Academic Profile

Statistics

Similar Authors

Papers on arXiv

Let $\Omega$ be a Polish space with Borel $\sigma$-field $\mathcal{F}$ and countably generated sub $\sigma$-field $\mathcal{G}\subset\mathcal{F}$. Denote by $\mathcal{L}(\mathcal{F})$ the set of all...

We address the problem of estimating the expected shortfall risk of a financial loss using a finite number of i.i.d. data. It is well known that the classical plug-in estimator suffers from poor sta...

We examine nonlinear Kolmogorov partial differential equations (PDEs). Here the nonlinear part of the PDE comes from its Hamiltonian where one maximizes over all possible drift and diffusion coeffic...

We show that under minimal assumption on a class of functions $\mathcal{H}$ defined on a probability space $(\mathcal{X},\mu)$, there is a threshold $\Delta_0$ satisfying the following: for every $\...

We examine optimization problems in which an investor has the opportunity to trade in $d$ stocks with the goal of maximizing her worst-case cost of cumulative gains and losses. Here, worst-case refe...

We construct the first non-gaussian ensemble that yields the optimal estimate in the Dvoretzky-Milman Theorem: the ensemble exhibits almost Euclidean sections in arbitrary normed spaces of the same ...

Let $G_1,\dots,G_m$ be independent copies of the standard gaussian random vector in $\mathbb{R}^d$. We show that there is an absolute constant $c$ such that for any $A \subset S^{d-1}$, with probabi...

Let $X$ be a real-valued random variable with distribution function $F$. Set $X_1,\dots, X_m$ to be independent copies of $X$ and let $F_m$ be the corresponding empirical distribution function. We s...

We show that under minimal assumptions on a random vector $X\in\mathbb{R}^d$ and with high probability, given $m$ independent copies of $X$, the coordinate distribution of each vector $(\langle X_i,...

We analyze the effect of small changes in the underlying probabilistic model on the value of multi-period stochastic optimization problems and optimal stopping problems. We work in finite discrete t...

Let $X$ be a symmetric, isotropic random vector in $\mathbb{R}^m$ and let $X_1...,X_n$ be independent copies of $X$. We show that under mild assumptions on $\|X\|_2$ (a suitable thin-shell bound) an...

Wasserstein distance induces a natural Riemannian structure for the probabilities on the Euclidean space. This insight of classical transport theory is fundamental for tremendous applications in var...

We develop a novel procedure for estimating the optimizer of general convex stochastic optimization problems of the form $\min_{x\in\mathcal{X}} \mathbb{E}[F(x,\xi)]$, when the given data is a finit...

In this paper we present a duality theory for the robust utility maximisation problem in continuous time for utility functions defined on the positive real axis. Our results are inspired by -- and c...

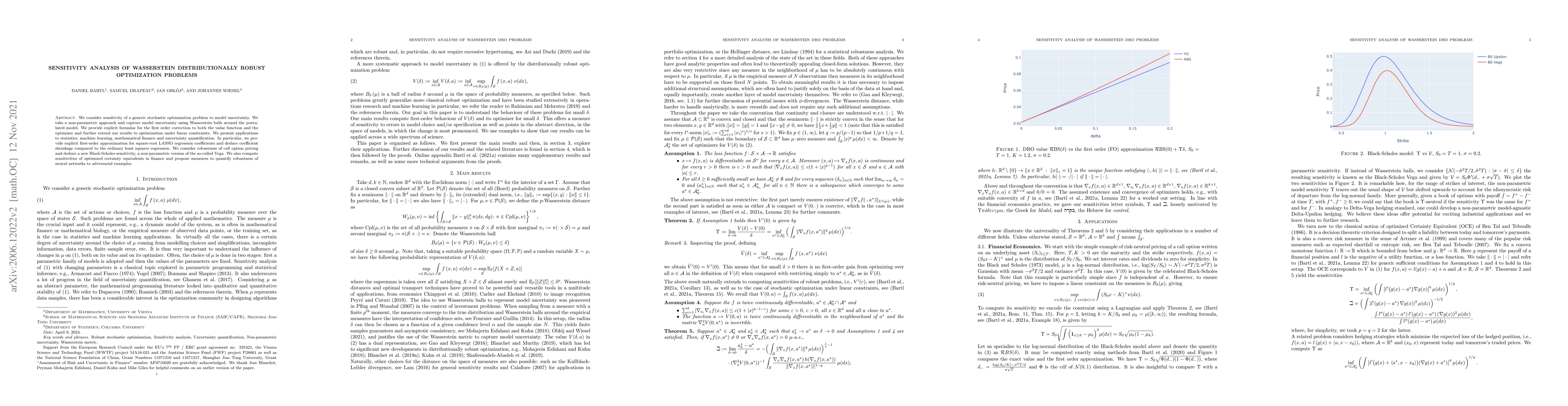

We consider sensitivity of a generic stochastic optimization problem to model uncertainty. We take a non-parametric approach and capture model uncertainty using Wasserstein balls around the postulat...

Let $\rho$ be a general law--invariant convex risk measure, for instance the average value at risk, and let $X$ be a financial loss, that is, a real random variable. In practice, either the true dis...

A number of researchers have independently introduced topologies on the set of laws of stochastic processes that extend the usual weak topology. Depending on the respective scientific background thi...

In this article we derive Talagrand's $T_2$ inequality on the path space w.r.t. the maximum norm for various stochastic processes, including solutions of one-dimensional stochastic differential equa...

A number of researchers have introduced topological structures on the set of laws of stochastic processes. A unifying goal of these authors is to strengthen the usual weak topology in order to adequ...

Assume that an agent models a financial asset through a measure Q with the goal to price / hedge some derivative or optimize some expected utility. Even if the model Q is chosen in the most skilful ...

The goal of this paper is to define stochastic integrals and to solve stochastic differential equations for typical paths taking values in a possibly infinite dimensional separable Hilbert space wit...

In this paper we provide a pricing-hedging duality for the model-independent superhedging price with respect to a prediction set $\Xi\subseteq C[0,T]$, where the superhedging property needs to hold ...

We provide a model-free pricing-hedging duality in continuous time. For a frictionless market consisting of $d$ risky assets with continuous price trajectories, we show that the purely analytic prob...

Researchers from different areas have independently defined extensions of the usual weak convergence of laws of stochastic processes with the goal of adequately accounting for the flow of information....

We study the fundamental problem of learning with respect to the squared loss in a convex class. The state-of-the-art sample complexity estimates in this setting rely on Rademacher complexities, which...

We introduce an empirical functional $\Psi$ that is an optimal uniform mean estimator: Let $F\subset L_2(\mu)$ be a class of mean zero functions, $u$ is a real valued function, and $X_1,\dots,X_N$ are...

Estimating the mean of a random vector from i.i.d. data has received considerable attention, and the optimal accuracy one may achieve with a given confidence is fairly well understood by now. When the...

Using i.i.d. data to estimate a high-dimensional distribution in Wasserstein distance is a fundamental instance of the curse of dimensionality. We explore how structural knowledge about the data-gener...

The adapted Bures--Wasserstein space consists of Gaussian processes endowed with the adapted Wasserstein distance. It can be viewed as the analogue of the classical Bures--Wasserstein space in optimal...

Let $G, G_1,\dots,G_N$ be independent copies of a standard gaussian random vector in $\mathbb{R}^d$ and denote by $Γ= \sum_{i=1}^N \langle G_i,\cdot\rangle e_i$ the standard gaussian ensemble. We show...