Academic Profile

Statistics

Similar Authors

Papers on arXiv

In biochemically reactive systems with small copy numbers of one or more reactant molecules, the dynamics is dominated by stochastic effects. To approximate those systems, discrete state-space and s...

Efficiently pricing multi-asset options poses a significant challenge in quantitative finance. The Monte Carlo (MC) method remains the prevalent choice for pricing engines; however, its slow converg...

This work considers a short-term, continuous time setting characterized by a coupled power supply system controlled exclusively by a single provider and comprising a cascade of hydropower systems (d...

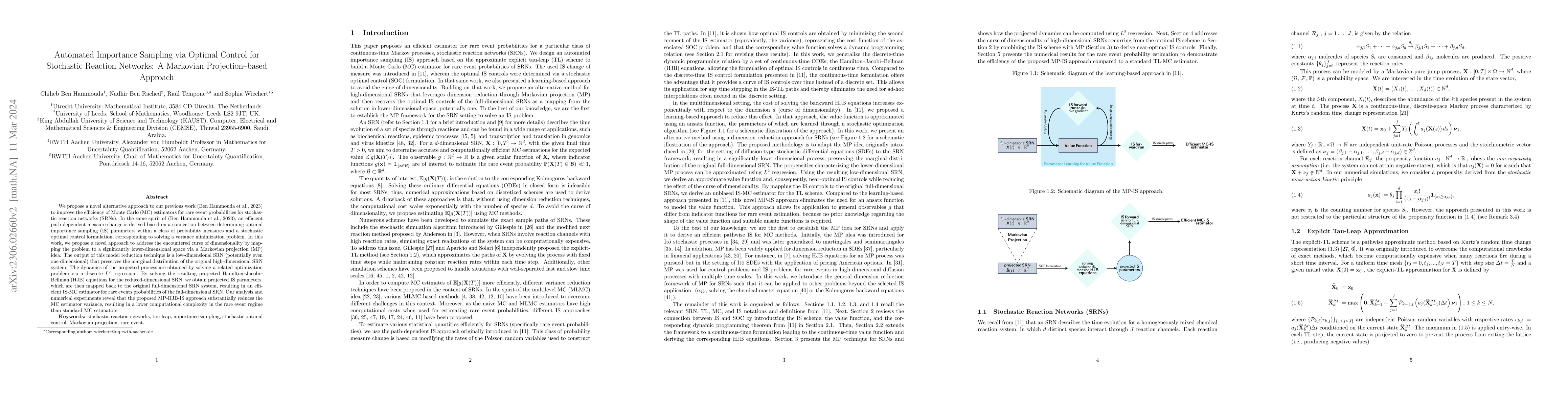

We propose a novel alternative approach to our previous work (Ben Hammouda et al., 2023) to improve the efficiency of Monte Carlo (MC) estimators for rare event probabilities for stochastic reaction...

When approximating the expectations of a functional of a solution to a stochastic differential equation, the numerical performance of deterministic quadrature methods, such as sparse grid quadrature...

We explore efficient estimation of statistical quantities, particularly rare event probabilities, for stochastic reaction networks. Consequently, we propose an importance sampling (IS) approach to i...

The multilevel Monte Carlo (MLMC) method is highly efficient for estimating expectations of a functional of a solution to a stochastic differential equation (SDE). However, MLMC estimators may be un...

The multilevel Monte Carlo (MLMC) method for continuous-time Markov chains, first introduced by Anderson and Higham (SIAM Multiscal Model. Simul. 10(1), 2012), is a highly efficient simulation techn...

