Academic Profile

Statistics

Similar Authors

Papers on arXiv

We investigate propagation of convexity and convex ordering on a typical stochastic optimal control problem, namely the pricing of \q{\emph{Take-or-Pay}} swing option, a financial derivative product...

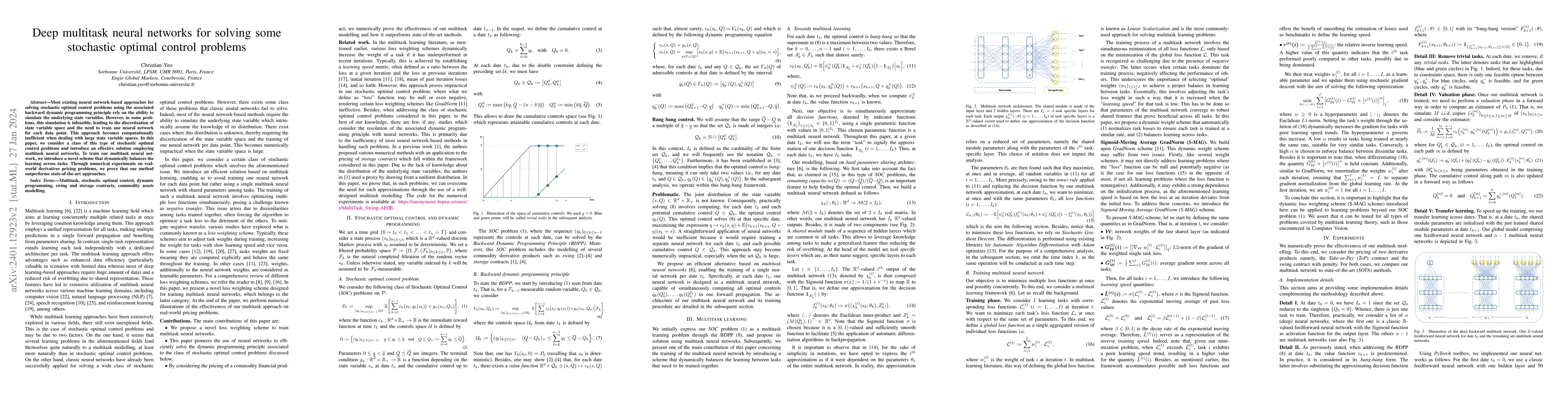

Most existing neural network-based approaches for solving stochastic optimal control problems using the associated backward dynamic programming principle rely on the ability to simulate the underlyi...

Least Squares regression was first introduced for the pricing of American-style options, but it has since been expanded to include swing options pricing. The swing options price may be viewed as a s...

We propose two parametric approaches to evaluate swing contracts with firm constraints. Our objective is to define approximations for the optimal control, which represents the amounts of energy purc...

We introduce a new class of neural networks designed to be convex functions of their inputs, leveraging the principle that any convex function can be represented as the supremum of the affine function...