Academic Profile

Statistics

Similar Authors

Papers on arXiv

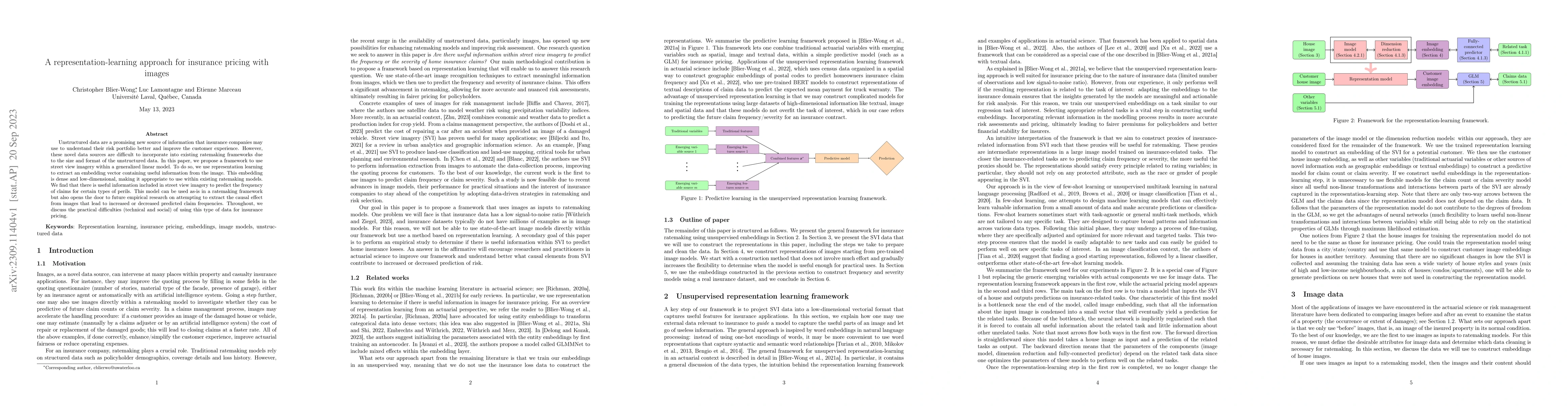

Unstructured data are a promising new source of information that insurance companies may use to understand their risk portfolio better and improve the customer experience. However, these novel data ...

We propose an approach to construct a new family of generalized Farlie-Gumbel-Morgenstern (GFGM) copulas that naturally scales to high dimensions. A GFGM copula can model moderate positive and negat...

