Academic Profile

Statistics

Similar Authors

Papers on arXiv

We investigate mean-field games (MFG) in which agents can actively control their speed of access to information. Specifically, the agents can dynamically decide to obtain observations with reduced d...

We consider a family of McKean-Vlasov equations arising as the large particle limit of a system of interacting particles on the positive half-line with common noise and feedback. Such systems are mo...

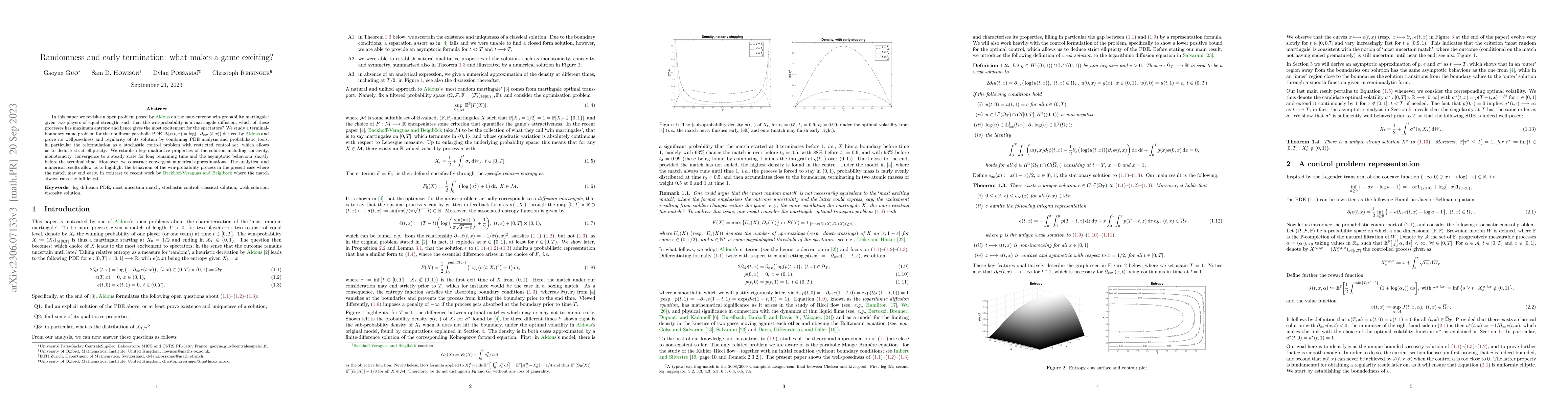

In this paper we revisit an open problem posed by Aldous on the max-entropy win-probability martingale: given two players of equal strength, such that the win-probability is a martingale diffusion, ...

In this paper, we propose a novel $K$-nearest neighbor resampling procedure for estimating the performance of a policy from historical data containing realized episodes of a decision process generat...

In this paper, we study the Euler--Maruyama scheme for a particle method to approximate the McKean--Vlasov dynamics of calibrated local-stochastic volatility (LSV) models. Given the open question of...

We study the global linear convergence of policy gradient (PG) methods for finite-horizon continuous-time exploratory linear-quadratic control (LQC) problems. The setting includes stochastic LQC pro...

We propose an explicit drift-randomised Milstein scheme for both McKean--Vlasov stochastic differential equations and associated high-dimensional interacting particle systems with common noise. By u...

We consider two implicit approximation schemes of the one-dimensional supercooled Stefan problem and prove their convergence, even in the presence of finite time blow-ups. All proofs are based on a ...

We study the capability of arbitrage-free neural-SDE market models to yield effective strategies for hedging options. In particular, we derive sensitivity-based and minimum-variance-based hedging st...

Despite its popularity in the reinforcement learning community, a provably convergent policy gradient method for continuous space-time control problems with nonlinear state dynamics has been elusive...

In this paper, we examine the capacity of an arbitrage-free neural-SDE market model to produce realistic scenarios for the joint dynamics of multiple European options on a single underlying. We subs...

We consider Markov decision processes where the state of the chain is only given at chosen observation times and of a cost. Optimal strategies involve the optimisation of observation times as well a...

We consider the problem faced by a central bank which bails out distressed financial institutions that pose systemic risk to the banking sector. In a structural default model with mutual obligations...

