Academic Profile

Statistics

Similar Authors

Papers on arXiv

Efficiently pricing multi-asset options poses a significant challenge in quantitative finance. The Monte Carlo (MC) method remains the prevalent choice for pricing engines; however, its slow converg...

We propose two signature-based methods to solve the optimal stopping problem - that is, to price American options - in non-Markovian frameworks. Both methods rely on a global approximation result fo...

We provide an efficient and accurate simulation scheme for the rough Heston model in the standard ($H>0$) as well as the hyper-rough regime ($H > -1/2$). The scheme is based on low-dimensional Marko...

The rough Heston model is a very popular recent model in mathematical finance; however, the lack of Markov and semimartingale properties poses significant challenges in both theory and practice. A w...

We present an adaptive algorithm for effectively solving rough differential equations (RDEs) using the log-ODE method. The algorithm is based on an error representation formula that accurately descr...

In this work, we introduce a novel pricing methodology in general, possibly non-Markovian local stochastic volatility (LSV) models. We observe that by conditioning the LSV dynamics on the Brownian m...

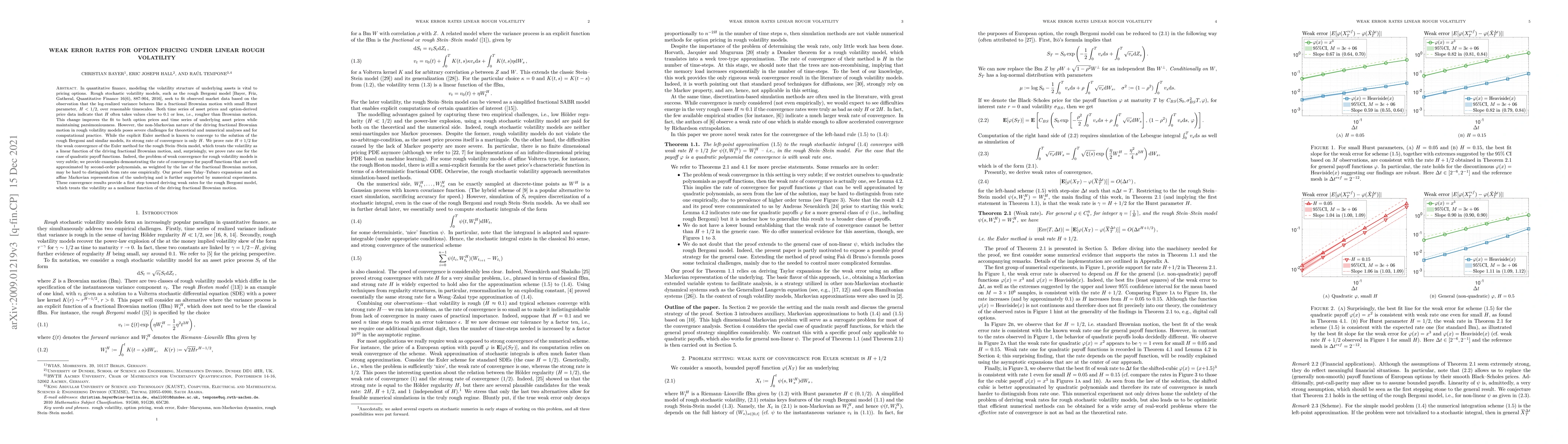

We study the weak convergence rate in the discretization of rough volatility models. After showing a lower bound $2H$ under a general model, where $H$ is the Hurst index of the volatility process, w...

Motivated by the challenges related to the calibration of financial models, we consider the problem of numerically solving a singular McKean-Vlasov equation $$ d X_t= \sigma(t,X_t) X_t \frac{\sqrt v...

Using rough path techniques, we provide a priori estimates for the output of Deep Residual Neural Networks in terms of both the input data and the (trained) network weights. As trained network weigh...

When approximating the expectations of a functional of a solution to a stochastic differential equation, the numerical performance of deterministic quadrature methods, such as sparse grid quadrature...

We consider rough stochastic volatility models where the variance process satisfies a stochastic Volterra equation with the fractional kernel, as in the rough Bergomi and the rough Heston model. In ...

We propose a new method for solving optimal stopping problems (such as American option pricing in finance) under minimal assumptions on the underlying stochastic process $X$. We consider classic a...

Least squares Monte Carlo methods are a popular numerical approximation method for solving stochastic control problems. Based on dynamic programming, their key feature is the approximation of the co...

