A Fourier interpolation method for numerical solution of FBSDEs: Global convergence, stability, and higher order discretizations

Publication

Metrics

AI Quick Summary

Researchers developed a new Fourier interpolation method to solve forward-backward stochastic differential equations (FBSDEs), achieving global convergence and explicit convergence rates, with potential applications in finance and beyond.

Paper Preview

Abstract

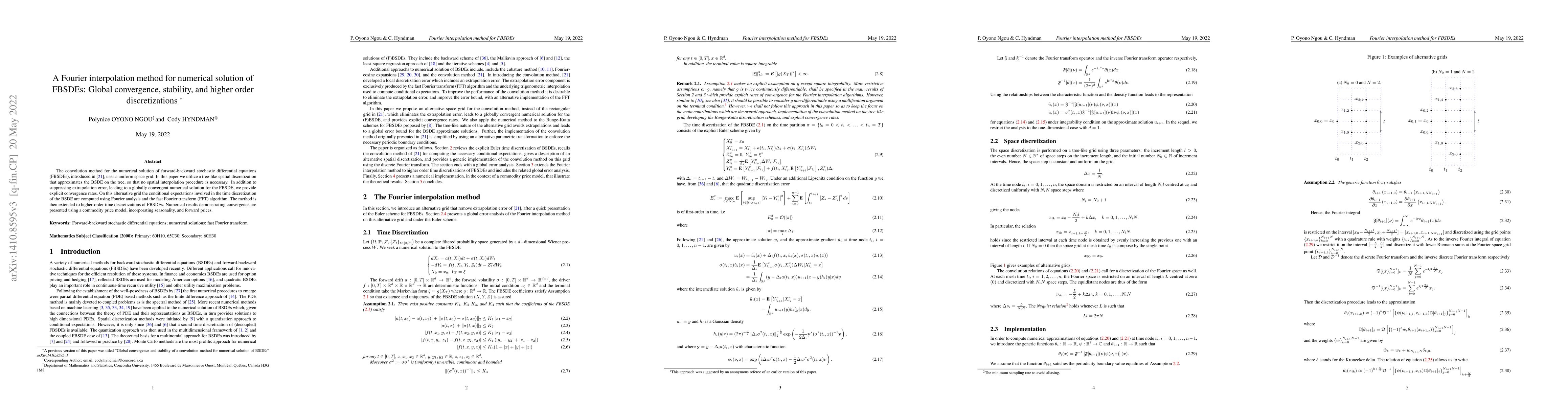

The convolution method for the numerical solution of forward-backward stochastic differential equations (FBSDEs), introduced in [21], uses a uniform space grid. In this paper we utilize a tree-like spatial discretization that approximates the BSDE on the tree, so that no spatial interpolation procedure is necessary. In addition to suppressing extrapolation error, leading to a globally convergent numerical solution for the FBSDE, we provide explicit convergence rates. On this alternative grid the conditional expectations involved in the time discretization of the BSDE are computed using Fourier analysis and the fast Fourier transform (FFT) algorithm. The method is then extended to higher-order time discretizations of FBSDEs. Numerical results demonstrating convergence are presented using a commodity price model, incorporating seasonality, and forward prices.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0