We propose a PDE-based accelerated gradient algorithm for optimal feedback controls of McKean-Vlasov dynamics that involve mean-field interactions both in the state and action. The method exploits a...

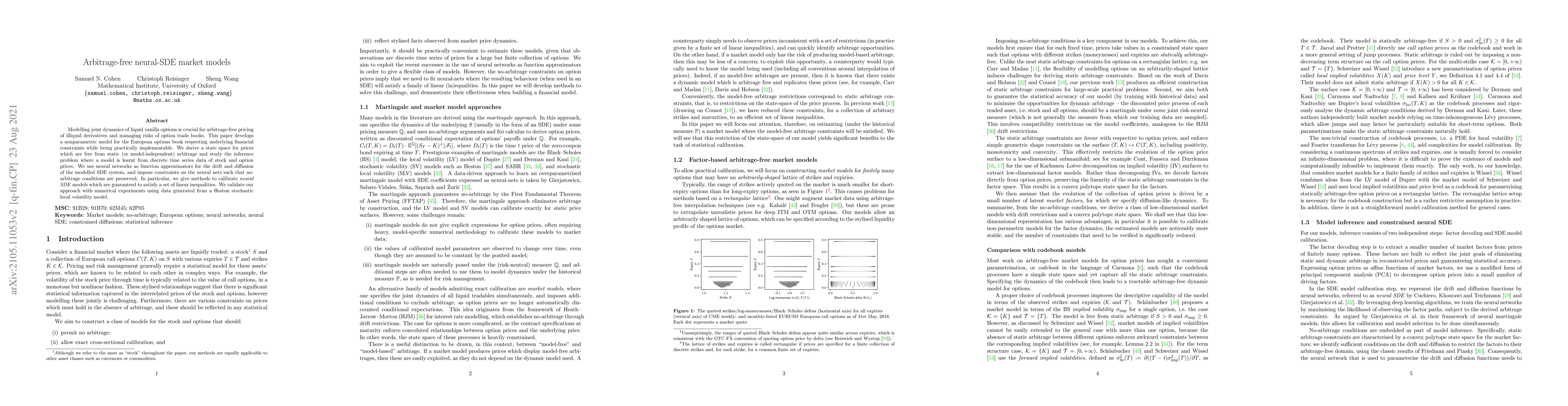

Modelling joint dynamics of liquid vanilla options is crucial for arbitrage-free pricing of illiquid derivatives and managing risks of option trade books. This paper develops a nonparametric model f...

This paper establishes H\"{o}lder time regularity of solutions to coupled McKean-Vlasov forward-backward stochastic differential equations (MV-FBSDEs). This is not only of fundamental mathematical i...

We prove the well-posedness of solutions to McKean-Vlasov stochastic differential equations driven by L\'evy noise under mild assumptions where, in particular, the L\'evy measure is not required to ...

The supercooled Stefan problem and its variants describe the freezing of a supercooled liquid in physics, as well as the large system limits of systemic risk models in finance and of integrate-and-f...

Option price data are used as inputs for model calibration, risk-neutral density estimation and many other financial applications. The presence of arbitrage in option price data can lead to poor per...

Fully coupled McKean-Vlasov forward-backward stochastic differential equations (MV-FBSDEs) arise naturally from large population optimization problems. Judging the quality of given numerical solutio...

In this paper, we first establish well-posedness results for one-dimensional McKean-Vlasov stochastic differential equations (SDEs) and related particle systems with a measure-dependent drift coeffi...

Recently, there has been a surge of interest in combining deep learning models with reasoning in order to handle more sophisticated learning tasks. In many cases, a reasoning task can be solved by a...

In this paper, we first establish well-posedness of McKean-Vlasov stochastic differential equations (McKean-Vlasov SDEs) with common noise, possibly with coefficients having super-linear growth in t...

In this paper, we introduce adaptive Euler-Maruyama schemes for McKean-Vlasov stochastic differential equations (SDEs) assuming only a standard monotonicity condition on the drift and diffusion coef...

In this paper, we present a novel computational framework for portfolio-wide risk management problems, where the presence of a potentially large number of risk factors makes traditional numerical te...

In this paper, we first derive Milstein schemes for an interacting particle system associated with point delay McKean-Vlasov stochastic differential equations (McKean-Vlasov SDEs), possibly with a d...

