Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper explores the dynamics of Decentralized Finance (DeFi) within the Layer-2 ecosystem, focusing on Automated Market Makers (AMM) and arbitrage on Ethereum rollups. We observe significant shi...

Arbitrage can arise from the simultaneous purchase and sale of the same asset in different markets in order to profit from a difference in its price. This work systematically reviews arbitrage oppor...

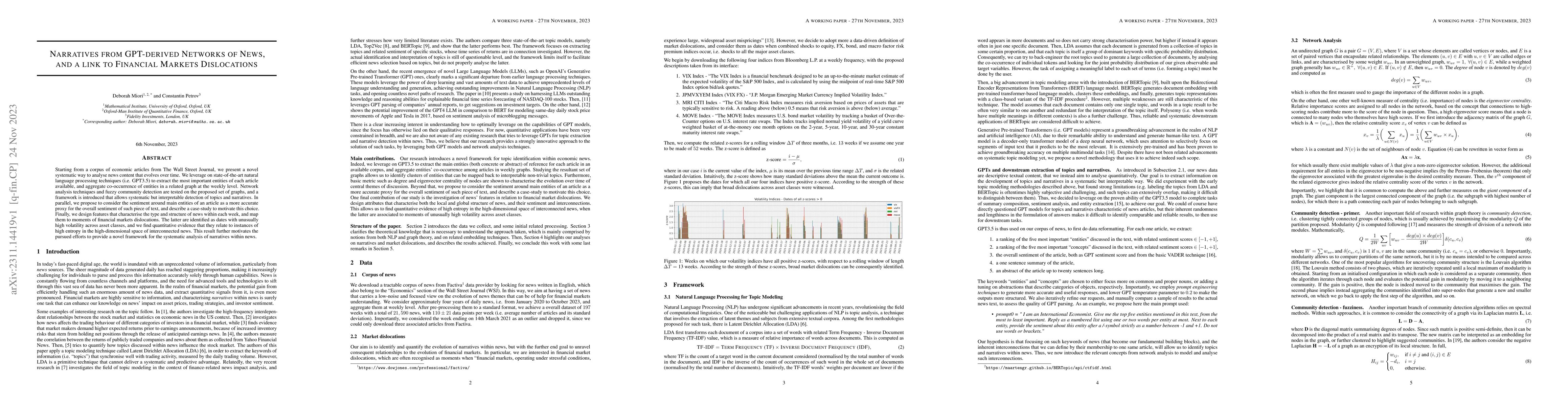

Starting from a corpus of economic articles from The Wall Street Journal, we present a novel systematic way to analyse news content that evolves over time. We leverage on state-of-the-art natural la...

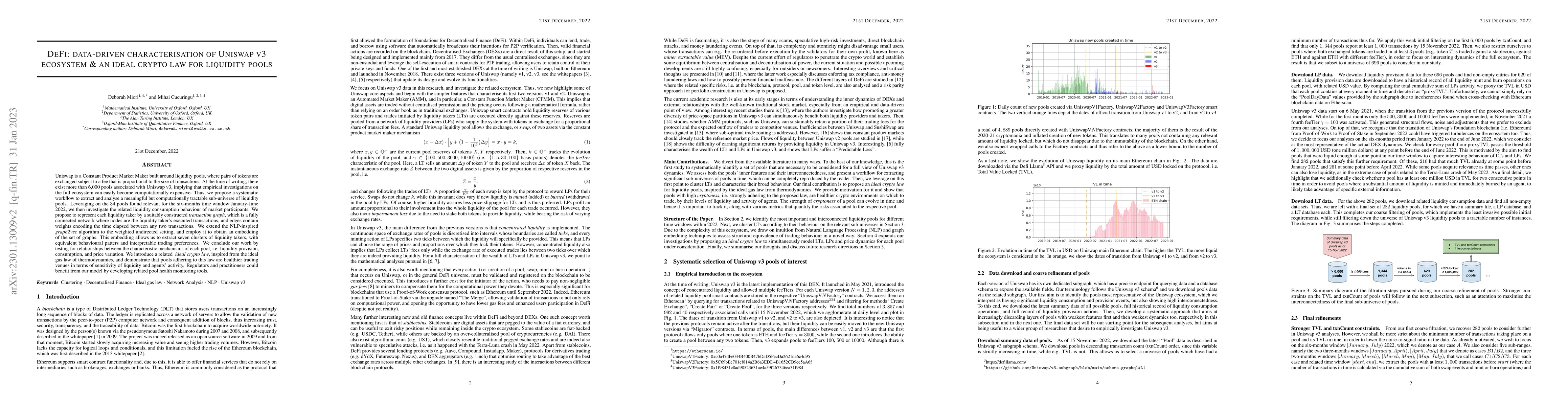

Uniswap is a Constant Product Market Maker built around liquidity pools, where pairs of tokens are exchanged subject to a fee that is proportional to the size of transactions. At the time of writing...

