Academic Profile

Statistics

Similar Authors

Papers on arXiv

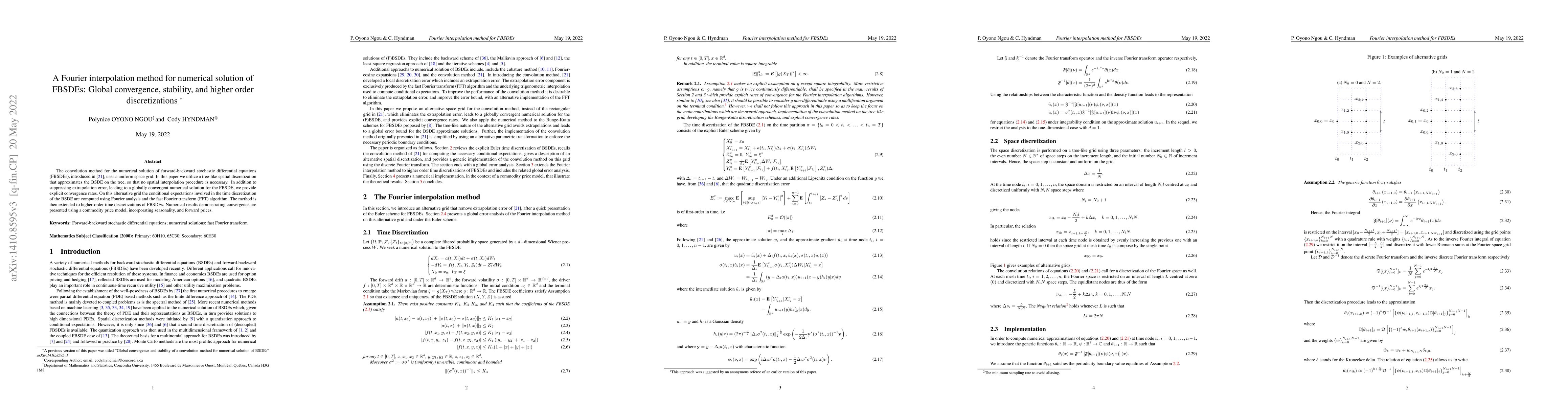

The convolution method for the numerical solution of forward-backward stochastic differential equations (FBSDEs), introduced in [21], uses a uniform space grid. In this paper we utilize a tree-like ...

We consider the problem of simultaneously approximating the conditional distribution of market prices and their log returns with a single machine learning model. We show that an instance of the GDN ...

Evidence shows that the labor participation rate of retirement age cohorts is non-negligible, and it is a widespread phenomenon globally. In the United States, the labor force participation rate for...

Effective feature representation is key to the predictive performance of any algorithm. This paper introduces a meta-procedure, called Non-Euclidean Upgrading (NEU), which learns feature maps that a...

We consider the problem of optimal annuitization with labour income, where an agent aims to maximize utility from consumption and labour income under age-dependent force of mortality. Using a dynamic ...

We develop an arbitrage-free deep learning framework for yield curve and bond price forecasting based on the Heath-Jarrow-Morton (HJM) term-structure model and a dynamic Nelson-Siegel parameterization...

We propose a convolution-FFT method for pricing European options under the Heston model that leverages a continuously differentiable representation of the joint characteristic function. Unlike existin...

We first review the convolution fast-Fourier-transform (CFFT) approach for the numerical solution of backward stochastic differential equations (BSDEs) introduced in (Hyndman and Oyono Ngou, 2017). We...

The decision to annuitize wealth in retirement planning has become increasingly complex due to rising longevity risk and changing retirement patterns, including increased labor force participation at ...