Academic Profile

Statistics

Similar Authors

Papers on arXiv

Many methods for estimating integrated volatility and related functionals of semimartingales in the presence of jumps require specification of tuning parameters for their use in practice. In much of...

We propose a novel family of test statistics to detect the presence of changepoints in a sequence of dependent, possibly multivariate, functional-valued observations. Our approach allows to test for...

Statistical inference for stochastic processes based on high-frequency observations has been an active research area for more than two decades. One of the most well-known and widely studied problems...

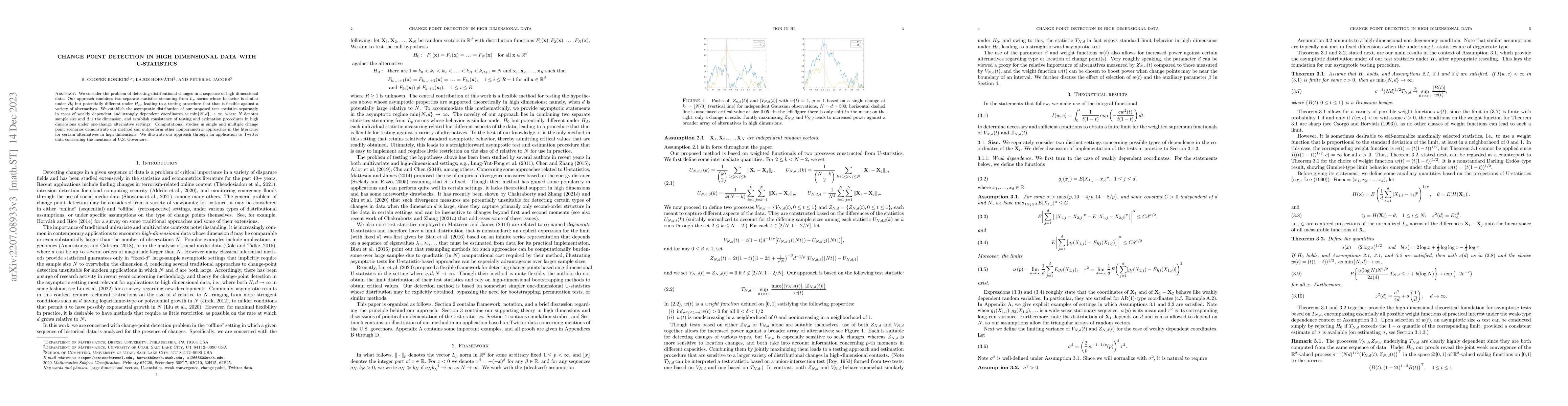

We consider the problem of detecting distributional changes in a sequence of high dimensional data. Our approach combines two separate statistics stemming from $L_p$ norms whose behavior is similar ...

Statistical inference for stochastic processes based on high-frequency observations has been an active research area for more than a decade. One of the most well-known and widely studied problems is...

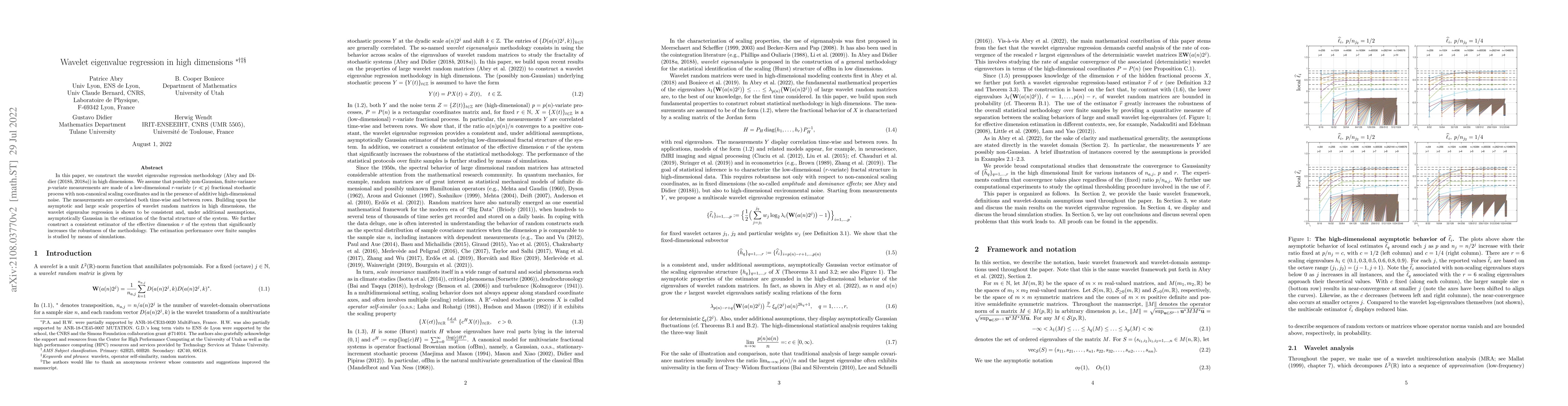

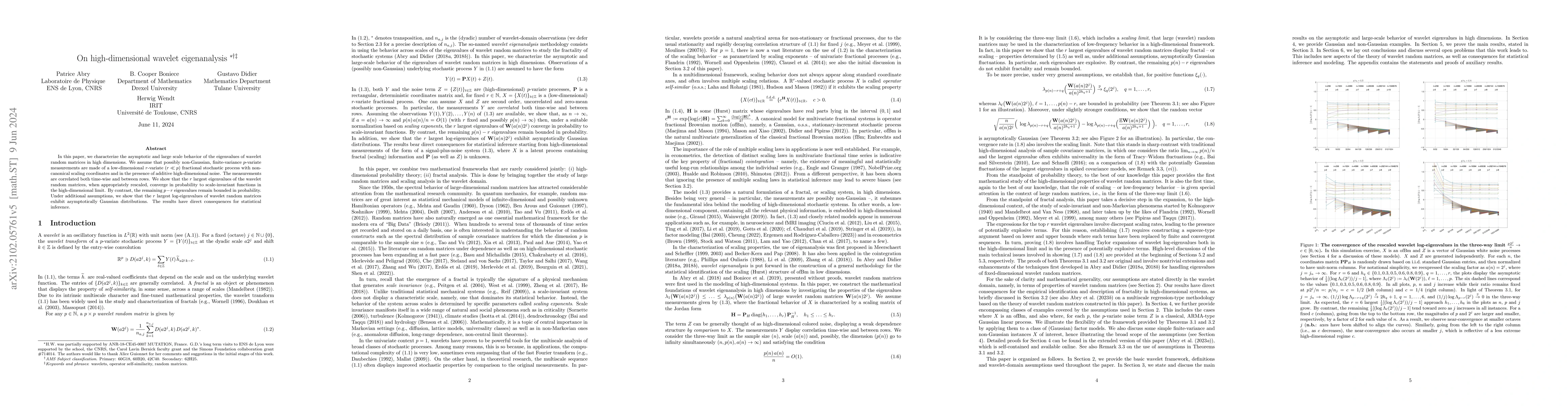

In this paper, we construct the wavelet eigenvalue regression methodology in high dimensions. We assume that possibly non-Gaussian, finite-variance $p$-variate measurements are made of a low-dimensi...

In this paper, we characterize the asymptotic and large scale behavior of the eigenvalues of wavelet random matrices in high dimensions. We assume that possibly non-Gaussian, finite-variance $p$-var...

Volatility estimation is a central problem in financial econometrics, but becomes particularly challenging when jump activity is high, a phenomenon observed empirically in highly traded financial secu...