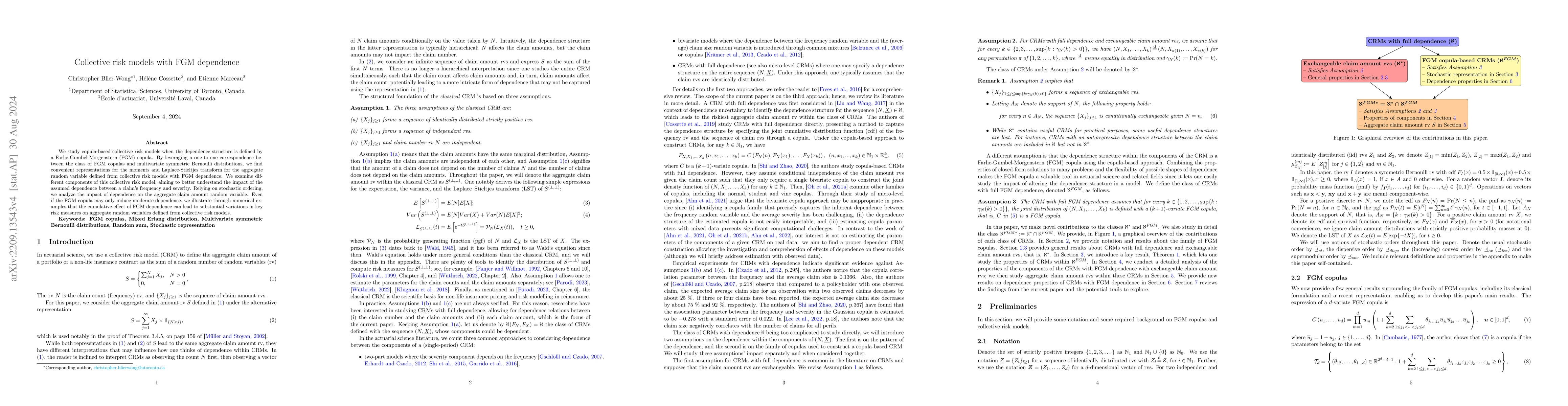

We study copula-based collective risk models when the dependence structure is defined by a Farlie-Gumbel-Morgenstern (FGM) copula. By leveraging a one-to-one correspondence between the class of FGM ...

We offer a new perspective on risk aggregation with FGM copulas. Along the way, we discover new results and revisit existing ones, providing simpler formulas than one can find in the existing litera...

Consider a risk portfolio with aggregate loss random variable $S=X_1+\dots +X_n$ defined as the sum of the $n$ individual losses $X_1, \dots, X_n$. The expected allocation, $E[X_i \times 1_{\{S = k\...

Copulas are a powerful tool to model dependence between the components of a random vector. One well-known class of copulas when working in two dimensions is the Farlie-GumbelMorgenstern (FGM) copula...

