Academic Profile

Statistics

Similar Authors

Papers on arXiv

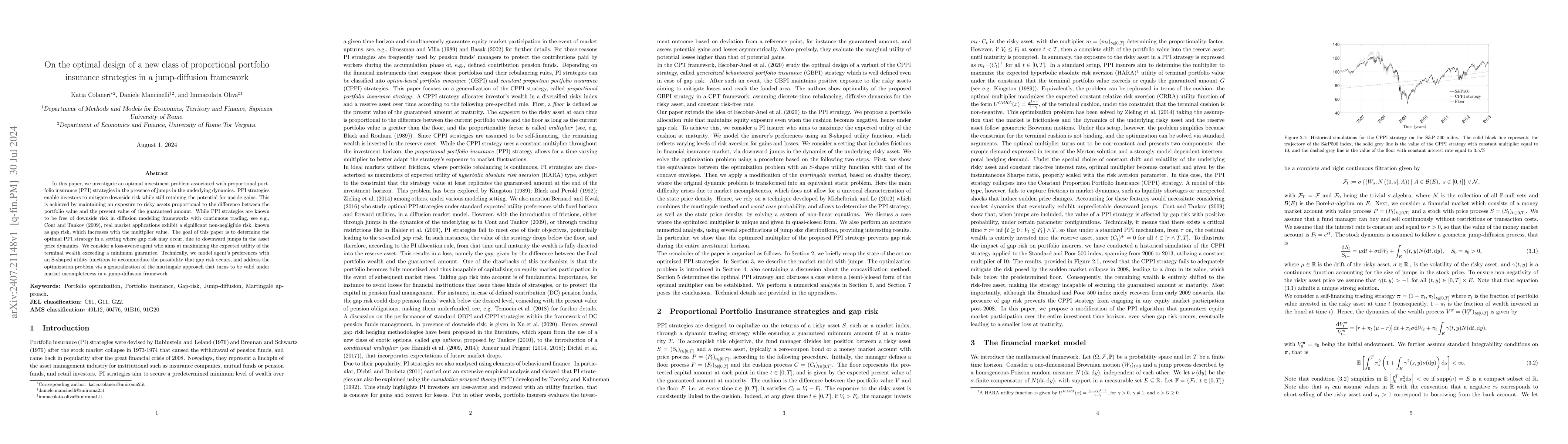

In this paper, we investigate an optimal investment problem associated with proportional portfolio insurance (PPI) strategies in the presence of jumps in the underlying dynamics. PPI strategies enable...

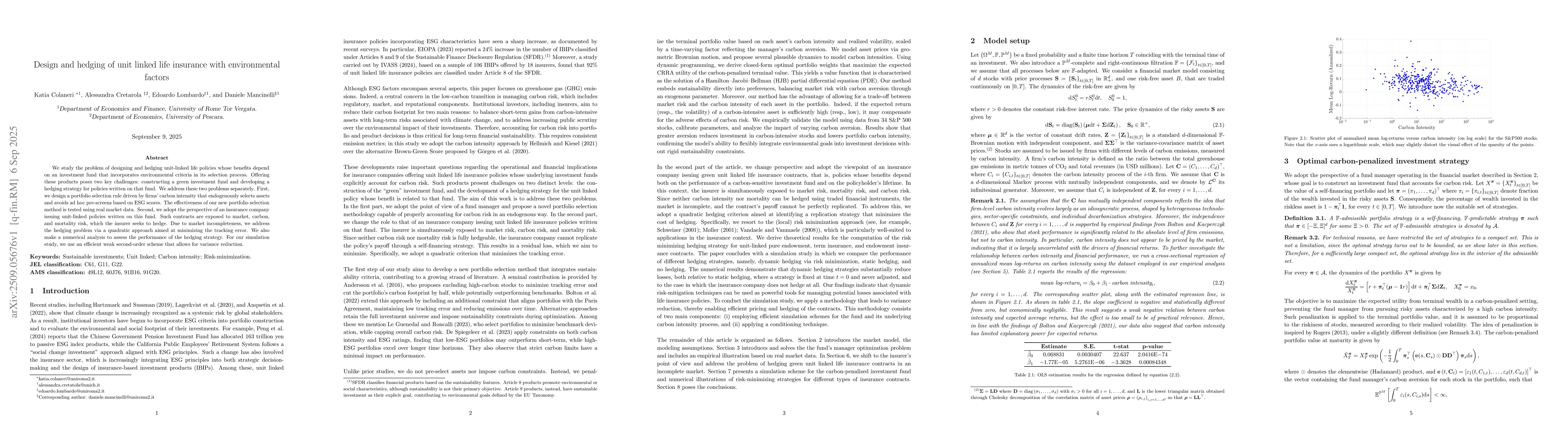

We study the problem of designing and hedging unit-linked life policies whose benefits depend on an investment fund that incorporates environmental criteria in its selection process. Offering these pr...

Given the increasing importance of environmental, social and governance (ESG) factors, particularly carbon emissions, we investigate optimal proportional portfolio insurance (PPI) strategies accountin...