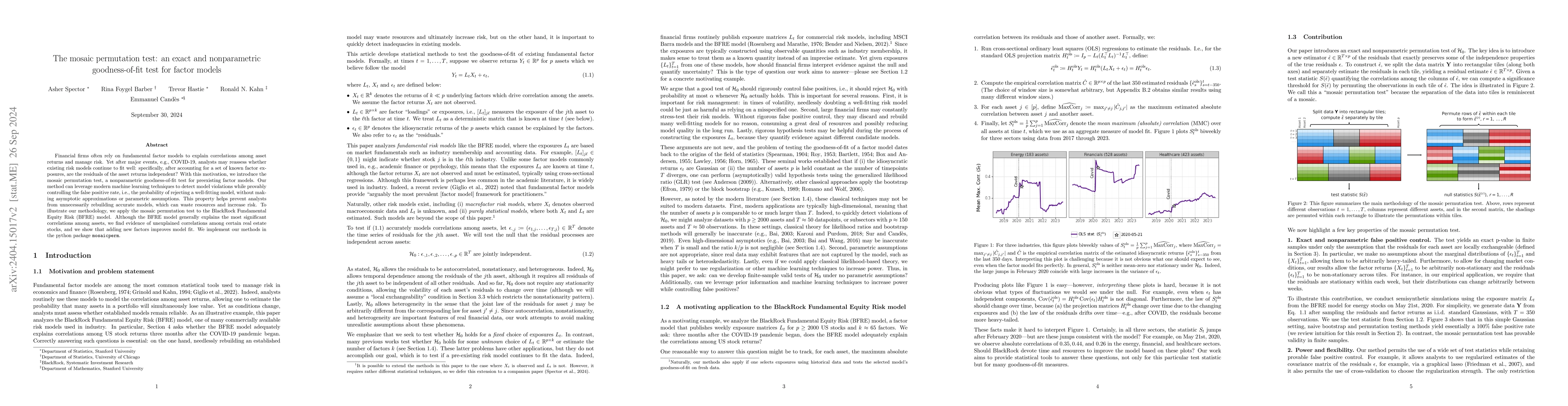

Financial firms often rely on factor models to explain correlations among

asset returns. These models are important for managing risk, for example by

modeling the probability that many assets will simultaneously lose value. Yet

after major events, e.g., COVID-19, analysts may reassess whether existing

models continue to fit well: specifically, after accounting for the factor

exposures, are the residuals of the asset returns independent? With this

motivation, we introduce the mosaic permutation test, a nonparametric

goodness-of-fit test for preexisting factor models. Our method allows analysts

to use nearly any machine learning technique to detect model violations while

provably controlling the false positive rate, i.e., the probability of

rejecting a well-fitting model. Notably, this result does not rely on

asymptotic approximations and makes no parametric assumptions. This property

helps prevent analysts from unnecessarily rebuilding accurate models, which can

waste resources and increase risk. We illustrate our methodology by applying it

to the Blackrock Fundamental Equity Risk (BFRE) model. Using the mosaic

permutation test, we find that the BFRE model generally explains the most

significant correlations among assets. However, we find evidence of unexplained

correlations among certain real estate stocks, and we show that adding new

factors improves model fit. We implement our methods in the python package

mosaicperm.

Discussion 0