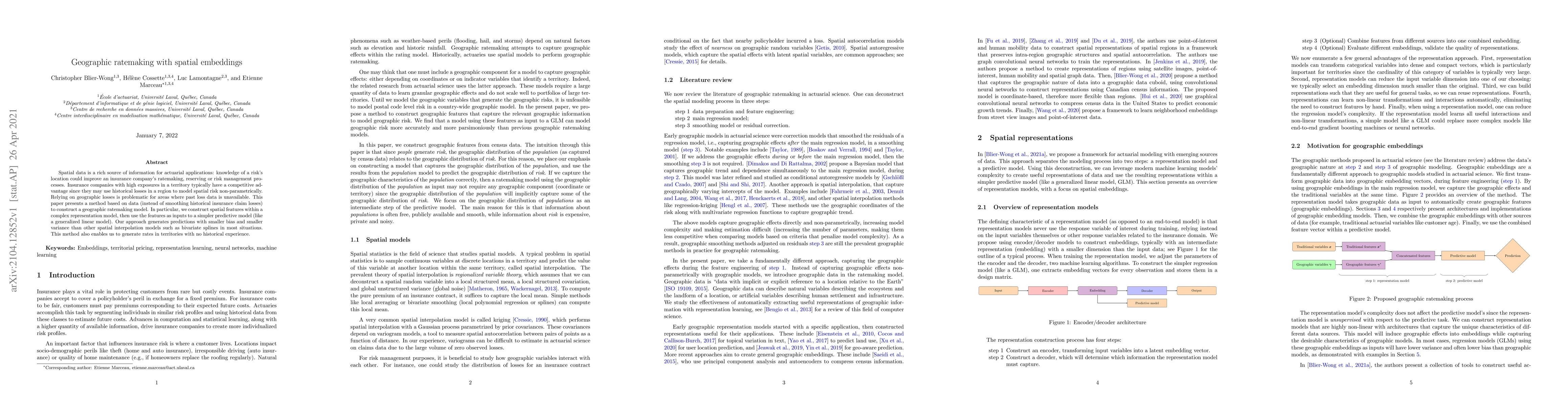

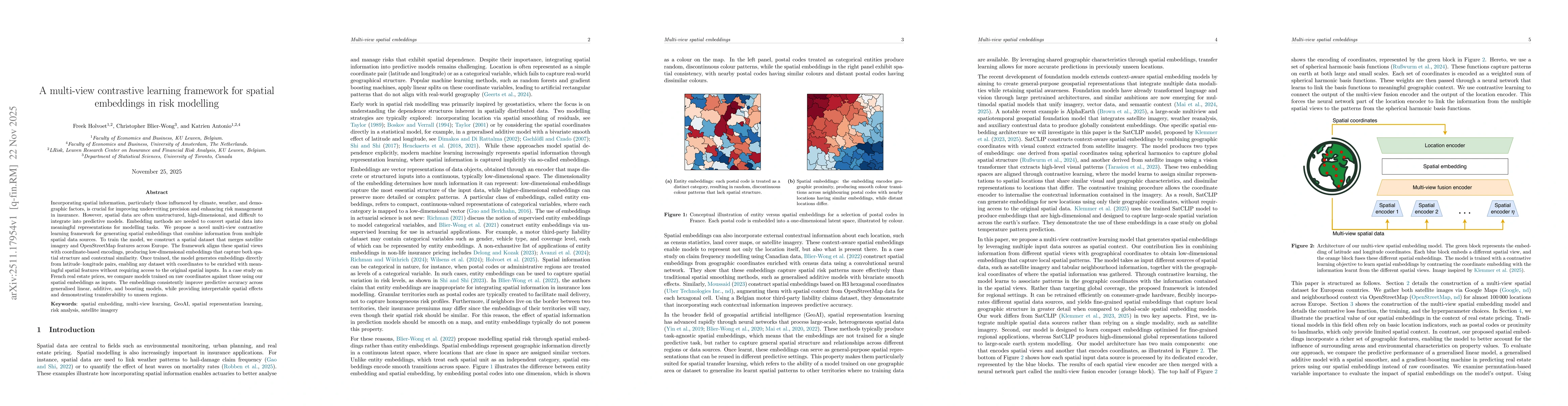

Spatial data is a rich source of information for actuarial applications: knowledge of a risk's location could improve an insurance company's ratemaking, reserving or risk management processes. Insur...

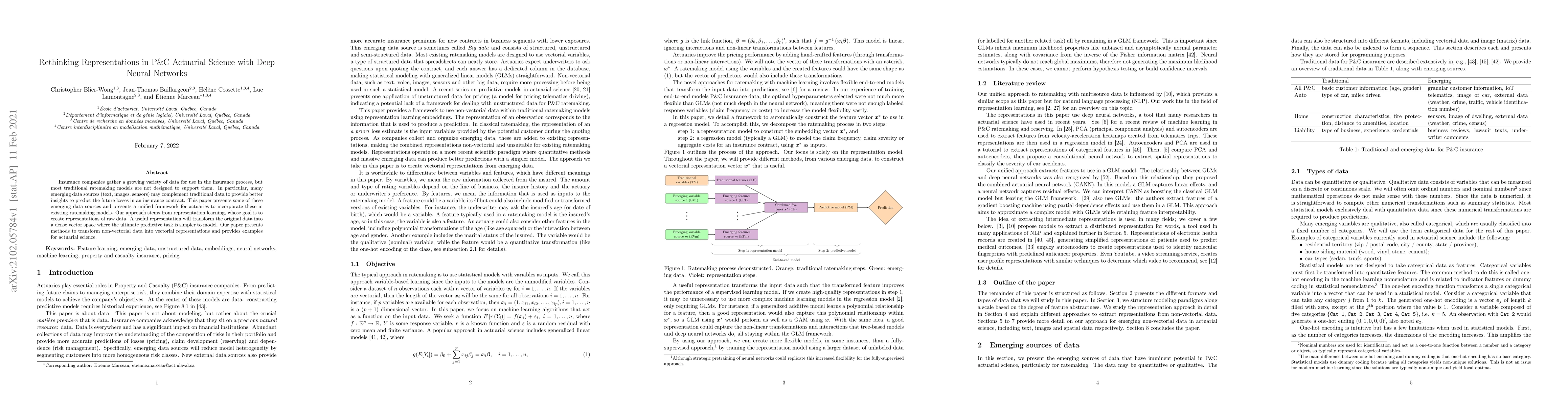

Insurance companies gather a growing variety of data for use in the insurance process, but most traditional ratemaking models are not designed to support them. In particular, many emerging data sour...