This paper proposes a relaxed control regularization with general exploration rewards to design robust feedback controls for multi-dimensional continuous-time stochastic exit time problems. We estab...

We consider a Markov chain approximation scheme for utility maximization problems in continuous time, which uses, in turn, a piecewise constant policy approximation, Euler-Maruyama time stepping, an...

We propose a generic calibration framework to both vanilla and no-touch options for a large class of continuous semi-martingale models. The method builds upon the forward partial integro-differentia...

We consider the numerical approximation of the quantile hedging price in a non-linear market. In a Markovian framework, we propose a numerical method based on a Piecewise Constant Policy Timesteppin...

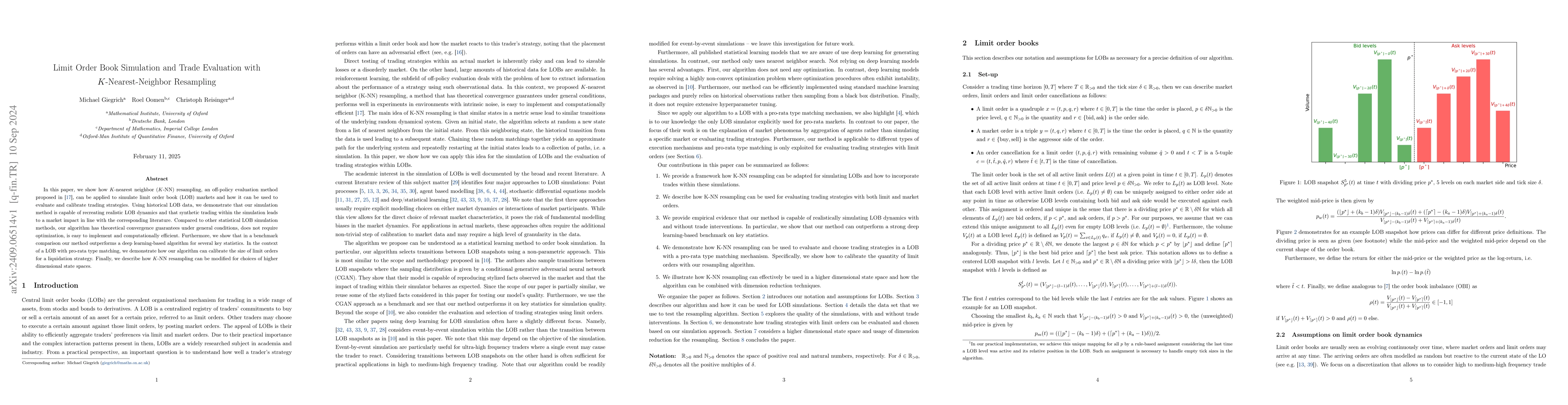

In this paper, we show how $K$-nearest neighbor ($K$-NN) resampling, an off-policy evaluation method proposed in \cite{giegrich2023k}, can be applied to simulate limit order book (LOB) markets and how...

In this work, we present a general Milstein-type scheme for McKean-Vlasov stochastic differential equations (SDEs) driven by Brownian motion and Poisson random measure and the associated system of int...

We analyse a Monte Carlo particle method for the simulation of the calibrated Heston-type local stochastic volatility (H-LSV) model. The common application of a kernel estimator for a conditional expe...

Designing efficient learning algorithms with complexity guarantees for Markov decision processes (MDPs) with large or continuous state and action spaces remains a fundamental challenge. We address thi...

Conditional flow matching (CFM) has emerged as a powerful framework for training continuous normalizing flows due to its computational efficiency and effectiveness. However, standard CFM often produce...

We consider a data-driven formulation of the classical discrete-time stochastic control problem. Our approach exploits the natural structure of many such problems, in which significant portions of the...

Piecewise constant control approximation provides a practical framework for designing numerical schemes of continuous-time control problems. We analyze the accuracy of such approximations for extended...

We show that a generalised sparse grid combination technique which combines multi-variate extrapolation of finite difference solutions with the standard combination formula lifts a second order accura...

We study model-free policy learning for discrete-time mean-field control (MFC) problems with finite state space and compact action space. In contrast to the extensive literature on value-based methods...

We study the large-depth limit of transformers trained with AdamW, by modelling the hidden-state dynamics as an interacting particle system (IPS) coupled through the attention mechanism. Under appropr...