Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose model-free (nonparametric) estimators of the volatility of volatility and leverage effect using high-frequency observations of short-dated options. At each point in time, we integrate ava...

We derive a nonparametric higher-order asymptotic expansion for small-time changes of conditional characteristic functions of It\^o semimartingale increments. The asymptotics setup is of joint type:...

We derive a higher-order asymptotic expansion of the conditional characteristic function of the increment of an It\^o semimartingale over a shrinking time interval. The spot characteristics of the I...

Consider the sum $Y=B+B(H)$ of a Brownian motion $B$ and an independent fractional Brownian motion $B(H)$ with Hurst parameter $H\in(0,1)$. Surprisingly, even though $B(H)$ is not a semimartingale, ...

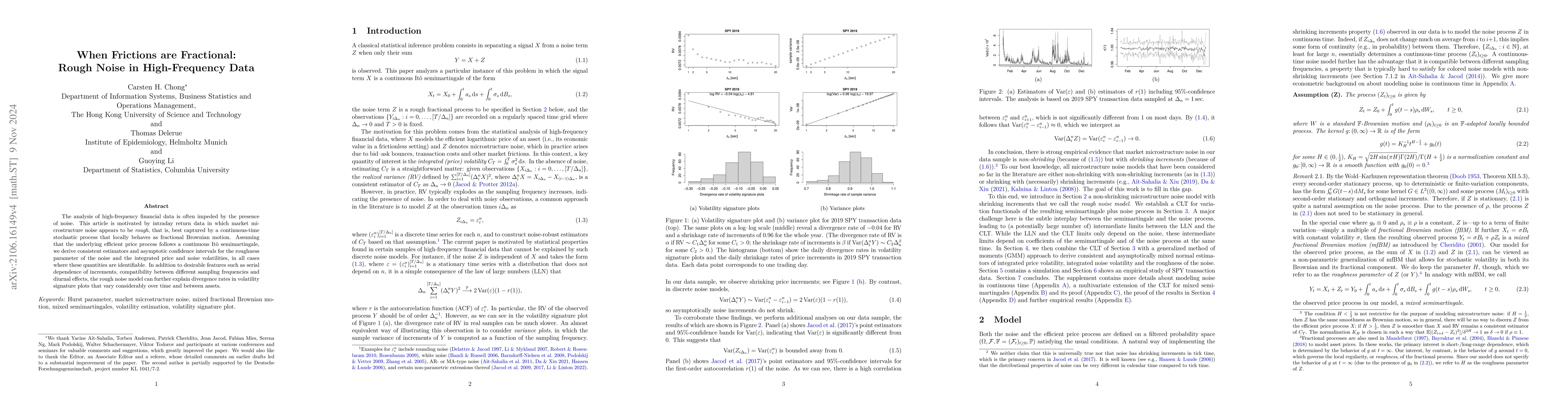

The analysis of high-frequency financial data is often impeded by the presence of noise. This article is motivated by intraday transactions data in which market microstructure noise appears to be ro...

We develop a nonparametric test for deciding whether volatility of an asset follows a standard semimartingale process, with paths of finite quadratic variation, or a rough process with paths of infini...

This paper develops the asymptotic likelihood theory for triangular arrays of stationary Gaussian time series depending on a multidimensional unknown parameter. We give sufficient conditions for the a...