Bezirgen Veliyev

9 papers on arXiv

Academic Profile

Statistics

Papers on arXiv

A GMM approach to estimate the roughness of stochastic volatility

We develop a GMM approach for estimation of log-normal stochastic volatility models driven by a fractional Brownian motion with unrestricted Hurst exponent. We show that a parameter estimator based ...

Treatment recommendation with distributional targets

We study the problem of a decision maker who must provide the best possible treatment recommendation based on an experiment. The desirability of the outcome distribution resulting from the policy re...

Functional Sequential Treatment Allocation with Covariates

We consider a multi-armed bandit problem with covariates. Given a realization of the covariate vector, instead of targeting the treatment with highest conditional expectation, the decision maker tar...

Functional Sequential Treatment Allocation

Consider a setting in which a policy maker assigns subjects to treatments, observing each outcome before the next subject arrives. Initially, it is unknown which treatment is best, but the sequentia...

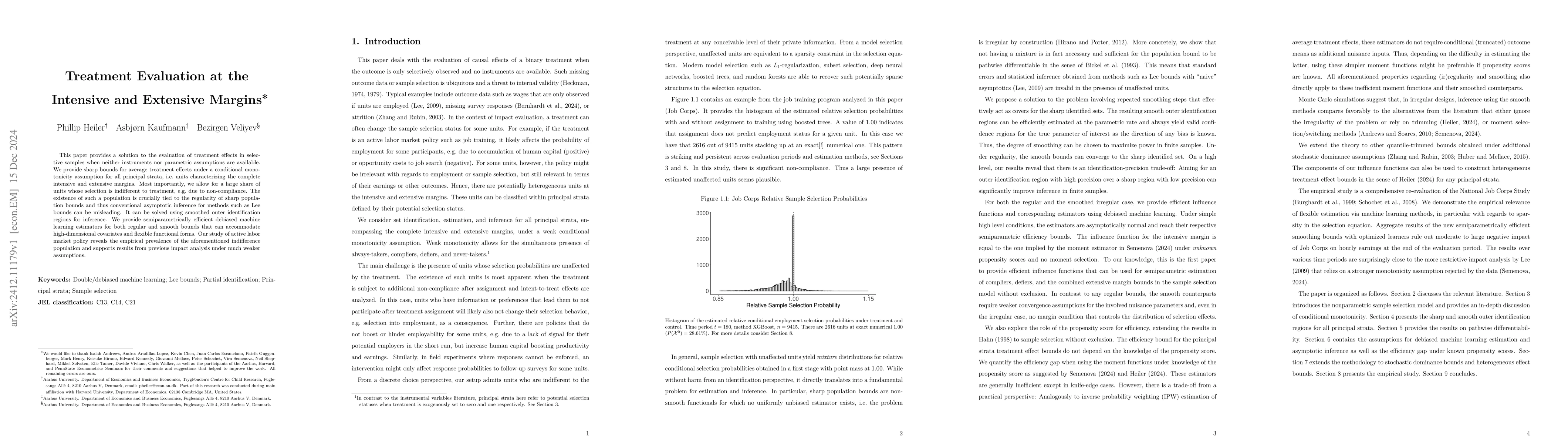

Treatment Evaluation at the Intensive and Extensive Margins

This paper provides a solution to the evaluation of treatment effects in selective samples when neither instruments nor parametric assumptions are available. We provide sharp bounds for average treatm...

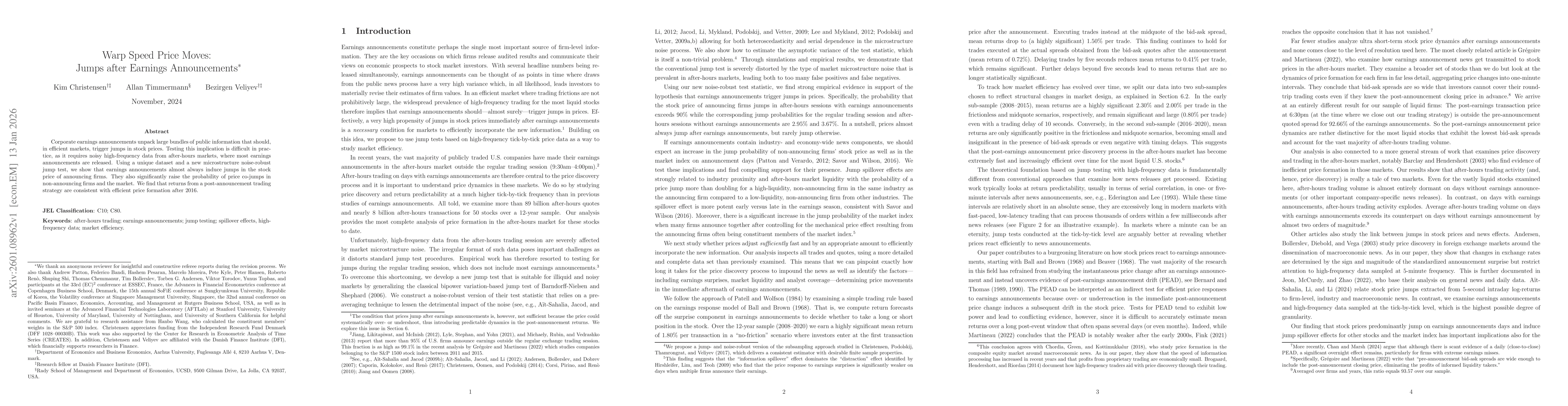

Warp speed price moves: Jumps after earnings announcements

Corporate earnings announcements unpack large bundles of public information that should, in efficient markets, trigger jumps in stock prices. Testing this implication is difficult in practice, as it r...

