Academic Profile

Statistics

Similar Authors

Papers on arXiv

By its nature, the so-called social cost of carbon (SCC(t)) will likely not cover the cost induced by climate change (damage cost and abatement cost) if it is used as a CO$_2$-price. It is a margina...

Today's decisions on climate change mitigation affect the damage that future generations will bear. Discounting future benefits and costs of climate change mitigation is one of the most critical com...

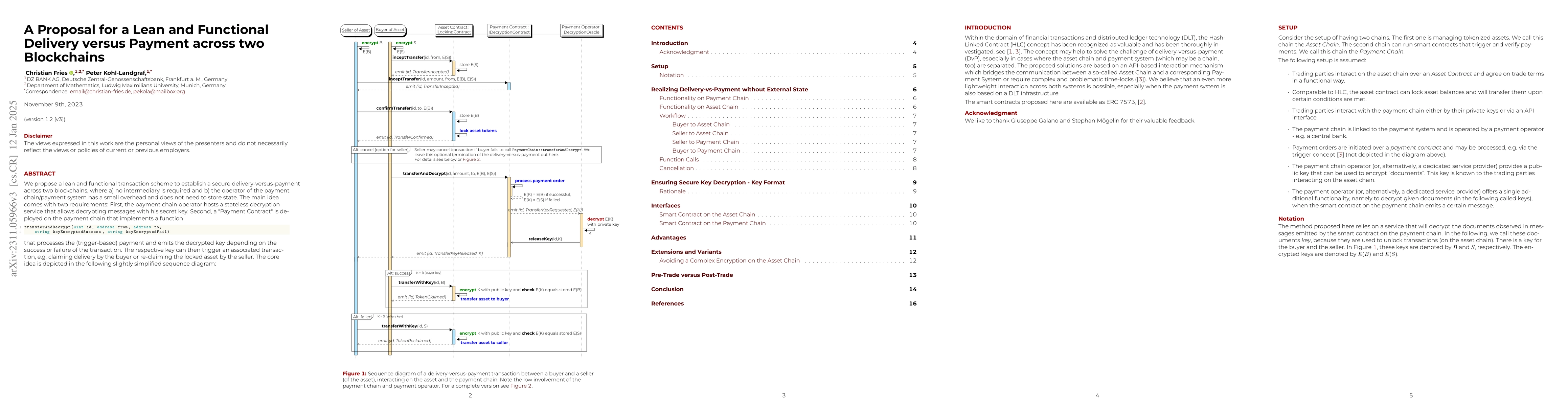

We propose a lean and functional transaction scheme to establish a secure delivery-versus-payment across two blockchains, where a) no intermediary is required and b) the operator of the payment chai...

In this paper, we introduce a model that adds a non-linearity to discounting: the discounting factor may depend on the notional (i.e., discounted values are no longer linear in the notional). In the...

We study cash-flow forecasting for derivatives used in liquidity management and clarify its relation to risk-neutral valuation and replication. While it is well known that expectations under different...