Academic Profile

Statistics

Similar Authors

Papers on arXiv

The Fractional Stochastic Regularity Model (FSRM) is an extension of Black-Scholes model describing the multifractal nature of prices. It is based on a multifractional process with a random Hurst expo...

Implied volatility IV is a key metric in financial markets, reflecting market expectations of future price fluctuations. Research has explored IV's relationship with moneyness, focusing on its connect...

This paper investigates the estimation of the self-similarity parameter in fractional processes. We re-examine the Kolmogorov-Smirnov (KS) test as a distribution-based method for assessing self-simila...

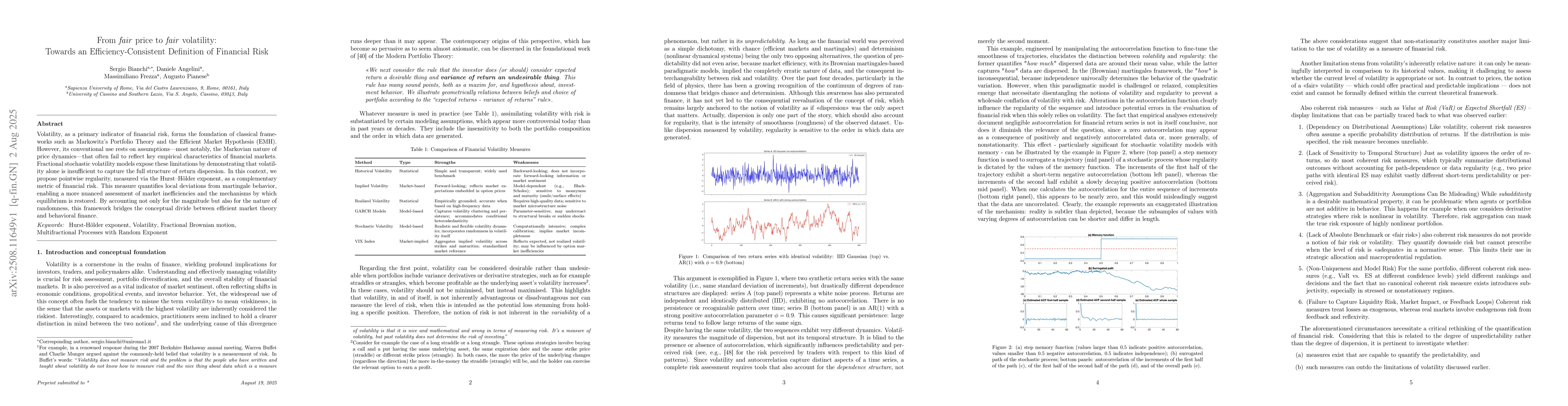

Volatility, as a primary indicator of financial risk, forms the foundation of classical frameworks such as Markowitz's Portfolio Theory and the Efficient Market Hypothesis (EMH). However, its conventi...

We introduce a novel distribution-based estimator for the Hurst parameter of log-volatility, leveraging the Kolmogorov-Smirnov statistic to assess the scaling behavior of entire distributions rather t...

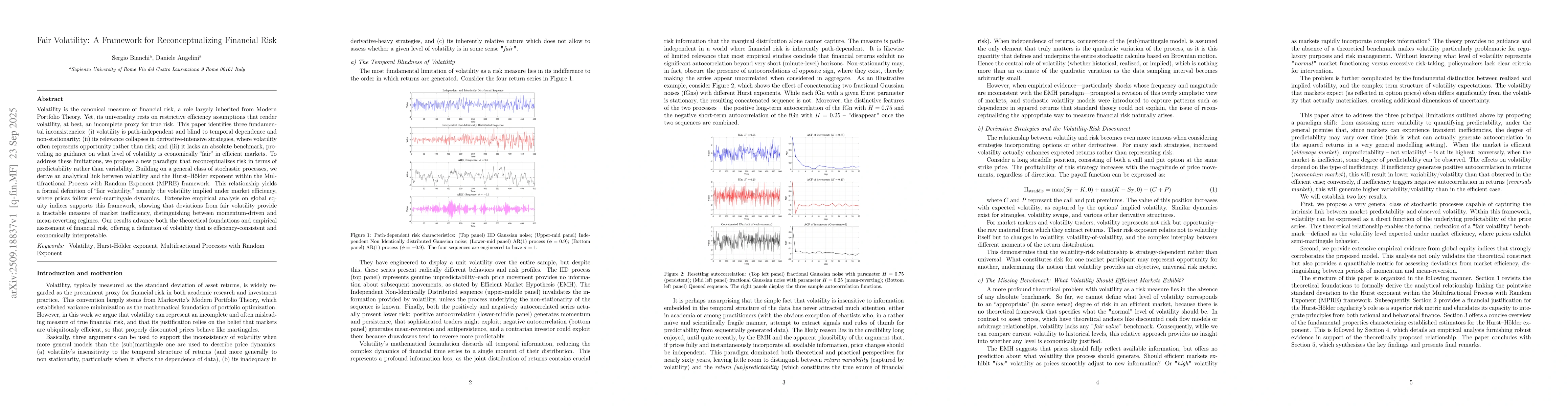

Volatility is the canonical measure of financial risk, a role largely inherited from Modern Portfolio Theory. Yet, its universality rests on restrictive efficiency assumptions that render volatility, ...