Academic Profile

Statistics

Similar Authors

Papers on arXiv

This work develops non-asymptotic theory for estimation of the long-run variance matrix and its inverse, the so-called precision matrix, for high-dimensional time series under general assumptions on...

Identifying network Granger causality in large vector autoregressive (VAR) models enhances explanatory power by capturing complex interdependencies among variables. Instead of constructing network str...

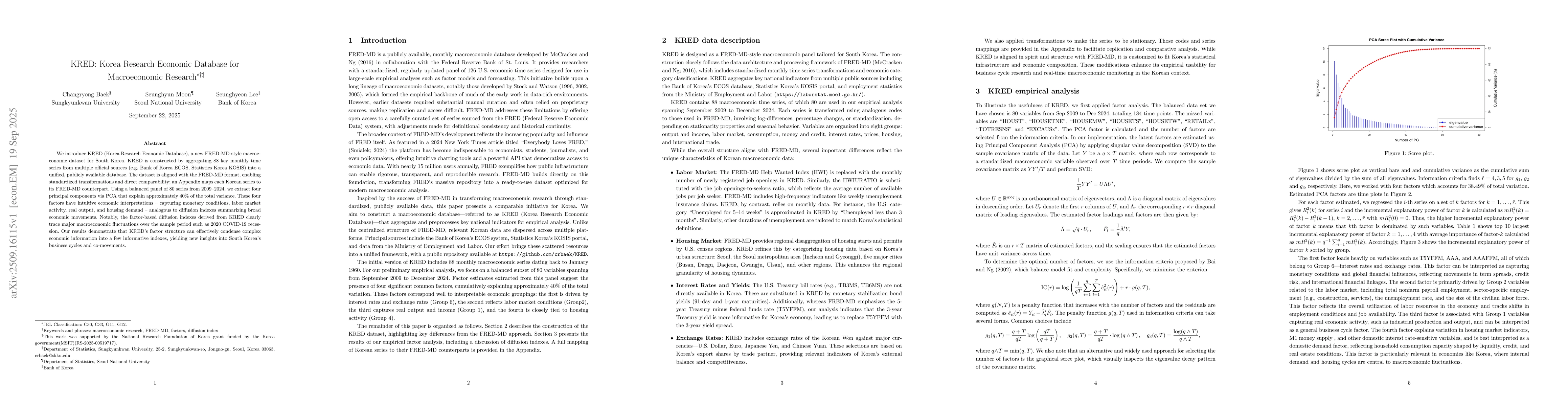

We introduce KRED (Korea Research Economic Database), a new FRED MD style macroeconomic dataset for South Korea. KRED is constructed by aggregating 88 key monthly time series from multiple official so...

This paper proposes a dynamic network framework for uncovering latent community paths in high-dimensional VAR-type models. By embedding a degree-corrected stochastic co-blockmodel (ScBM) into the tran...