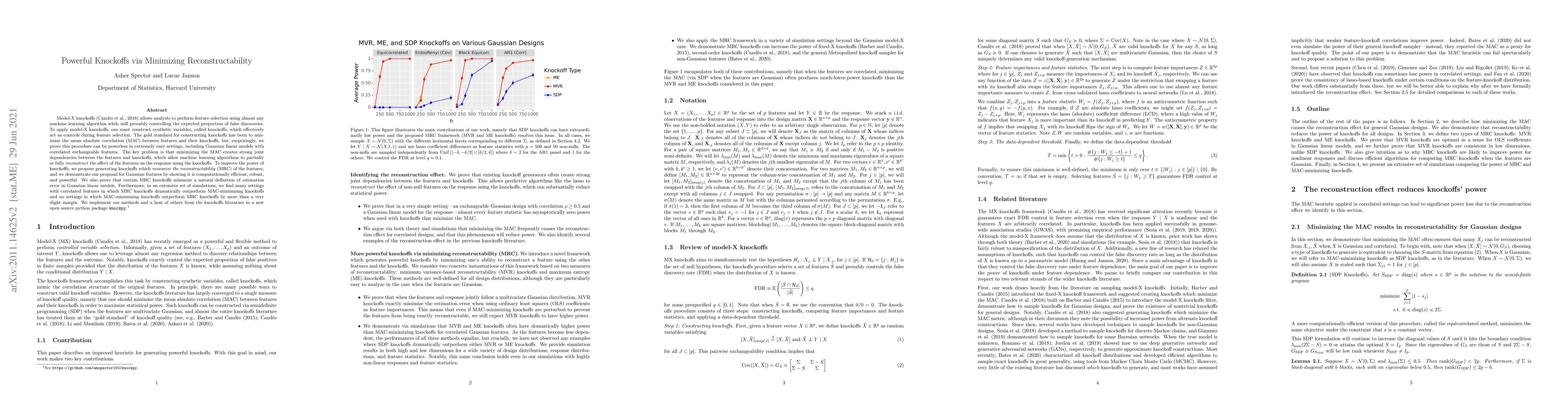

Model-X knockoffs allows analysts to perform feature selection using almost any machine learning algorithm while still provably controlling the expected proportion of false discoveries. To apply mod...

Assessing treatment effect heterogeneity (TEH) in clinical trials is crucial, as it provides insights into the variability of treatment responses among patients, influencing important decisions relate...