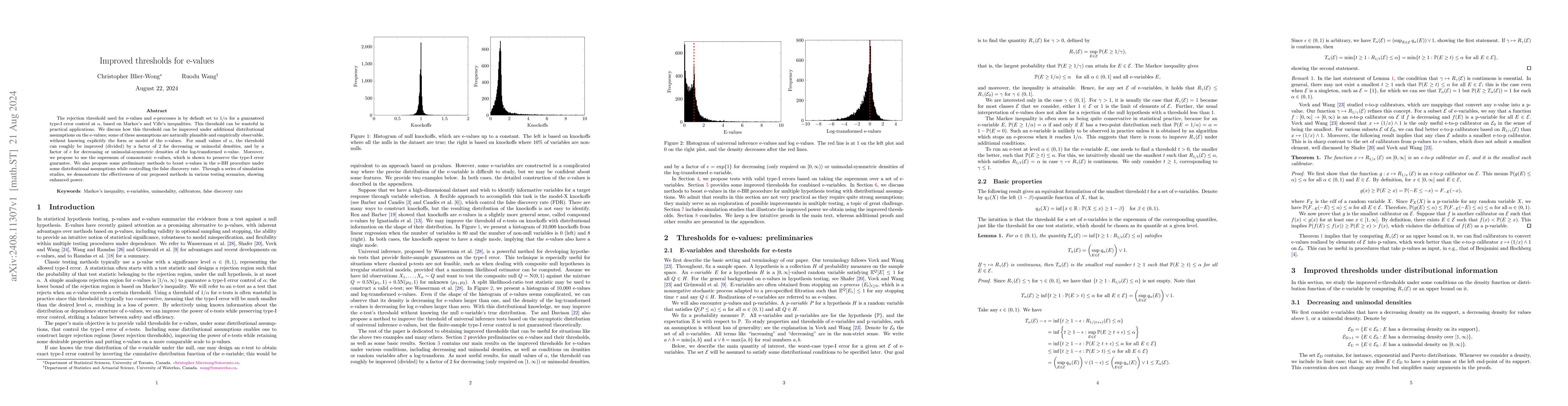

The rejection threshold used for e-values and e-processes is by default set to $1/\alpha$ for a guaranteed type-I error control at $\alpha$, based on Markov's and Ville's inequalities. This threshold ...

Incorporating spatial information, particularly those influenced by climate, weather, and demographic factors, is crucial for improving underwriting precision and enhancing risk management in insuranc...

Sarmanov copulas offer a simple and tractable way to build multivariate distributions by perturbing the independence copula. They admit closed-form expressions for densities and many functionals of in...

The conditional mean risk-sharing (CMRS) rule is an important tool for distributing aggregate losses across individual risks, but its implementation in continuous multivariate models typically require...

We study the sharp bounds of $\mathbb{E}[X_1\cdots X_d]$ when the univariate marginal distributions are known, but the dependence structure between them is unspecified. Maximizing products over non-ne...

Regulatory and contractual constraints on individual exposures are standard in insurance and reinsurance markets, but a poorly designed constraint can distort the economic incentives of risk-averse ag...

While risk pooling lowers the total cost of risk, efficiency alone does not make a pool viable. Participants need terms that ensure their participation, that are immune to subgroups breaking away, and...

