Byoung Ki Seo

Ulsan National Institute of Science and Technology

Academic Profile

Statistics

Similar Authors

Papers on arXiv

The stochastic-alpha-beta-rho (SABR) model has been widely adopted in options trading. In particular, the normal ($\beta=0$) SABR model is a popular model choice for interest rates because it allows...

This study proposes a versatile model for the dynamics of the best bid and ask prices using an extended Hawkes process. The model incorporates the zero intensities of the spread-narrowing processes ...

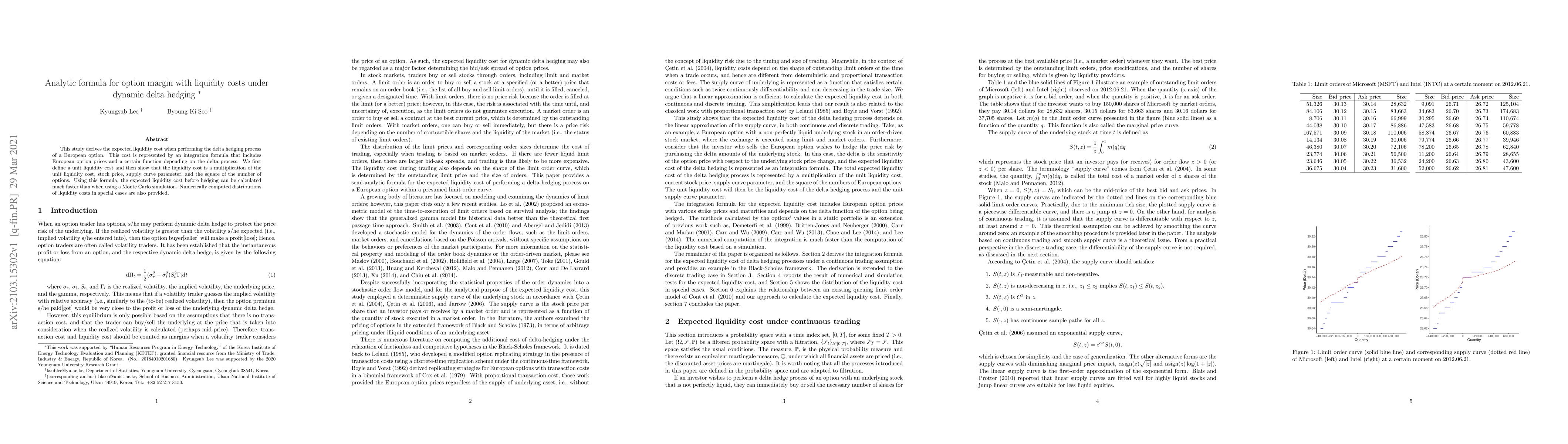

This study derives the expected liquidity cost when performing the delta hedging process of a European option. This cost is represented by an integration formula that includes European option prices...

The third moment variation of a financial asset return process is defined by the quadratic covariation between the return and square return processes. The skew and fat tail risk of an underlying ass...

This study examine the theoretical and empirical perspectives of the symmetric Hawkes model of the price tick structure. Combined with the maximum likelihood estimation, the model provides a proper ...

A simple Hawkes model have been developed for the price tick structure dynamics incorporating market microstructure noise and trade clustering. In this paper, the model is extended with random mark ...