Academic Profile

Statistics

Similar Authors

Papers on arXiv

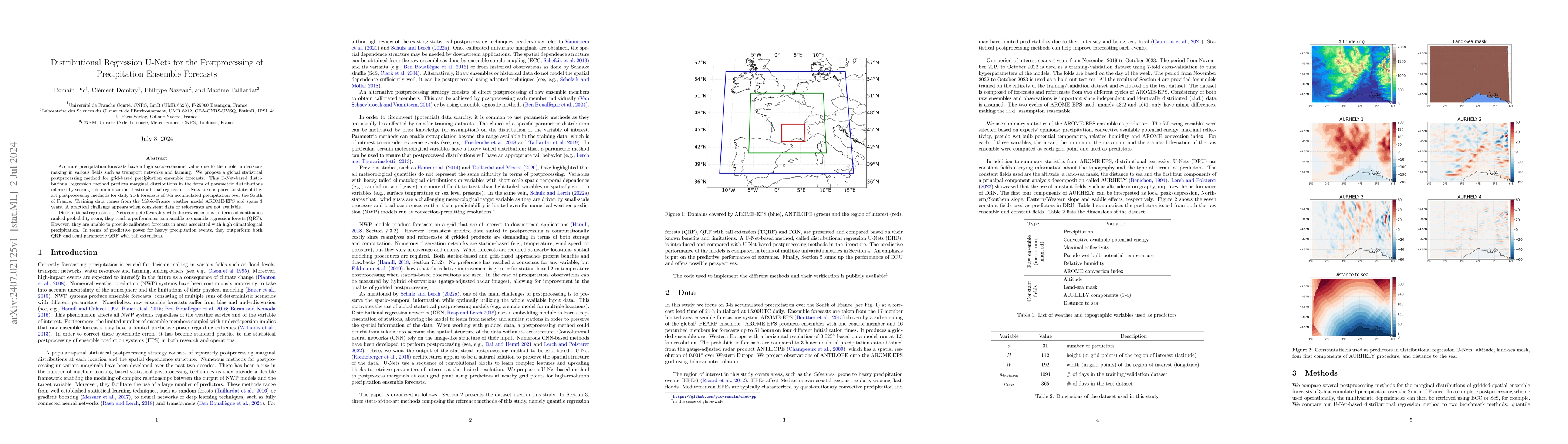

Accurate precipitation forecasts have a high socio-economic value due to their role in decision-making in various fields such as transport networks and farming. We propose a global statistical postpro...

