Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a multivariate version of adapted transport, which we name multicausal transport, involving several filtered processes among which causality constraints are imposed. Subsequently, we co...

We regard the optimal reinsurance problem as an iterated optimal transport problem between a (known) initial and an (unknown) resulting risk exposure of the insurer. We also provide conditions that ...

The Bass local volatility model introduced by Backhoff-Veraguas--Beiglb\"ock--Huesmann--K\"allblad is a Markov model perfectly calibrated to vanilla options at finitely many maturities, that approxi...

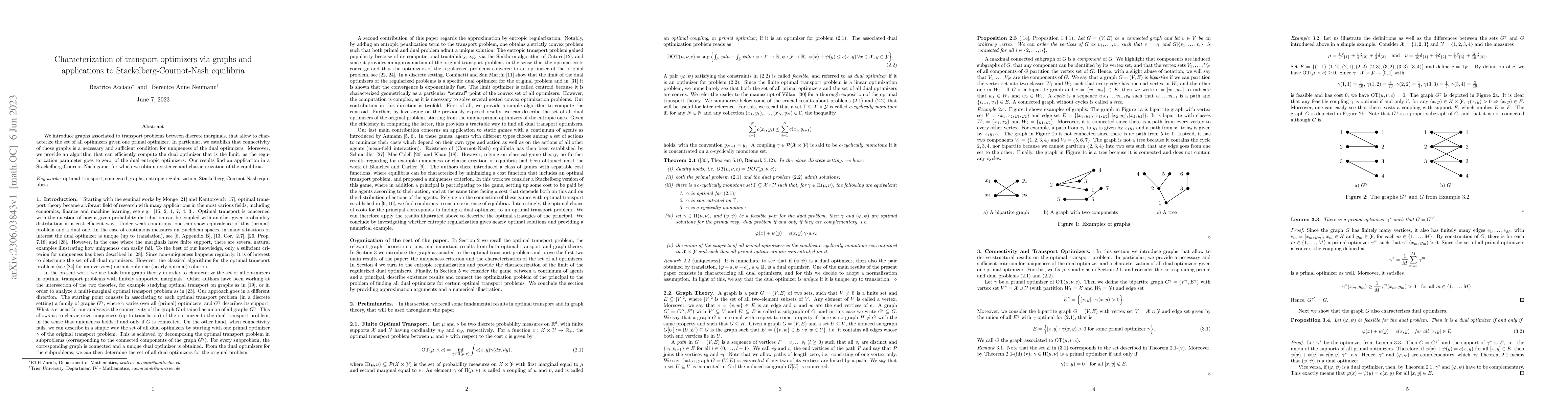

We introduce graphs associated to transport problems between discrete marginals, that allow to characterize the set of all optimizers given one primal optimizer. In particular, we establish that con...

We consider empirical measures of $\R^{d}$-valued stochastic process in finite discrete-time. We show that the adapted empirical measure introduced in the recent work \cite{backhoff2022estimating} b...

In this paper we provide a quantitative analysis to the concept of arbitrage, that allows to deal with model uncertainty without imposing the no-arbitrage condition. In markets that admit ``small ar...

We provide a short proof of the intriguing characterisation of the convex order given by Wiesel and Zhang.

