Academic Profile

Statistics

Similar Authors

Papers on arXiv

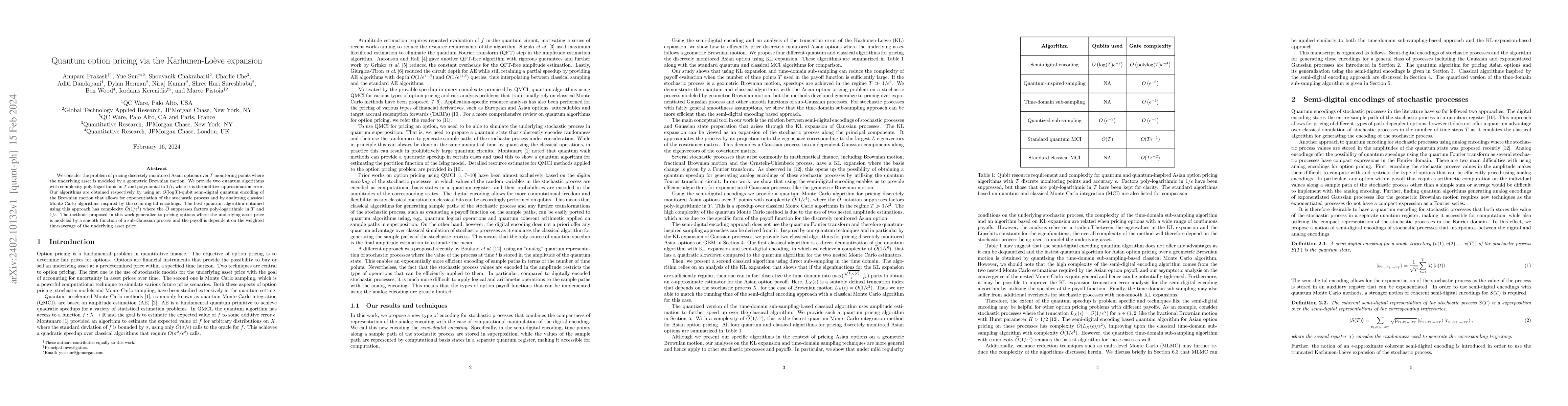

We consider the problem of pricing discretely monitored Asian options over $T$ monitoring points where the underlying asset is modeled by a geometric Brownian motion. We provide two quantum algorith...

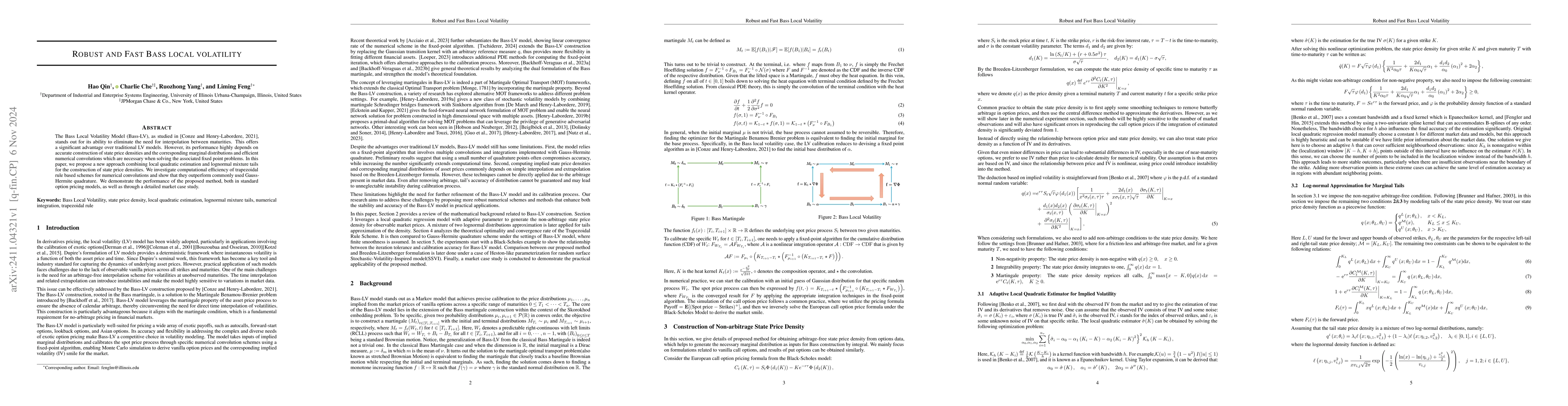

The Bass Local Volatility Model (Bass-LV), as studied in \citep{henry2021bass}, stands out for its ability to eliminate the need for interpolation between maturities. This offers a significant advanta...

Managing exotic derivatives requires accurate mark-to-market pricing and stable Greeks for reliable hedging. The Local Volatility (LV) model distinguishes itself from other pricing models by its abili...

This paper explores advancements in quantum algorithms for derivative pricing of exotics, a computational pipeline of fundamental importance in quantitative finance. For such cases, the classical Mont...

We establish dual attainment for the multimarginal, multi-asset martingale optimal transport (MOT) problem, a fundamental question in the mathematical theory of model-independent pricing and hedging i...

We propose a model independent framework for generating SPX and VIX risk scenarios based on a joint optimal transport calibration of their market smiles. Starting from the entropic martingale optimal ...