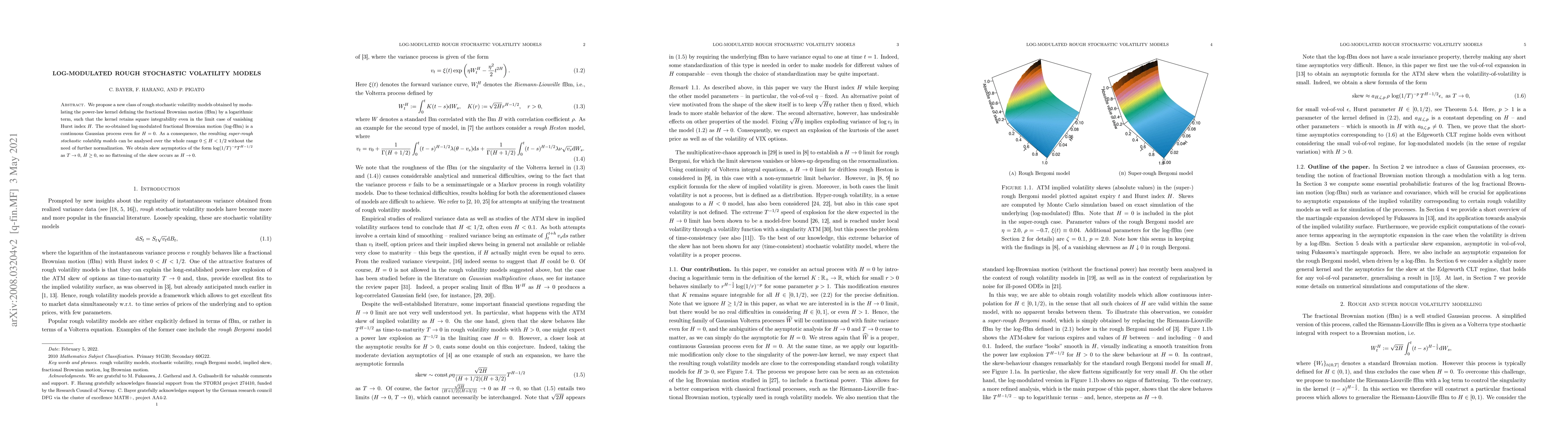

In quantitative finance, modeling the volatility structure of underlying assets is vital to pricing options. Rough stochastic volatility models, such as the rough Bergomi model [Bayer, Friz, Gathera...

We propose a new class of rough stochastic volatility models obtained by modulating the power-law kernel defining the fractional Brownian motion (fBm) by a logarithmic term, such that the kernel ret...

In this paper, we study the option pricing problems for rough volatility models. As the framework is non-Markovian, the value function for a European option is not deterministic; rather, it is rando...

We consider high-dimensional asset price models that are reduced in their dimension in order to reduce the complexity of the problem or the effect of the curse of dimensionality in the context of op...

The multilevel Monte Carlo (MLMC) method is highly efficient for estimating expectations of a functional of a solution to a stochastic differential equation (SDE). However, MLMC estimators may be un...

In this paper we study randomized optimal stopping problems and consider corresponding forward and backward Monte Carlo based optimisation algorithms. In particular we prove the convergence of the p...

Techniques from deep learning play a more and more important role for the important task of calibration of financial models. The pioneering paper by Hernandez [Risk, 2017] was a catalyst for resurfa...

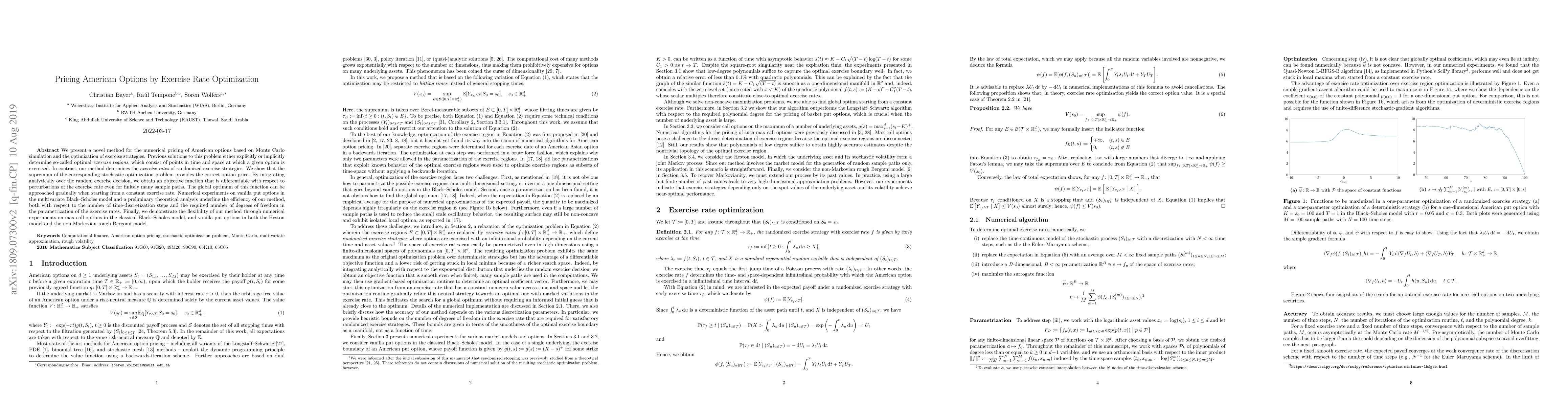

We present a novel method for the numerical pricing of American options based on Monte Carlo simulation and the optimization of exercise strategies. Previous solutions to this problem either explici...

This work addresses stochastic optimal control problems where the unknown state evolves in continuous time while partial, noisy, and possibly controllable measurements are only available in discrete t...

We show that the state spaces of multifactor Markovian processes, coming from approximations of nonnegative Volterra processes, are given by explicit linear transformation of the nonnegative orthant. ...

This paper focuses on the mathematical framework for reducing the complexity of models using path signatures. The structure of these signatures, which can be interpreted as collections of iterated int...

We extend the signature-based primal and dual solutions to the optimal stopping problem recently introduced in [Bayer et al.: Primal and dual optimal stopping with signatures, to appear in Finance & S...

We study nonparametric regression and classification for path-valued data. We introduce a functional Nadaraya-Watson estimator that combines the signature transform from rough path theory with local k...

We study a continuous time stochastic optimal control problem under partial observations that are available only at discrete time instants. This hybrid setting, with continuous dynamics and intermitte...