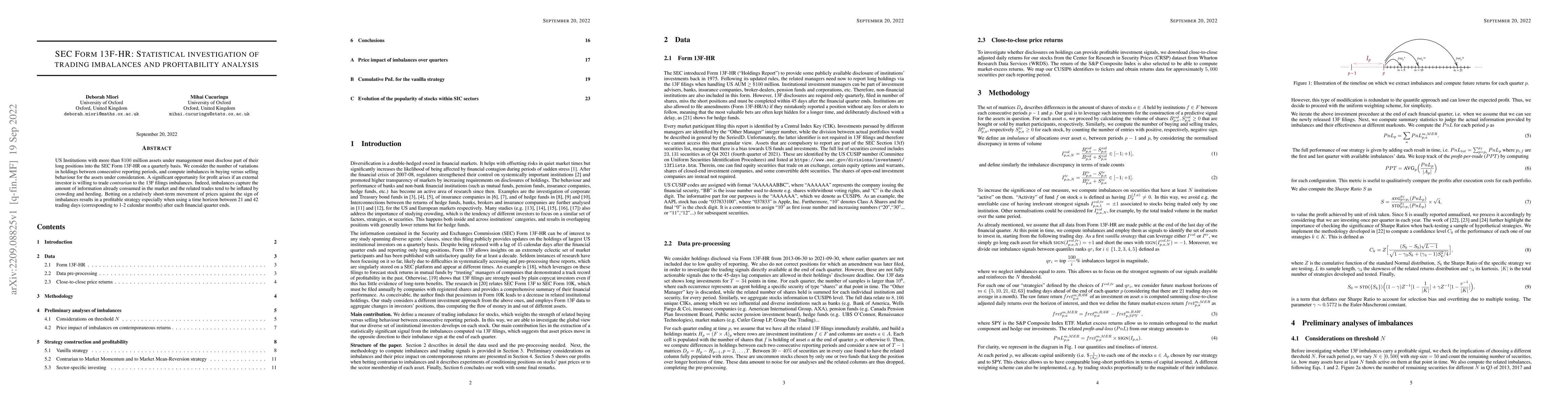

US Institutions with more than $100 million assets under management must disclose part of their long positions into the SEC Form 13F-HR on a quarterly basis. We consider the number of variations in ...

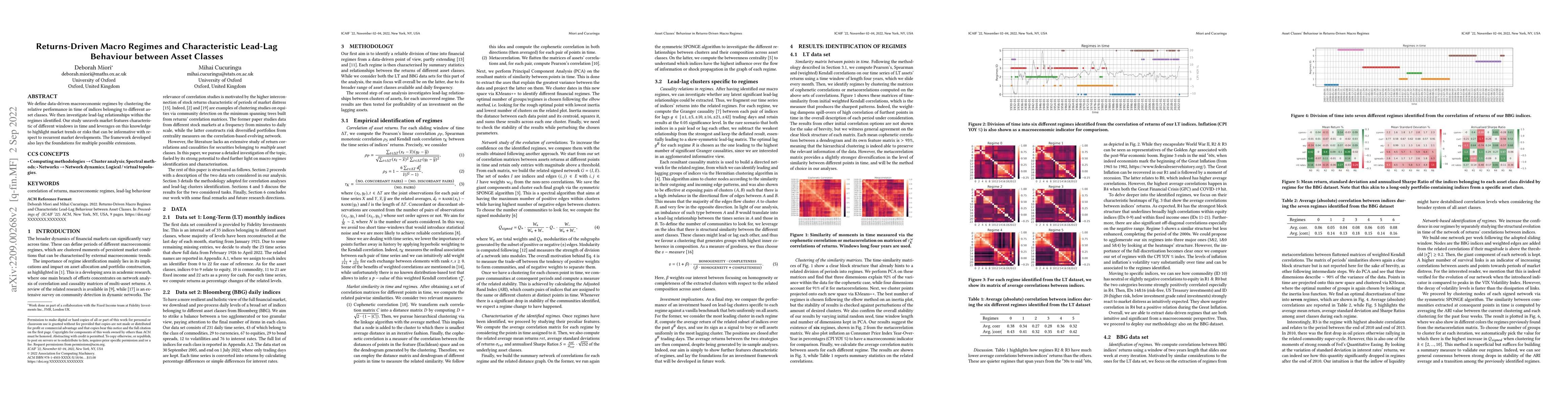

We define data-driven macroeconomic regimes by clustering the relative performance in time of indices belonging to different asset classes. We then investigate lead-lag relationships within the regi...