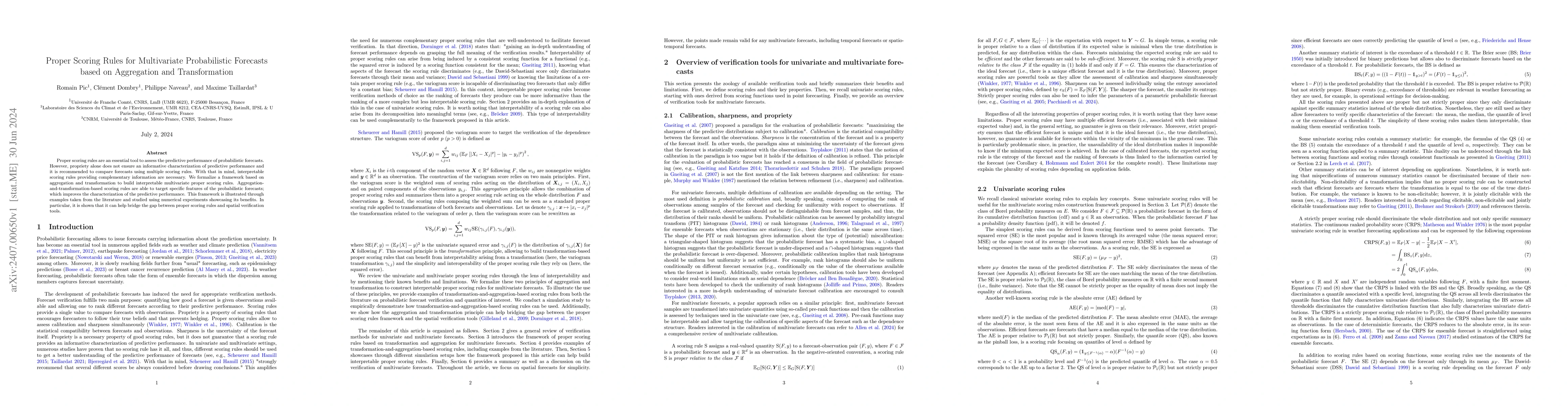

Proper scoring rules are an essential tool to assess the predictive performance of probabilistic forecasts. However, propriety alone does not ensure an informative characterization of predictive per...

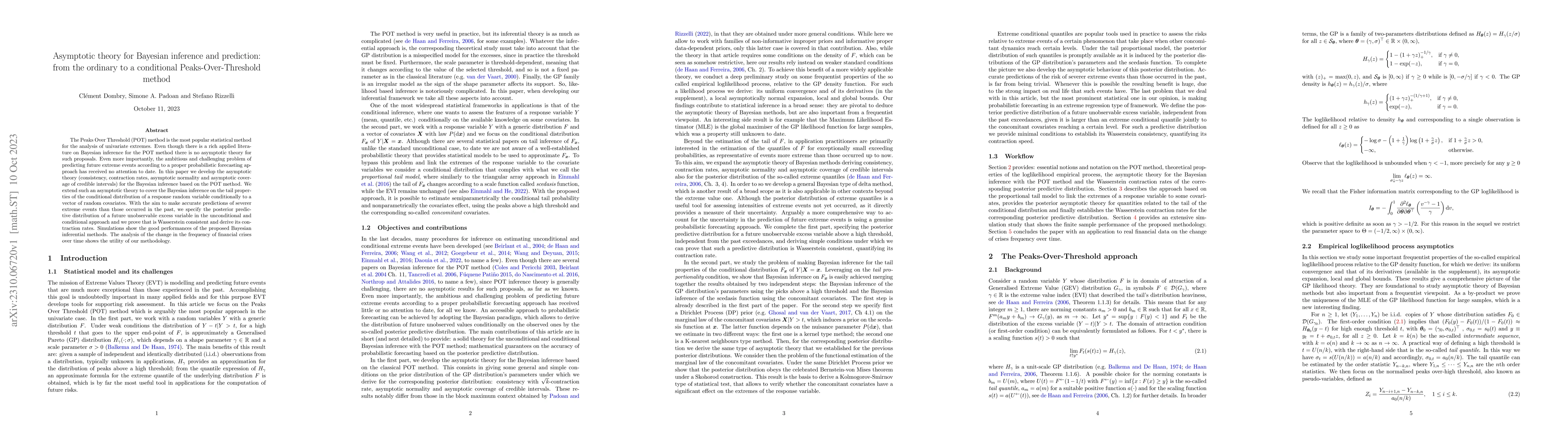

The Peaks Over Threshold (POT) method is the most popular statistical method for the analysis of univariate extremes. Even though there is a rich applied literature on Bayesian inference for the POT...

Introduction: The Oncotype DX (ODX) test is a commercially available molecular test for breast cancer assay that provides prognostic and predictive breast cancer recurrence information for hormone p...

We extend the celebrated Stone's theorem to the framework of distributional regression. More precisely, we prove that weighted empirical distribution with local probability weights satisfying the co...

The theoretical advances on the properties of scoring rules over the past decades have broadened the use of scoring rules in probabilistic forecasting. In meteorological forecasting, statistical pos...

