Academic Profile

Statistics

Similar Authors

Papers on arXiv

Applying historical data from the USD LIBOR transition period, we estimate a joint model for SOFR, Fed Funds, and Eurodollar futures rates as well as spot USD LIBOR and term repo rates. The framewor...

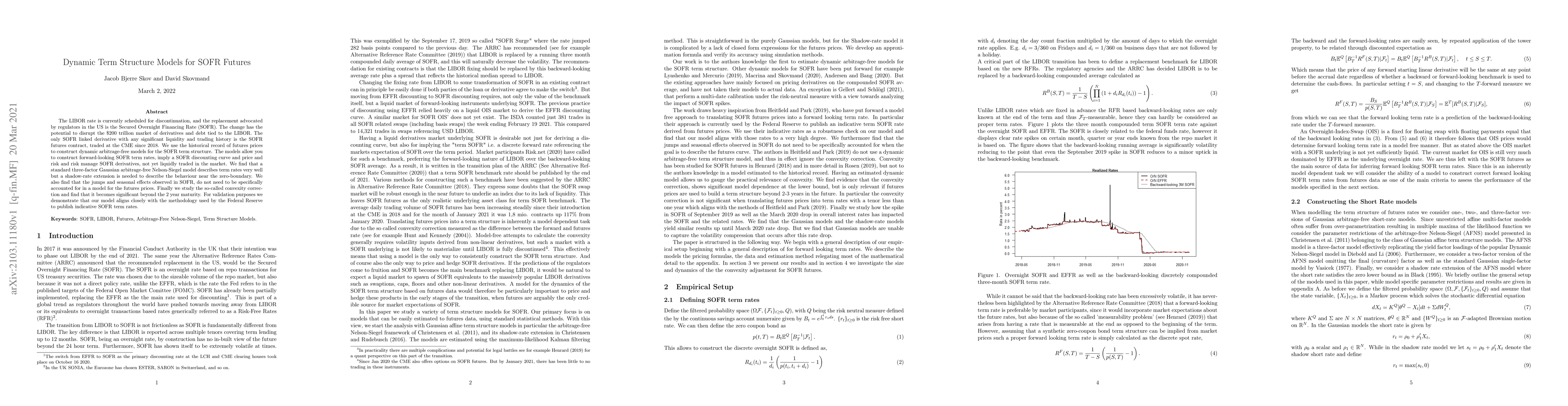

The LIBOR rate is currently scheduled for discontinuation, and the replacement advocated by regulators in the US is the Secured Overnight Financing Rate (SOFR). The change has the potential to disru...

We construct models for the pricing and risk management of inflation-linked derivatives. The models are rational in the sense that linear payoffs written on the consumer price index have prices that...