Academic Profile

Statistics

Similar Authors

Papers on arXiv

This work introduces a novel approach to price rainbow options, a type of path-independent multi-asset derivatives, with quantum computers. Leveraging the Iterative Quantum Amplitude Estimation meth...

The Portfolio Optimization task has long been studied in the Financial Services literature as a procedure to identify the basket of assets that satisfy desired conditions on the expected return and ...

We present a comprehensive quantum algorithm tailored for pricing autocallable options, offering a full implementation and experimental validation. Our experiments include simulations conducted on hig...

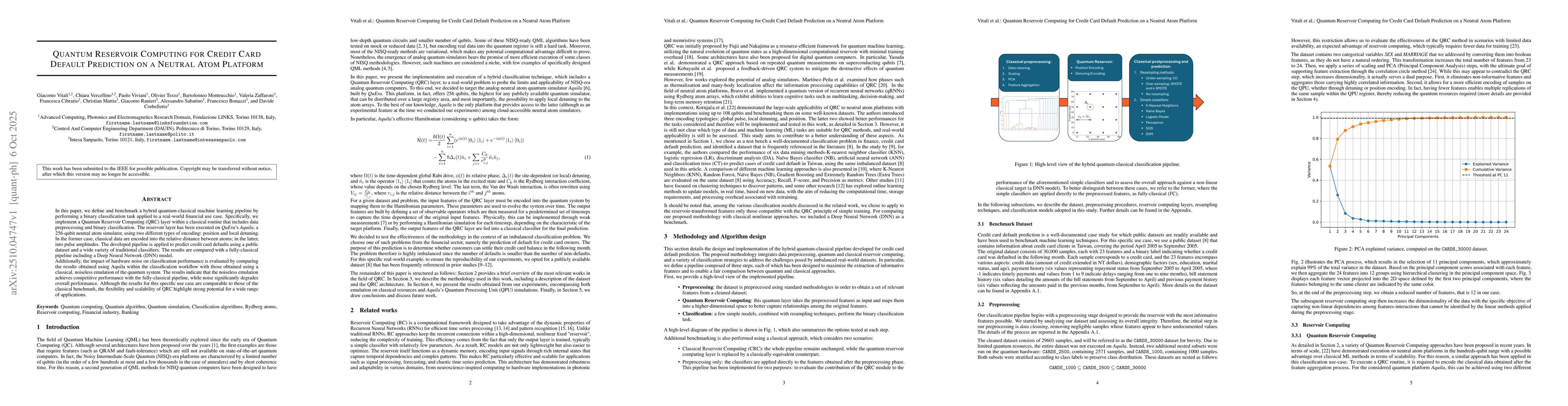

In this paper, we define and benchmark a hybrid quantum-classical machine learning pipeline by performing a binary classification task applied to a real-world financial use case. Specifically, we impl...

In finance, assessing the creditworthiness of loan applicants requires lenders to cluster borrowers using rating scales. Financial institutions must define the scales in compliance with strict institu...