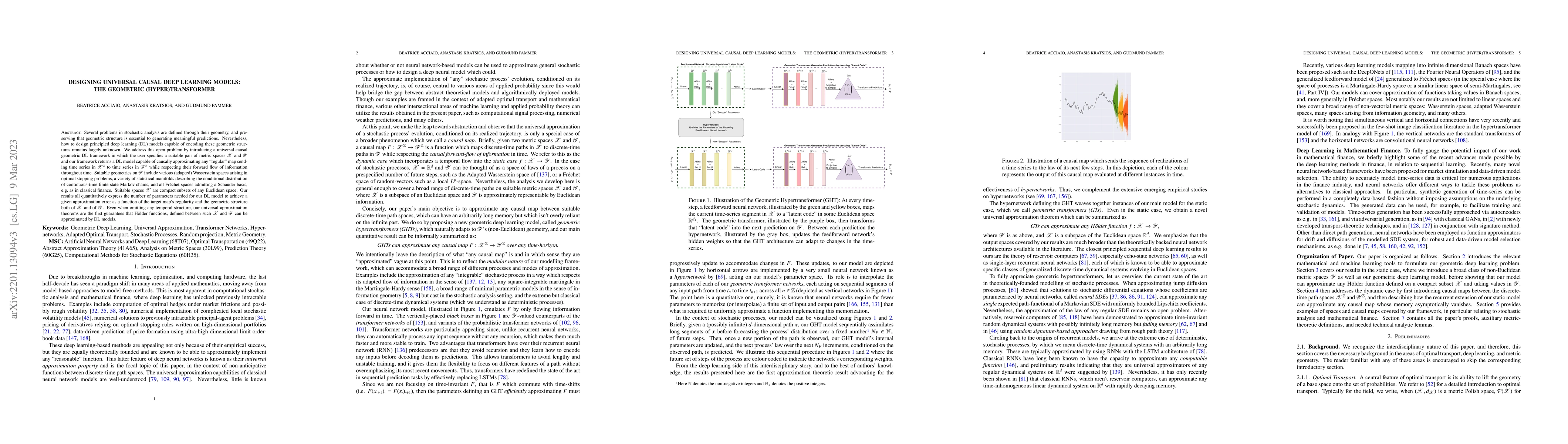

Several problems in stochastic analysis are defined through their geometry, and preserving that geometric structure is essential to generating meaningful predictions. Nevertheless, how to design pri...

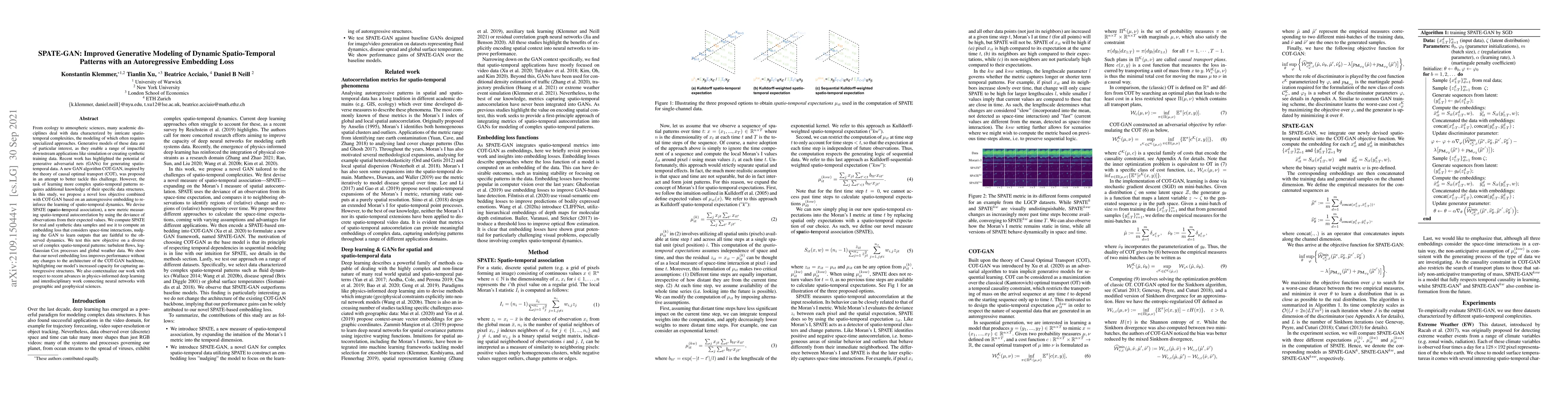

From ecology to atmospheric sciences, many academic disciplines deal with data characterized by intricate spatio-temporal complexities, the modeling of which often requires specialized approaches. G...

Causal Optimal Transport (COT) results from imposing a temporal causality constraint on classic optimal transport problems, which naturally generates a new concept of distances between distributions...

We consider a model-independent pricing problem in a fixed-income market and show that it leads to a weak optimal transport problem as introduced by Gozlan et al. We use this to characterize the ext...