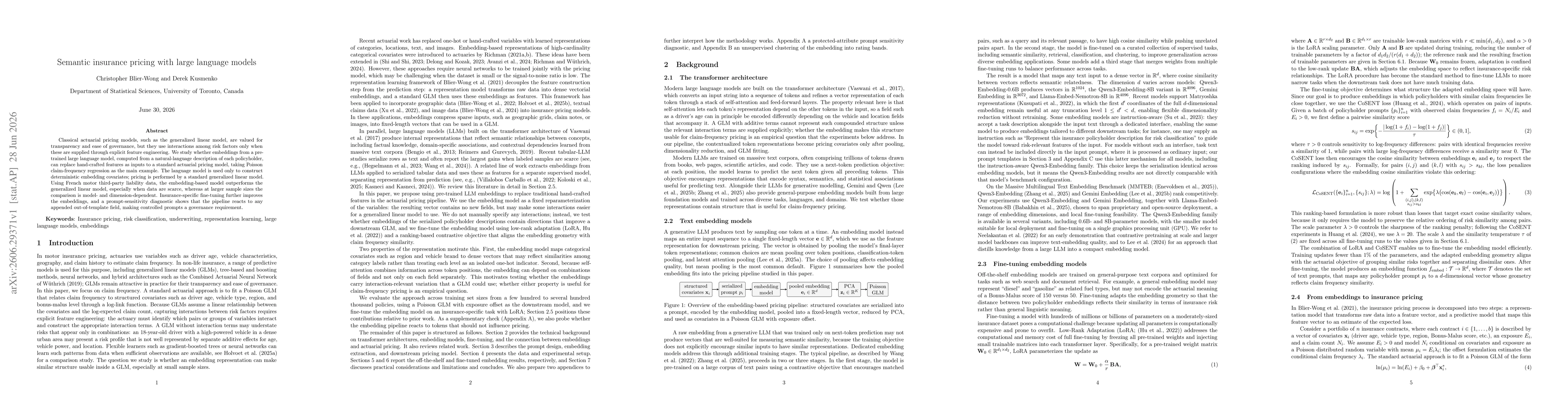

Classical actuarial pricing models, such as the generalized linear model, are valued for transparency and ease of governance, but they use interactions among risk factors only when these are supplied ...

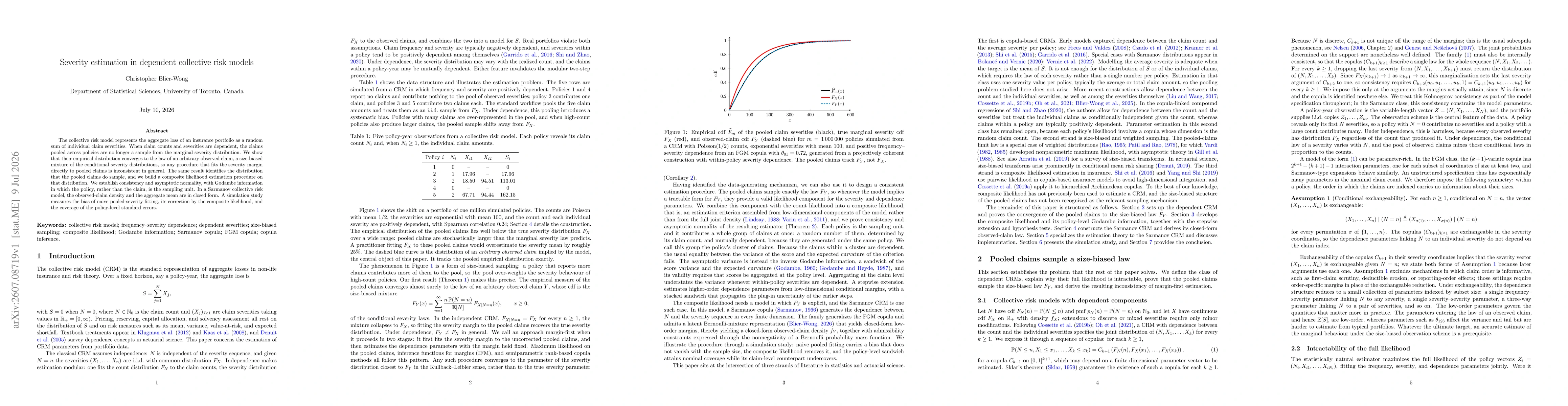

The collective risk model represents the aggregate loss of an insurance portfolio as a random sum of individual claim severities. When claim counts and severities are dependent, the claims pooled acro...