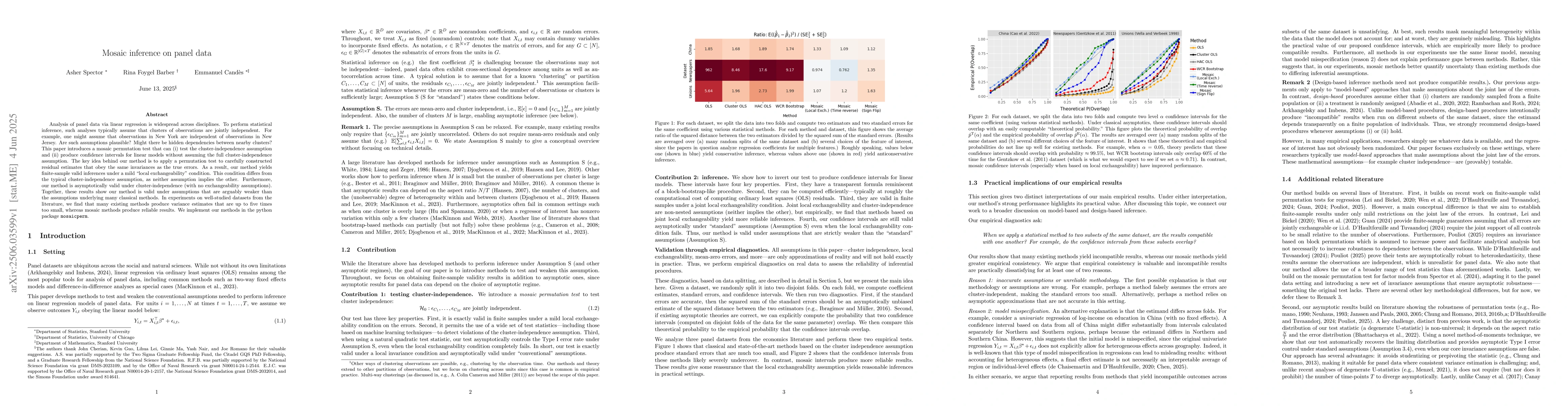

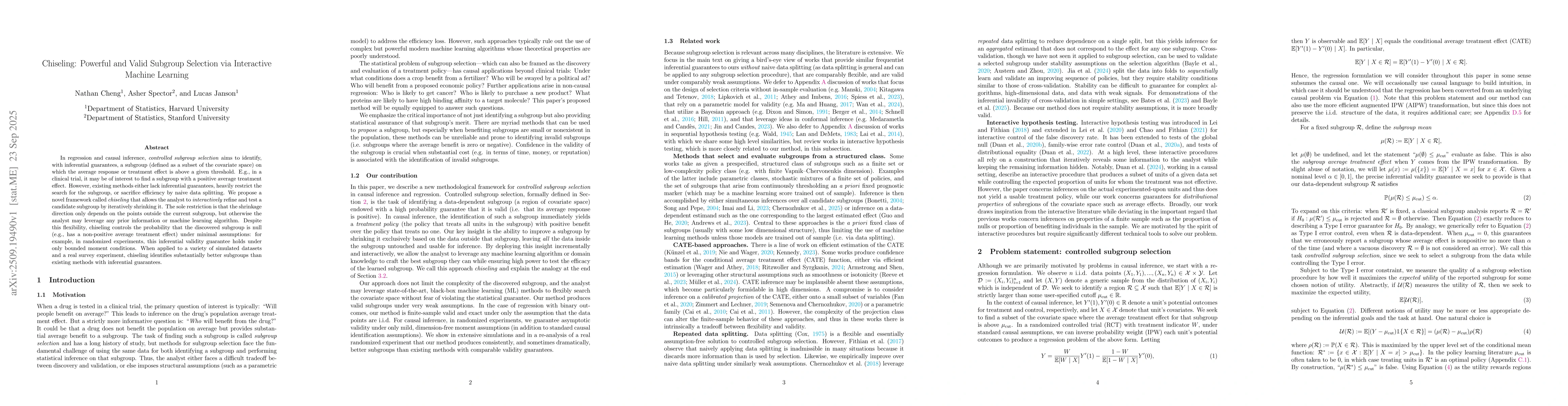

Analysis of panel data via linear regression is widespread across disciplines. To perform statistical inference, such analyses typically assume that clusters of observations are jointly independent. F...

In regression and causal inference, controlled subgroup selection aims to identify, with inferential guarantees, a subgroup (defined as a subset of the covariate space) on which the average response o...

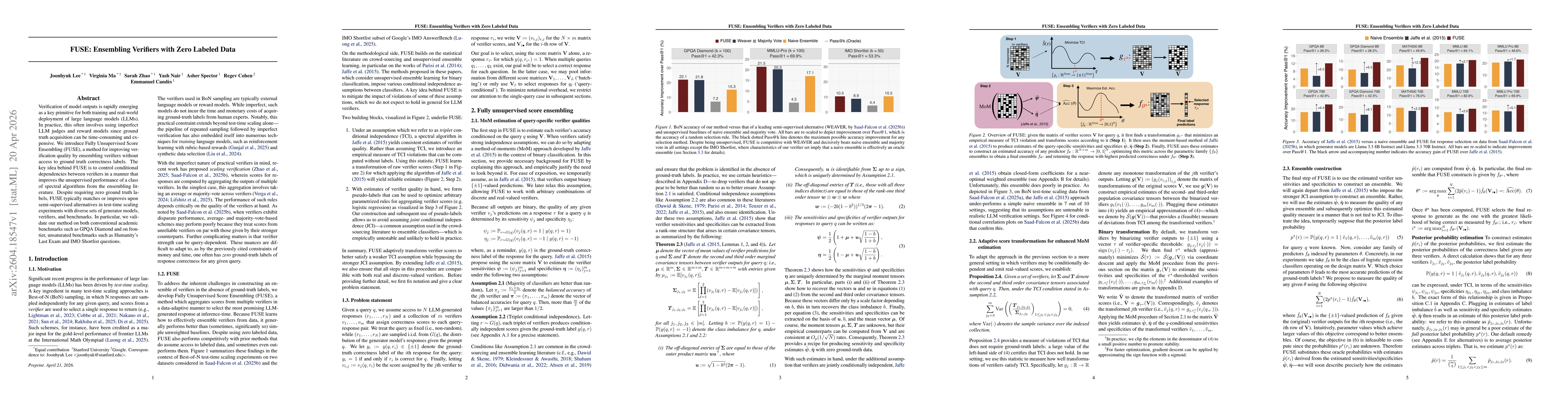

Verification of model outputs is rapidly emerging as a key primitive for both training and real-world deployment of large language models (LLMs). In practice, this often involves using imperfect LLM j...