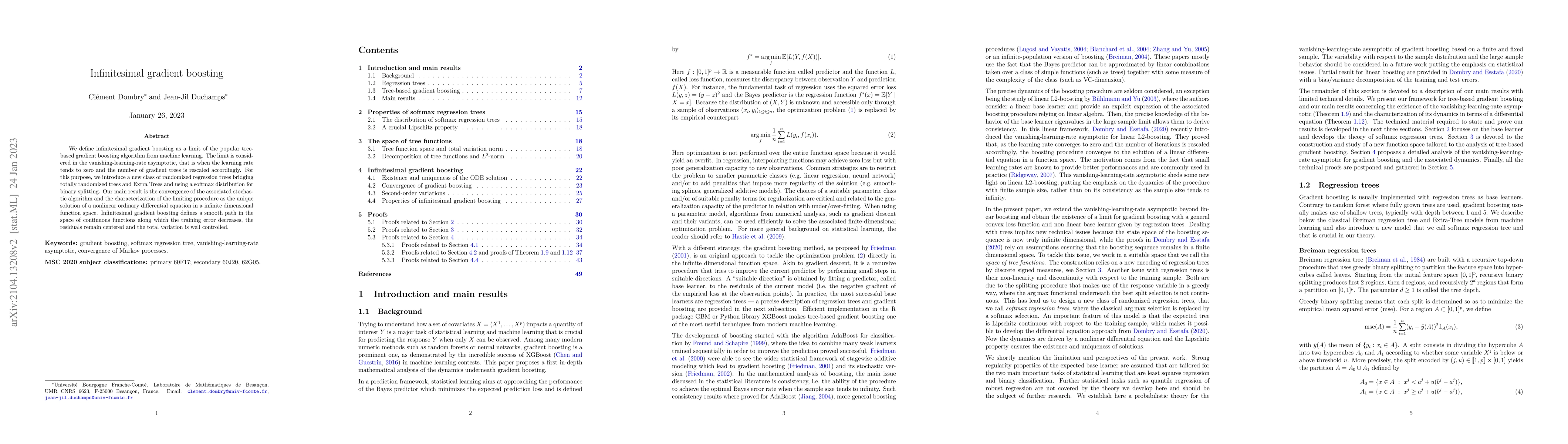

We define infinitesimal gradient boosting as a limit of the popular tree-based gradient boosting algorithm from machine learning. The limit is considered in the vanishing-learning-rate asymptotic, t...

Extreme quantile regression provides estimates of conditional quantiles outside the range of the data. Classical quantile regression performs poorly in such cases since data in the tail region are t...

We consider regular variation for marked point processes with independent heavy-tailed marks and prove a single large point heuristic: the limit measure is concentrated on the cone of point measures...

We investigate the asymptotic behaviour of gradient boosting algorithms when the learning rate converges to zero and the number of iterations is rescaled accordingly. We mostly consider L2-boosting ...

We revisit the model of heteroscedastic extremes initially introduced by Einmahl et al. (JRSSB, 2016) to describe the evolution of a non stationary sequence whose extremes evolve over time and adapt...

A coupling method is developed for univariate extreme value theory , providing an alternative to the use of the tail empirical/quantile processes. Emphasizing the Peak-over-Threshold approach that a...

Distributional regression aims at estimating the conditional distribution of a targetvariable given explanatory co-variates. It is a crucial tool for forecasting whena precise uncertainty quantificati...

This paper investigates predictive probability inference for classification tasks using random forests in the context of imbalanced data. In this setting, we analyze the asymptotic properties of simpl...

Selective prediction, where a model has the option to abstain from making a decision, is crucial for machine learning applications in which mistakes are costly. In this work, we focus on distributiona...

We study quantile regression in an extrapolation regime where the covariate takes unusually large values. Under regular variation assumptions, extreme observations can be effectively characterized thr...

Building on the large-sample analysis of infinitesimal gradient boosting (Dombry and Duchamps, 2024b), we study the fluctuations of the process around its deterministic limit and establish a functiona...