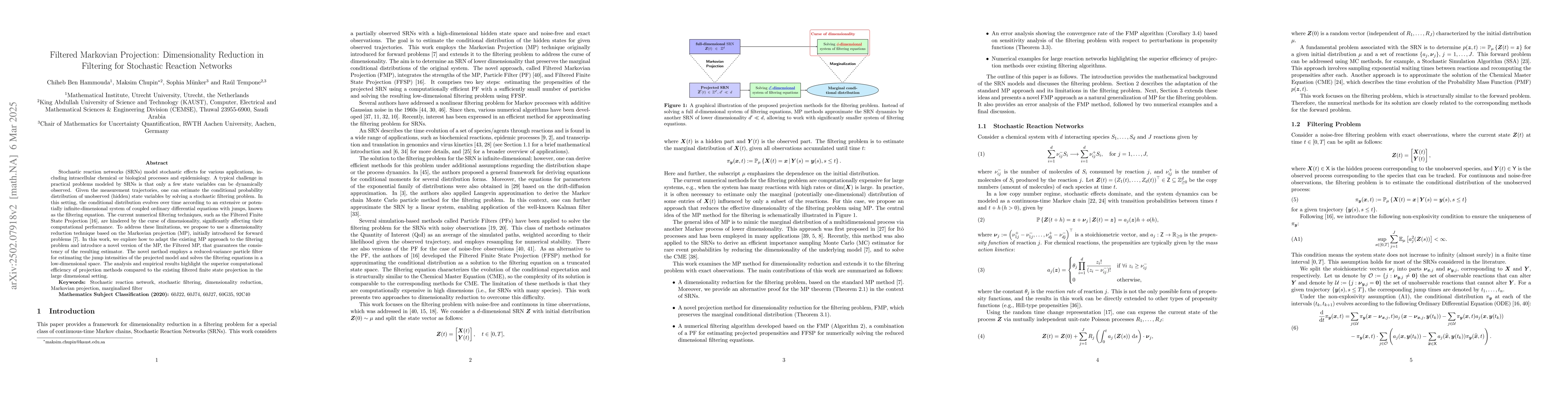

Stochastic reaction networks (SRNs) model stochastic effects for various applications, including intracellular chemical or biological processes and epidemiology. A typical challenge in practical probl...

Stochastic differential equations (SDEs) driven by fractional Brownian motion (fBm) are increasingly used to model systems with rough dynamics and long-range dependence, such as those arising in quant...

Multivariate shortfall risk measures provide a principled framework for quantifying systemic risk and determining capital allocations prior to aggregation in interconnected financial systems. Despite ...

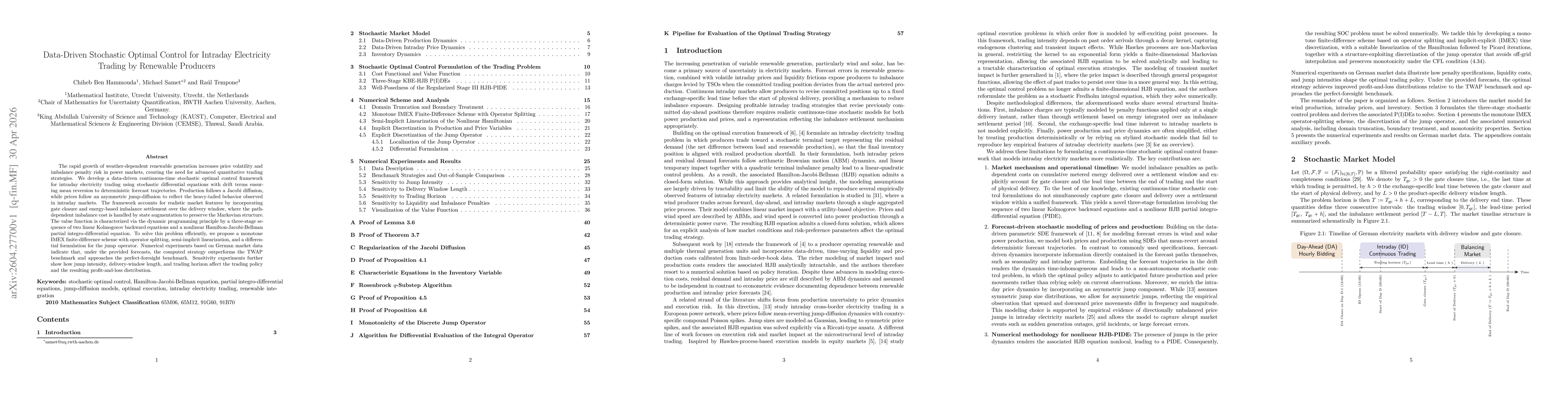

The rapid growth of weather-dependent renewable generation increases price volatility and imbalance penalty risk in power markets, creating the need for advanced quantitative trading strategies. We de...