Academic Profile

Statistics

Similar Authors

Papers on arXiv

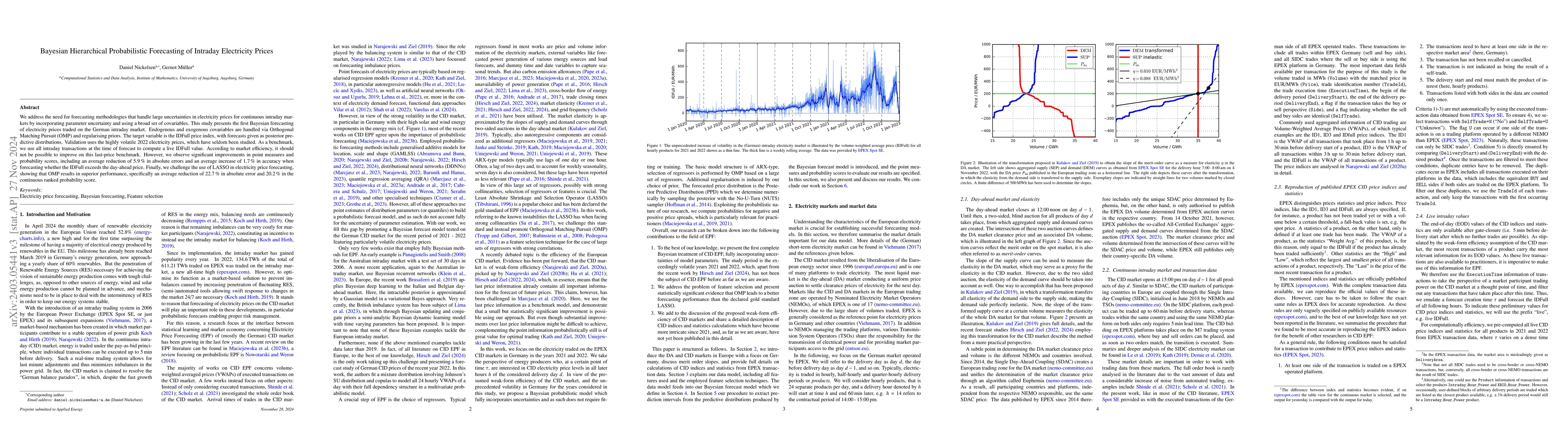

We present a first study of Bayesian forecasting of electricity prices traded on the German continuous intraday market which fully incorporates parameter uncertainty. Our target variable is the IDFu...

In the field of equation learning, exhaustively considering all possible equations derived from a basis function dictionary is infeasible. Sparse regression and greedy algorithms have emerged as pop...

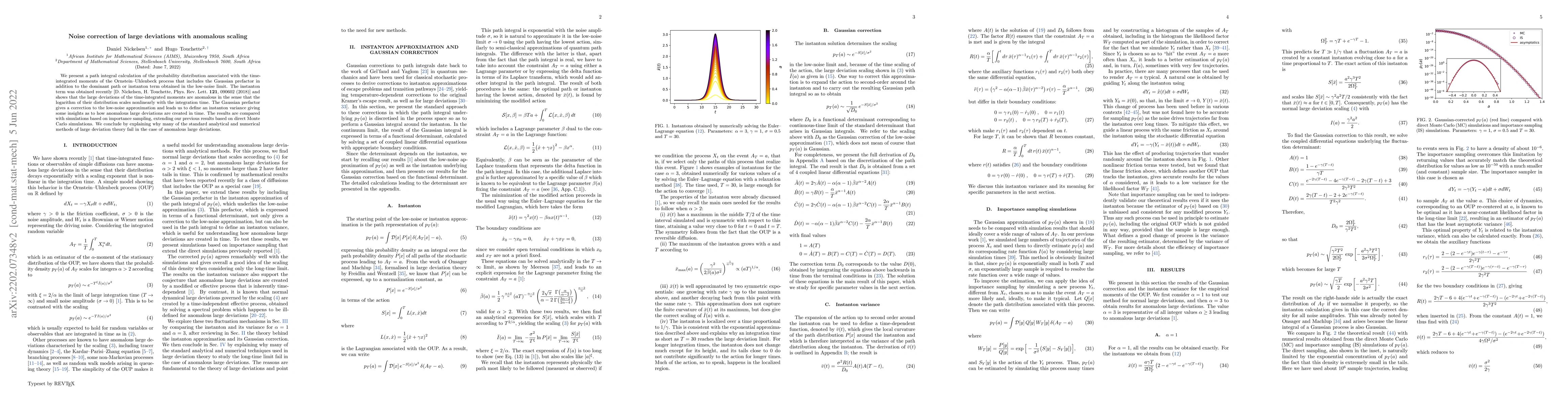

We present a path integral calculation of the probability distribution associated with the time-integrated moments of the Ornstein-Uhlenbeck process that includes the Gaussian prefactor in addition ...

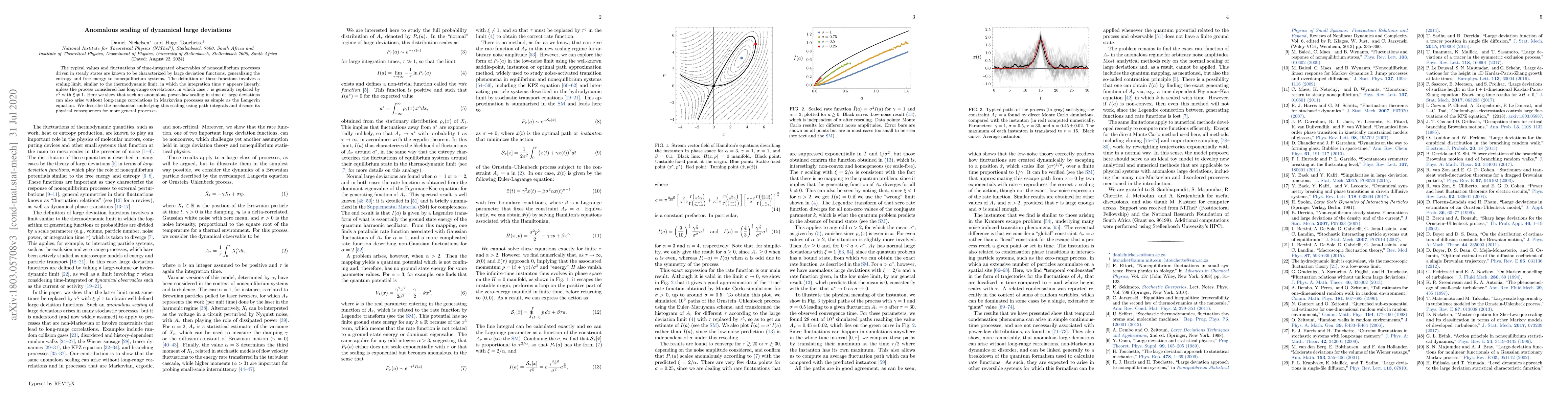

The typical values and fluctuations of time-integrated observables of nonequilibrium processes driven in steady states are known to be characterized by large deviation functions, generalizing the en...