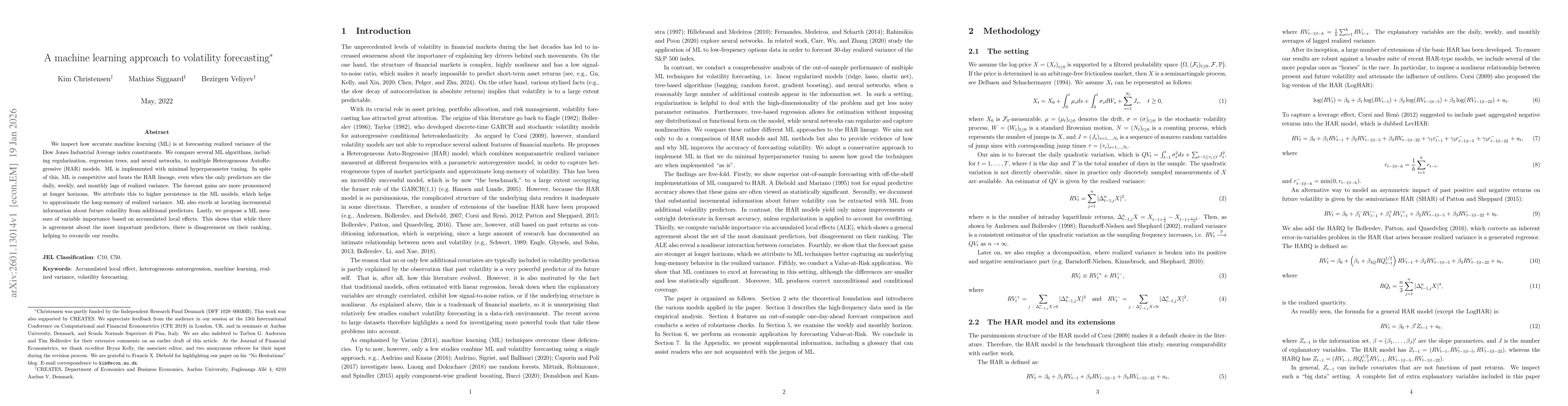

A machine learning approach to volatility forecasting

We inspect how accurate machine learning (ML) is at forecasting realized variance of the Dow Jones Industrial Average index constituents. We compare several ML algorithms, including regularization, re...

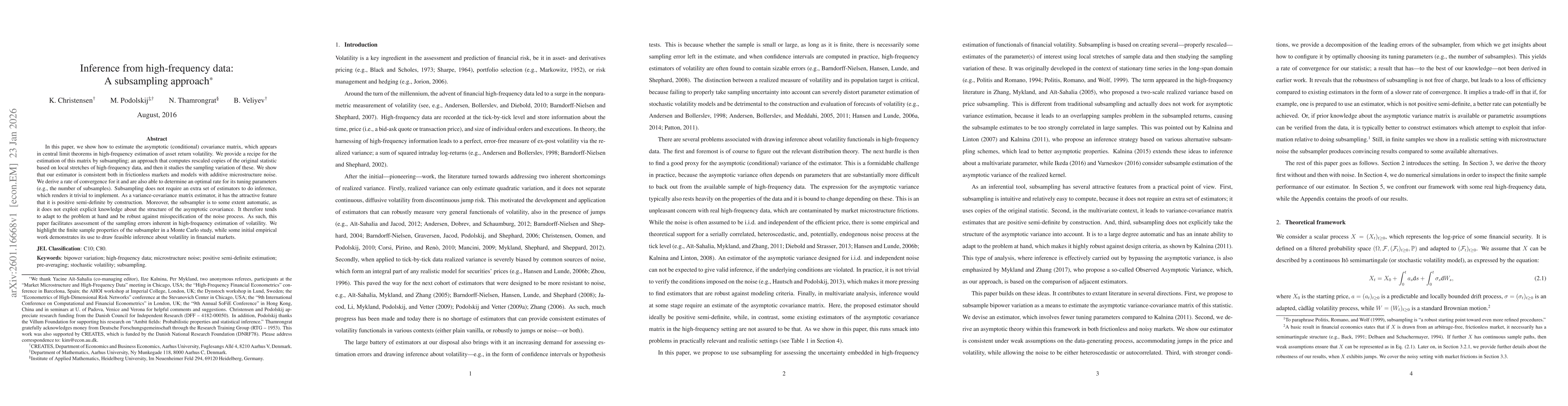

Inference from high-frequency data: A subsampling approach

In this paper, we show how to estimate the asymptotic (conditional) covariance matrix, which appears in central limit theorems in high-frequency estimation of asset return volatility. We provide a rec...

The realized empirical distribution function of stochastic variance with application to goodness-of-fit testing

We propose a nonparametric estimator of the empirical distribution function (EDF) of the latent spot variance of the log-price of a financial asset. We show that over a fixed time span our realized ED...