Academic Profile

Statistics

Similar Authors

Papers on arXiv

Numerous robust estimators exist as alternatives to the maximum likelihood estimator (MLE) when a completely observed ground-up loss severity sample dataset is available. However, the options for ro...

When constructing parametric models to predict the cost of future claims, several important details have to be taken into account: (i) models should be designed to accommodate deductibles, policy li...

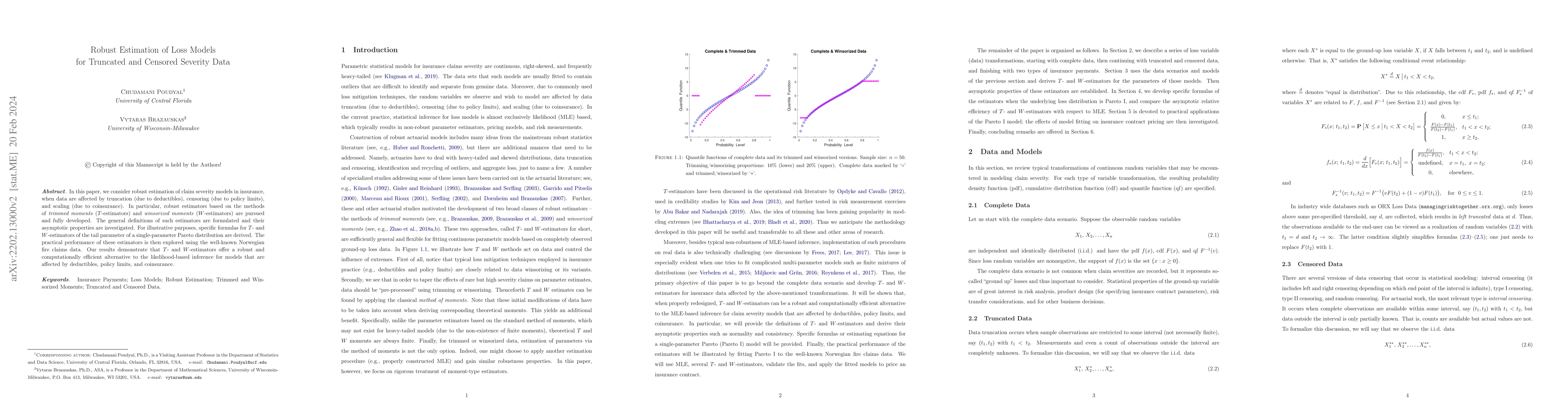

In this paper, we consider robust estimation of claim severity models in insurance, when data are affected by truncation (due to deductibles), censoring (due to policy limits), and scaling (due to c...

The primary objective of this scholarly work is to develop two estimation procedures - maximum likelihood estimator (MLE) and method of trimmed moments (MTM) - for the mean and variance of lognormal...

With some regularity conditions maximum likelihood estimators (MLEs) always produce asymptotically optimal (in the sense of consistency, efficiency, sufficiency, and unbiasedness) estimators. But in...

Statistical modeling of claim severity distributions is essential in insurance and risk management, where achieving a balance between robustness and efficiency in parameter estimation is critical agai...

This paper proposes a robust and computationally efficient estimation framework for fitting parametric distributions based on trimmed L-moments. Trimmed L-moments extend classical L-moment theory by d...