Academic Profile

Statistics

Similar Authors

Papers on arXiv

Fractional Brownian motion has become a standard tool to address long-range dependence in financial time series. However, a constant memory parameter is too restrictive to address different market c...

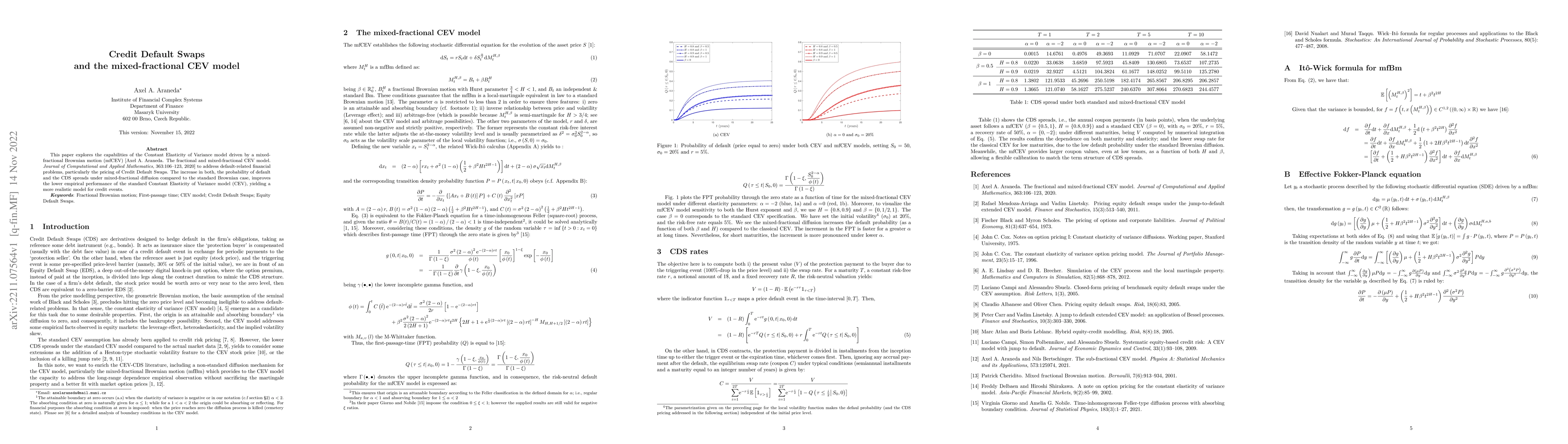

This paper explores the capabilities of the Constant Elasticity of Variance model driven by a mixed-fractional Brownian motion (mfCEV) [Axel A. Araneda. The fractional and mixed-fractional CEV model...

In this paper, we examine the interlinkages among firms through a financial network where cross-holdings on both equity and debt are allowed. We relate mathematically the correlation among equities ...

The Generalized fractional Brownian motion (gfBm) is a stochastic process that acts as a generalization for both fractional, sub-fractional, and standard Brownian motion. Here we study its use as th...

The exponentially weighted moving average (EMWA) could be labeled as a competitive volatility estimator, where its main strength relies on computation simplicity, especially in a multi-asset scenari...

The sub-fractional Brownian motion (sfBm) is a stochastic process, characterized by non-stationarity in their increments and long-range dependency, considered as an intermediate step between the sta...

The continuous observation of the financial markets has identified some stylized facts which challenge the conventional assumptions, promoting the born of new approaches. On the one hand, the long-r...