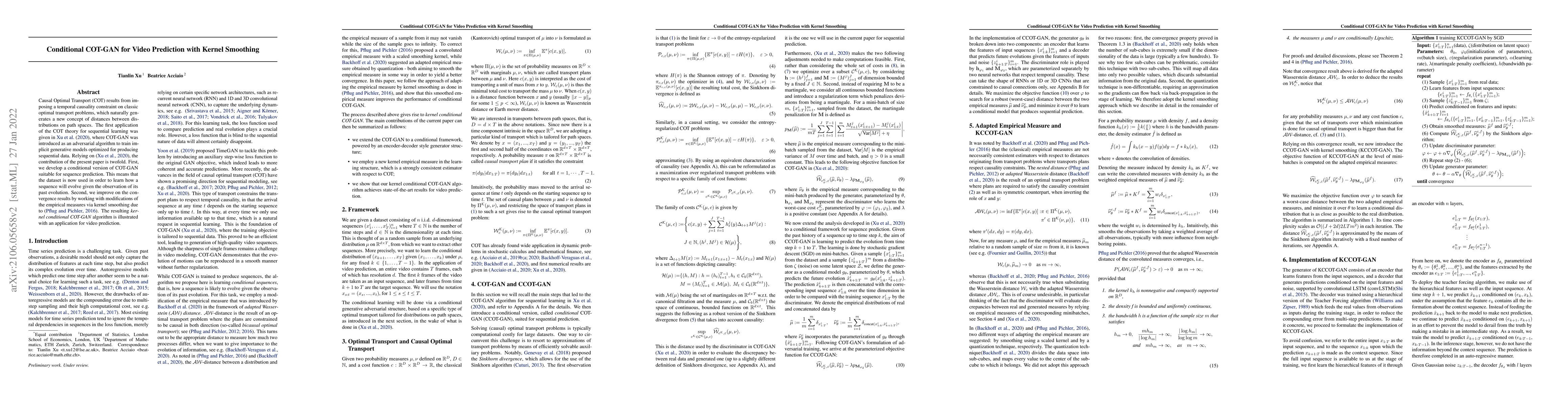

We introduce COT-GAN, an adversarial algorithm to train implicit generative models optimized for producing sequential data. The loss function of this algorithm is formulated using ideas from Causal ...

We consider a large population dynamic game in discrete time. The peculiarity of the game is that players are characterized by time-evolving types, and so reasonably their actions should not anticip...

It has often been stated that, within the class of continuous stochastic volatility models calibrated to vanillas, the price of a VIX future is maximized by the Dupire local volatility model. In thi...

We build a time-causal variational autoencoder (TC-VAE) for robust generation of financial time series data. Our approach imposes a causality constraint on the encoder and decoder networks, ensuring a...

The adapted Wasserstein distance is a metric for quantifying distributional uncertainty and assessing the sensitivity of stochastic optimization problems on time series data. A computationally efficie...

The adapted Wasserstein ($AW$) distance refines the classical Wasserstein ($W$) distance by incorporating the temporal structure of stochastic processes. This makes the $AW$-distance well-suited as a ...

We study absolutely continuous curves in the adapted Wasserstein space of filtered processes. We provide a probabilistic representation of such curves as flows of adapted processes on a common filtere...

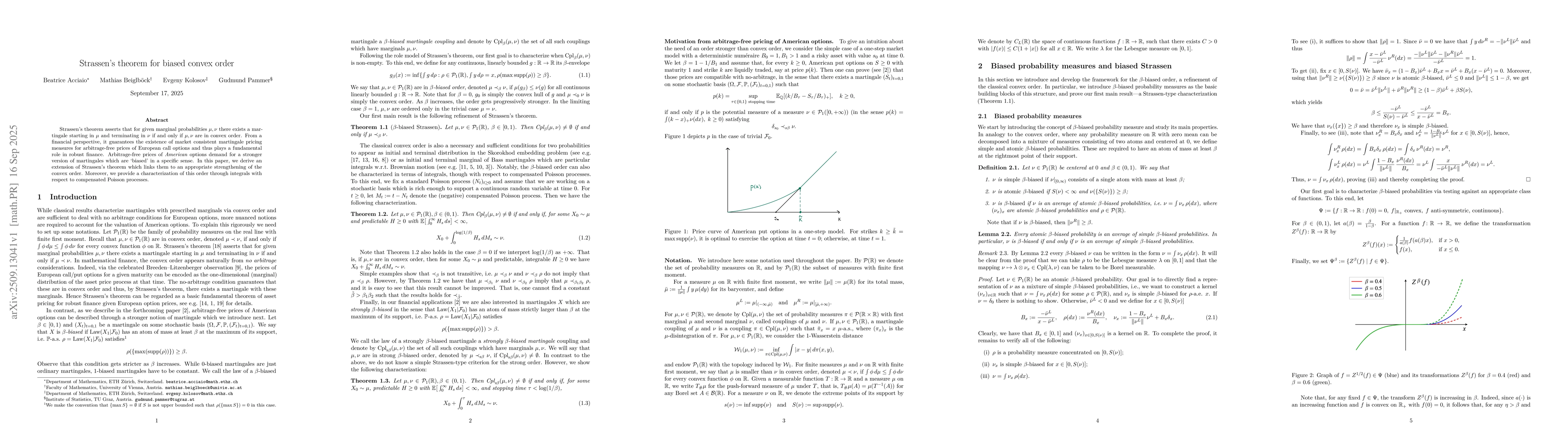

Strassen's theorem asserts that for given marginal probabilities $\mu,\nu$ there exists a martingale starting in $\mu$ and terminating in $\nu$ if and only if $\mu,\nu$ are in convex order. From a fin...

We formulate a dynamic reinsurance problem in which the insurer seeks to control the terminal distribution of its surplus while minimizing the L2-norm of the ceded risk. Using techniques from martinga...

The adapted Bures--Wasserstein space consists of Gaussian processes endowed with the adapted Wasserstein distance. It can be viewed as the analogue of the classical Bures--Wasserstein space in optimal...

We propose a mathematical framework to explain implicit regularization from early stopping during the training of overparametrized neural networks. In the mean-field limit, the parameter distribution ...

Motivated by the connection between the Kyle equilibrium with static private signal and the Brownian bridge, we study a much broader class of bridges that allow one to consider more general equilibriu...